AI has made memory one of the strategically essential parts of contemporary computing, thus making Micron Technology (MU) one of the biggest winners in the market throughout the last year. Nonetheless, any good momentum stocks eventually get corrected, and that is precisely what investors witnessed during the last couple of weeks.

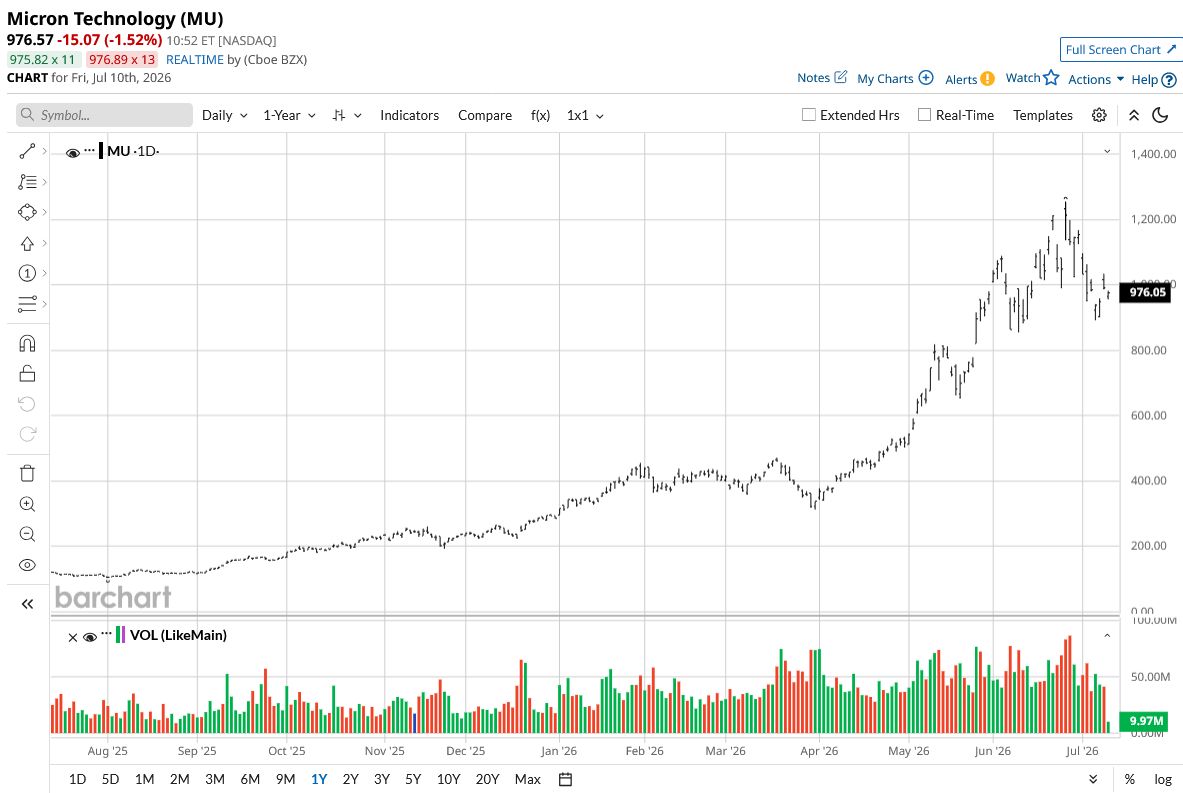

While reporting record quarterly results and providing yet another impressive outlook, Micron's shares declined by almost 25% from their June 25 high. Such a selloff led to heated discussion regarding whether the correction resulted from worsening fundamentals or just valuation correction after a very impressive run-up. For the long-term investors, such a question might be vital in the future.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

About Micron Stock

Micron Technology is among the largest providers of DRAM, NAND flash memory, and HBM (High-Bandwidth Memory) solutions used in AI accelerators, data centers, smartphones, PCs, cars, and other industries. Located in Boise, Idaho, the company has a capitalization of about $1.07 trillion, and it is one of the largest semiconductor companies in the world.

MU is still among the best-performing large-cap technology stocks. During the last 52 weeks, the stock has increased by around 692% while being about 21% below its all-time high of $1,255. MU stock still continues outperforming the overall S&P 500 ($SPX) by a substantial margin.

www.barchart.com

www.barchart.com After the selloff, the current valuation has become significantly cheaper. Currently, MU stock trades at 13 times forward P/E, which does look reasonable considering that the company is expected for the foreseeable future to report impressive earnings growth due to AI memory demand. Although the price-sales ratio of 28.7x does look quite high, investors are increasingly willing to value the company according to the earnings instead of revenue. Thus, the recent selloff eliminated some of the valuation excess of the previous period.

Although the company provides a quarterly dividend of $0.15 per share (which yields just a little), the income stream looks like an additional bonus for those who invest in Micron shares due to its long-term AI prospects.

Micron Reports Record Earnings

Micron posted another record quarter in its fiscal third-quarter 2026 results released on June 24. Revenue increased to $41.46 billion (from $23.86 billion in the previous quarter and from $9.30 billion in the same quarter of the previous year).

The profitability of the company increased even faster. Micron managed to generate GAAP EPS of $24.67 and non-GAAP EPS of $25.11 and also achieved a gross margin of almost 85%, indicating an extremely favorable environment for the company's memory products. Operating cash flow increased to $25.4 billion, allowing Micron to continue investing in its projects actively and keep its balance sheet healthy (with more than $30 billion of cash and investment).

The most interesting thing announced by management is not the record quarter but the Strategic Customer Agreements (SCAs). According to Micron's CEO, Sanjay Mehrotra, these agreements would improve the visibility and the sustainability of demand, which should help to stabilize the memory business since it is traditionally famous for boom-bust cycles because of the unpredictable customers' orders. With the new SCAs, Micron can make its demand more predictable and lock in.

Also, Micron continues investing at a record pace in building capacity for manufacturing memory solutions, especially high-bandwidth memory for AI GPUs. Although these investments lead to the growth of the capital expenditures of the company now, they allow it to prepare for the multi-year AI infrastructure expansion.

What Do Analysts Expect for MU Stock?

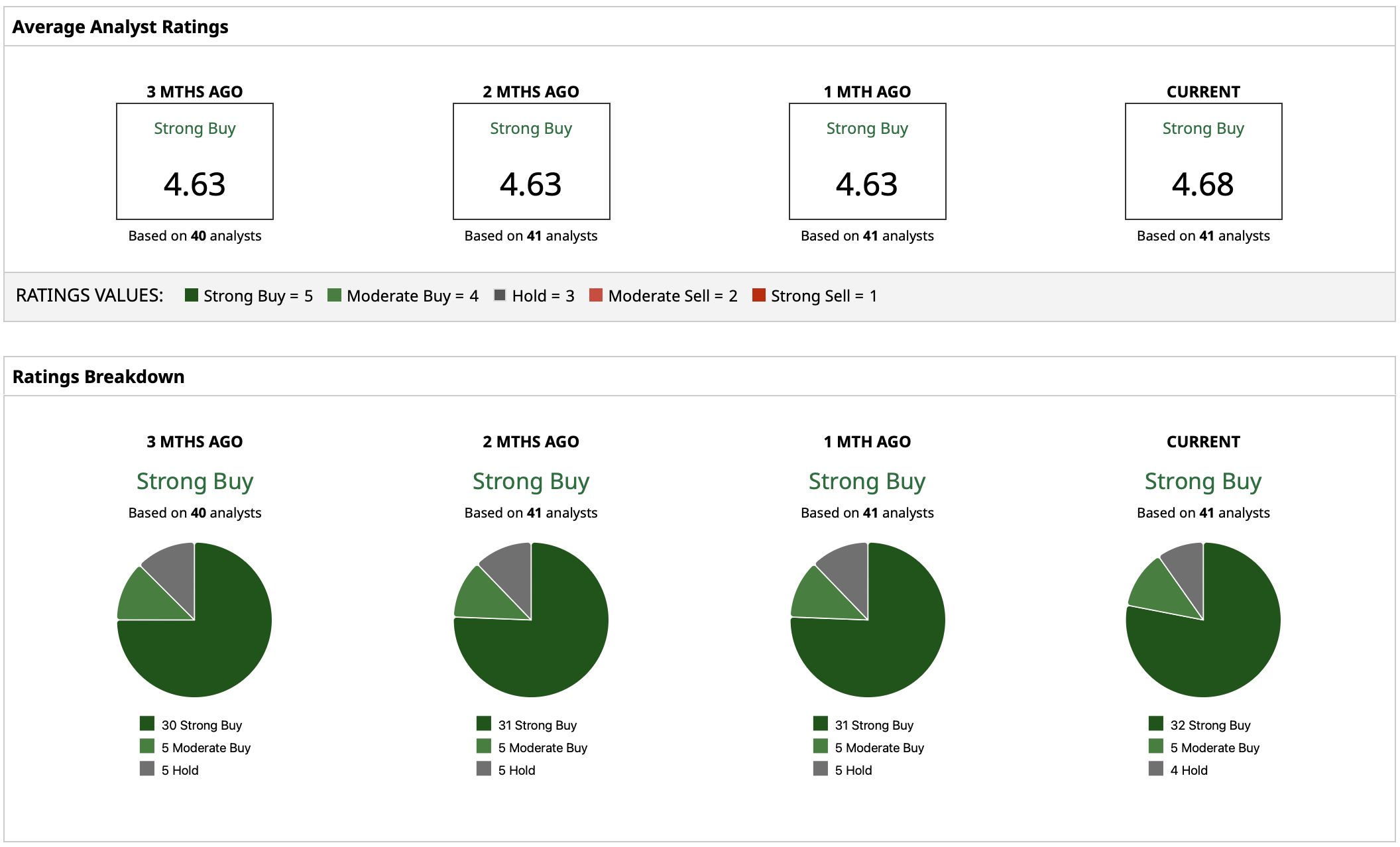

The Street appears to be still overwhelmingly positive on MU stock despite the recent correction, assigning a “Strong Buy” rating consensus. Analysts are indicating that they believe AI memory demand is still in its early stages. The mean price target is $1,487.65, while the highest price target is even higher ($2,000). Considering Thursday's closing price of $991.64, analysts' mean target of $1,487.65 suggests a potential upside of 50%.

www.barchart.com

www.barchart.com On the date of publication, Yiannis Zourmpanos had a position in: MU . All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

How to Play Micron Stock After It Lost a Quarter of Its Value in Just 2 Weeks Backblaze Is a Little-Known Cloud Storage Stock Up More Than 200% This Year Rackspace Slashed Revenue Guidance, Sending RXT Stock Plummeting. What Comes Next. Salesforce Just Scored a Major Air Force Win. How to Play CRM Stock Here.