After years of navigating post-pandemic uncertainty, Delta Air Lines (DAL) has reemerged as one of the strongest performers in the airline industry. The stock has climbed 24.5% in 2026, yet Wall Street remains overwhelmingly bullish, reflecting confidence that the rally may not be over.

Investors are increasingly betting that resilient travel demand, premium revenue growth, and disciplined capacity management will continue to support earnings even amid elevated fuel costs and broader macroeconomic uncertainty. Recent quarterly results reinforced that optimism, with Delta delivering an earnings beat and reaffirming its full-year outlook.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

Moreover, with analysts continuing to raise price targets, Delta appears well-positioned to outperform many cyclical peers through the remainder of 2026.

About Delta Air Lines Stock

As one of the world’s largest airlines, Delta provides scheduled passenger and cargo transportation across an extensive domestic and international network. Headquartered in Atlanta, Georgia, the company operates major hub airports across the United States and generates revenue through its airline operations, premium travel offerings, loyalty program, and refinery segment. Delta has a market cap of $57.41 billion, making it one of the largest publicly traded airlines globally.

DAL has significantly outperformed the broader market and most U.S. airline peers over the past year, reflecting improving investor confidence in the carrier’s earnings power and strategy. The stock is up 52.5% over the past 52 weeks and 24.5% year-to-date (YTD), extending a rally that has been fueled by stronger-than-expected financial results and resilient travel demand.

Also, the rally has propelled Delta to a 52-week high of $95.68 on July 2, as investors rewarded Delta for consistently delivering record revenue, expanding premium and loyalty revenues, and maintaining disciplined capacity growth despite elevated fuel costs.

www.barchart.com

www.barchart.com Despite the solid run, the stock seems to be trading at a discount compared to industry peers at 15.40 times forward earnings.

Record Top-Line Performance

Delta Air Lines reported its second-quarter 2026 financial results on July 10, delivering results that exceeded Wall Street expectations despite facing high fuel costs. Solid pricing power and resilient demand for premium travel enabled the airline to offset much of the surge in fuel expenses while maintaining its full-year outlook.

Total revenue increased 14% year-over-year (YOY) to a record $17.7 billion. Adjusted earnings per share came in at $1.56, down 26% from $2.12 a year earlier as fuel costs weighed on profitability, although the figure comfortably beat analysts’ estimates. Adjusted net income declined 26% YOY to $1.03 billion.

Premium revenue climbed 17%, loyalty revenue rose 19%, and cargo revenue surged 39%, reflecting continued strength in high-margin revenue streams. Capacity increased only about 1%, highlighting Delta’s disciplined approach to supply growth. Adjusted fuel expense jumped 77% YOY to $4.4 billion, with the average fuel price rising to $3.93 per gallon, significantly pressuring margins.

Furthermore, Delta guided for third-quarter adjusted EPS of $2.00 to $2.50, revenue growth in the mid-teens, and an operating margin of 11% to 13%. Management reaffirmed its full-year 2026 adjusted EPS guidance of $6.50 to $7.50, citing resilient travel demand, sustained fare strength, and confidence that premium and loyalty revenues will continue to support earnings despite uncertainty surrounding fuel prices.

Analysts predict EPS to decline marginally to $6.50 in fiscal 2026, but surge by 19.85% annually to $7.79 in fiscal 2027.

Wall Street Remains Highly Bullish

Recently, Morgan Stanley raised its price target on Delta Air Lines to $115 from $105 while reiterating its “Overweight” rating, reflecting increased confidence in the airline’s earnings outlook and growth prospects. Analyst Ravi Shanker said that what initially appeared likely to be a disruptive quarter had instead ended on a positive note, reinforcing Morgan Stanley’s bullish stance on Delta.

Also, UBS reiterated its “Buy” rating on Delta Air Lines while maintaining its $107 price target.

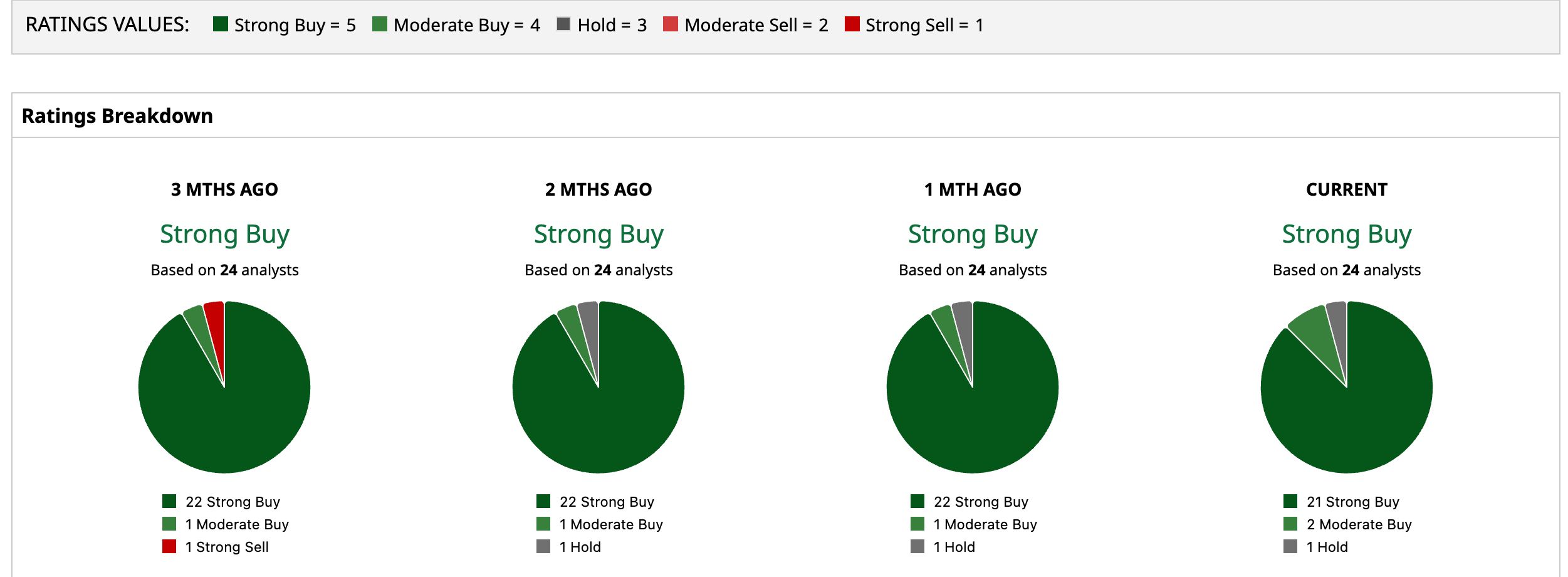

Overall, DAL has a consensus “Strong Buy” rating. Of the 24 analysts covering the stock, 21 advise a “Strong Buy,” two suggest a “Moderate Buy,” and one recommends a “Hold.”

The average analyst price target for DAL is $100.76, indicating a potential upside of 16.7%. The Street-high target price of $116 suggests that the stock could rally 34.3% from here.

www.barchart.com

www.barchart.com  www.barchart.com

www.barchart.com On the date of publication, Subhasree Kar did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Why Delta Air Lines Could Be a Top Stock to Buy for the Rest of 2026 Why Analysts Are Betting Western Digital Stock Can Gain Another 30% from Here COIN Stock Alert: 3 Reasons Why Coinbase Shares Are In Focus A New Report Says Meta Platforms Could Overtake Google AI. How to Play META Stock Here.