Michael Burry has been one of the most vocal voices against the artificial intelligence (AI) trade. Previously, the infamous investor aimed at the likes of Nvidia (NVDA) and Palantir (PLTR). Now, shares of memory chip giant Micron (MU) are entering his crosshairs.

Backing his rationale in a Substack post, Burry attributed the rally to “fear of missing out, greater fool theory, [and] public commitment bias.” Not stopping there, he also delved into the stock's historical price movement to state that, in the past 42 years, Micron stock has witnessed 34 drawdowns of 30% or more.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

Recent price movement also lends credence to Burry's theory, with MU stock down slightly over the past five days. So, should investors heed Burry's argument and short Micron? Let's take a closer look.

www.barchart.com

www.barchart.com This Time It Is Different

Burry is correct about the drawdowns and the cyclical nature of MU stock. However, investors should take into account that at no point in Micron's history has the company seen this kind of demand-supply mismatch in its favor — so much so that customers are willing to pay up ($22 billion to be precise) to secure long-term supply agreements. In fact, these “take-or-pay” agreements make sure that Micron gets paid even if the customers do not eventually want their chips.

Burry should also take into account that, even amid the drawdowns and cyclical nature of memory demand, the so-called “Big Three” of this world — Samsung, SK Hynix, and Micron — have held their market shares for several years while numerous competitors such as Intel (INTC), Texas Instruments (TXN), and NEC (NIPNF) have fallen by the wayside. As of the first quarter of 2026, these three hold 89% of the global DRAM market, with Micron's share at 22%.

Finally, we should also point out the current geopolitical scenario — where skepticism is sky-high, flashpoints are visible across the globe, and memory has become a strategic asset. Micron's status as the only major Western memory manufacturer provides the company with a critical position, not only in the AI race but also as a vital player in the region's memory chip market.

Yet, if one has to make a bearish bet, then the incumbent players (not just Micron) should be wary of the China-based players emerging in the memory market. The threat from these companies is structural, and their dominance in the electric vehicle (EV) market attests to their ability to upend an established market. Companies like ChangXin Memory Technologies (CXMT) and Yangtze Memory Technologies (YMTC) have not achieved the same prowess in high-bandwidth memory (HBM) yet, but they are aggressively filling the vacuum in the DRAM and NAND spaces. In fact, Apple (AAPL) is reportedly trying to lobby U.S. authorities in order to procure CXMT memory chips to keep its products' prices in check.

Micron's Financials Weaken the Bear Case

Micron posted an outstanding performance in the third quarter of fiscal 2026 as revenue climbed to $41.46 billion, marking a 346% year-over-year (YOY) surge. Gross margins expanded dramatically to 84.9% from 39% in the prior-year quarter.

This momentum was reflected across all primary business lines. The cloud segment contributed $13.8 billion with 306% YOY growth and 83% gross margins, while the data-center business added $11.5 billion in revenue, advancing more than 650% YOY with 87% margins. Similarly, mobile revenue reached $11.5 billion, up 254% YOY with 87% margins, while the automotive segment generated $4.6 billion, rising 313% with 79% margins. Micron continues to exhibit balanced growth across multiple areas and is not dependent on any one segment, even after applying meaningful sequential price adjustments for DRAM and NAND products.

Non-GAAP EPS increased sharply to $25.11 from $1.91 in the year-ago period, comfortably beating the consensus forecast of $20.86 and representing the ninth-straight quarter of exceeding profit expectations.

For Q4, Micron guided revenue in the range of $49 billion to $51 billion and EPS between $30 and $32 per share.

One of the most notable aspects of Q3 was the signing of 16 strategic customer agreements (SCAs) spanning the data center, consumer, and automotive sectors. These arrangements carry $22 billion in total commitments, supported by $18 billion in cash deposits. This level of visibility covers more than 80% of the company's $27 billion in capital expenditures planned for fiscal 2026.

Micron also provided an update on its HBM4E memory platform developed on the advanced 1 gamma process technology, with volume manufacturing slated for 2027. The new architecture promises important enhancements in power efficiency and bandwidth performance, strengthening the company's role as a preferred partner for leading hyperscale providers and AI processor manufacturers.

Over the nine months ended May 28, 2026, net cash from operating activities rose substantially to $45.7 billion from $11.8 billion in the prior-year period. The company ended Q3 with $25 billion in cash and only $582 million in short-term debt.

Even after a substantial share price increase, MU stock appears to trade at attractive levels. The forward price-to-earnings (P/E) ratio of 12.8 times currently stands below the corresponding sector median.

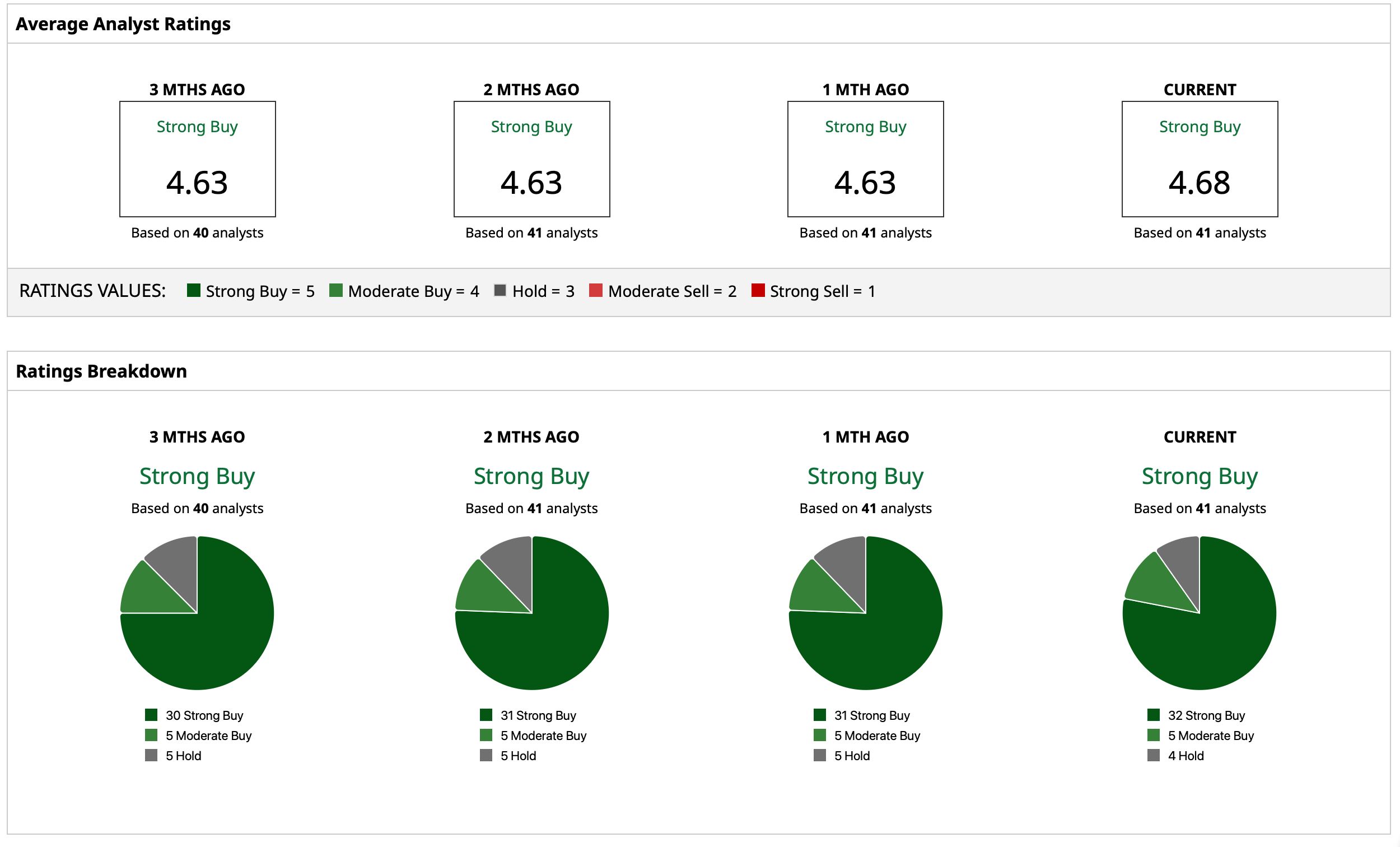

What Do Analysts Think of Micron Stock?

Overall, analysts remain bullish on Micron with a consensus “Strong Buy" rating. The mean target price of $1,487.65 indicates potential upside of 46% from current levels. Out of the 41 analysts covering MU stock, 32 have a “Strong Buy” rating, five have a “Moderate Buy” rating, and four have a “Hold” rating.

www.barchart.com

www.barchart.com On the date of publication, Pathikrit Bose did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Figma Stock Is Down 85%, But Wall Street Thinks It’s Time for the Stock to Surge Samsung Just Reported a Profit That Was Up 19-Fold. That’s Great News for Micron Stock. SK Hynix Stock Debuts for U.S. Investors Tomorrow. The DRAM ETF Could Be the Biggest Loser. There Are 100 Trillion Reasons to Watch the Upcoming U.S. Debut of SK Hynix Stock