International Business Machines (IBM) just suffered the largest single-day drop in its long history.

The cause?

Can’t Get Enough Options?: Join the list for Barchart’s daily unusual options report, delivered free.

Missed revenue, missed earnings, but most damningly, the company stated that many of their clients are shifting their “quarterly capex towards servers, storage, and memory purchases” in the last few weeks of June, implying that customer spending will be down in the upcoming months.

Now, if you’re bullish on IBM, this might present a good opportunity to buy - an opportunity that comes around maybe once every 10- 15 years. After all, it’s still a good business, despite the sour guidance.

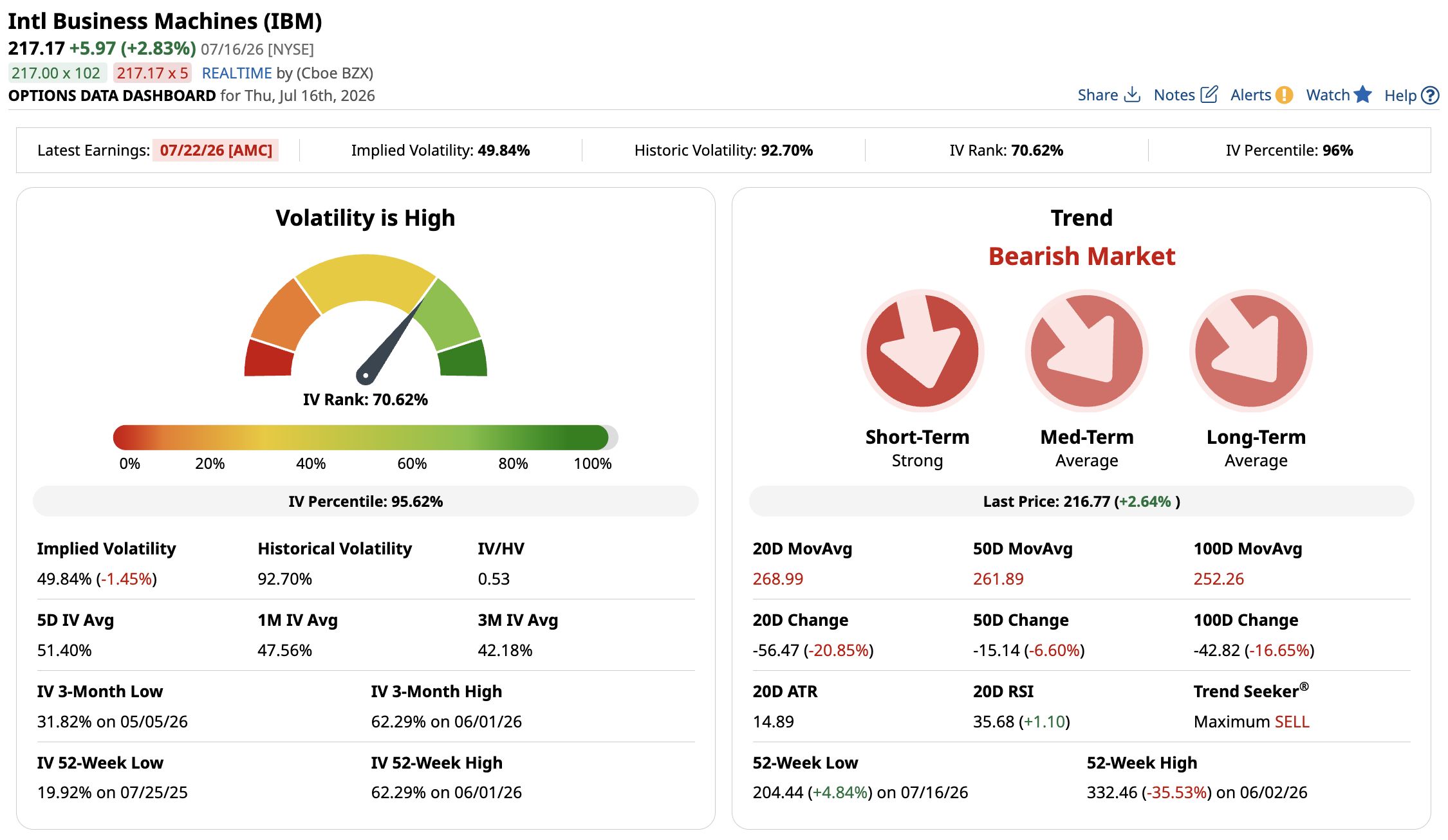

If you’re thinking of going the options route, selling a put option might be a good idea. Barchart's option dashboard pretty much says it all:

IV rank is highly elevated, meaning for option sellers, the opportunity is there; all you need is the right move.

So here’s a very interesting idea to consider.

Ride out the volatility by selling a put option

For those unfamiliar, selling a put, or being "short" a put, involves collecting an upfront premium in exchange for agreeing to buy a stock at a predetermined price (strike price) if the option is assigned before it expires. The goal of short puts is for the stock to trade above the strike price at expiration, allowing you to keep the entire premium without further obligation.

The reason why you're starting with this strategy is that options generally become more valuable when implied volatility is elevated. Since IBM's earnings miss sent volatility soaring, put premiums are higher than usual, allowing you to collect more income for taking on the obligation to buy the stock.

But that’s the crux here: if you sell an option, you commit to buying 100 shares of IBM if assigned. That means you need the buying power to do so and, more importantly, you need to believe that the stock’s price will improve later on.

However, that same risk is also why selling puts is one of the best ways to buy stocks at a discount. If you set the strike price below the current trading price and get assigned, you get paid to wait for IBM to go down to your preferred purchase price.

Looking for short put trades

With that settled, let’s look for trades.

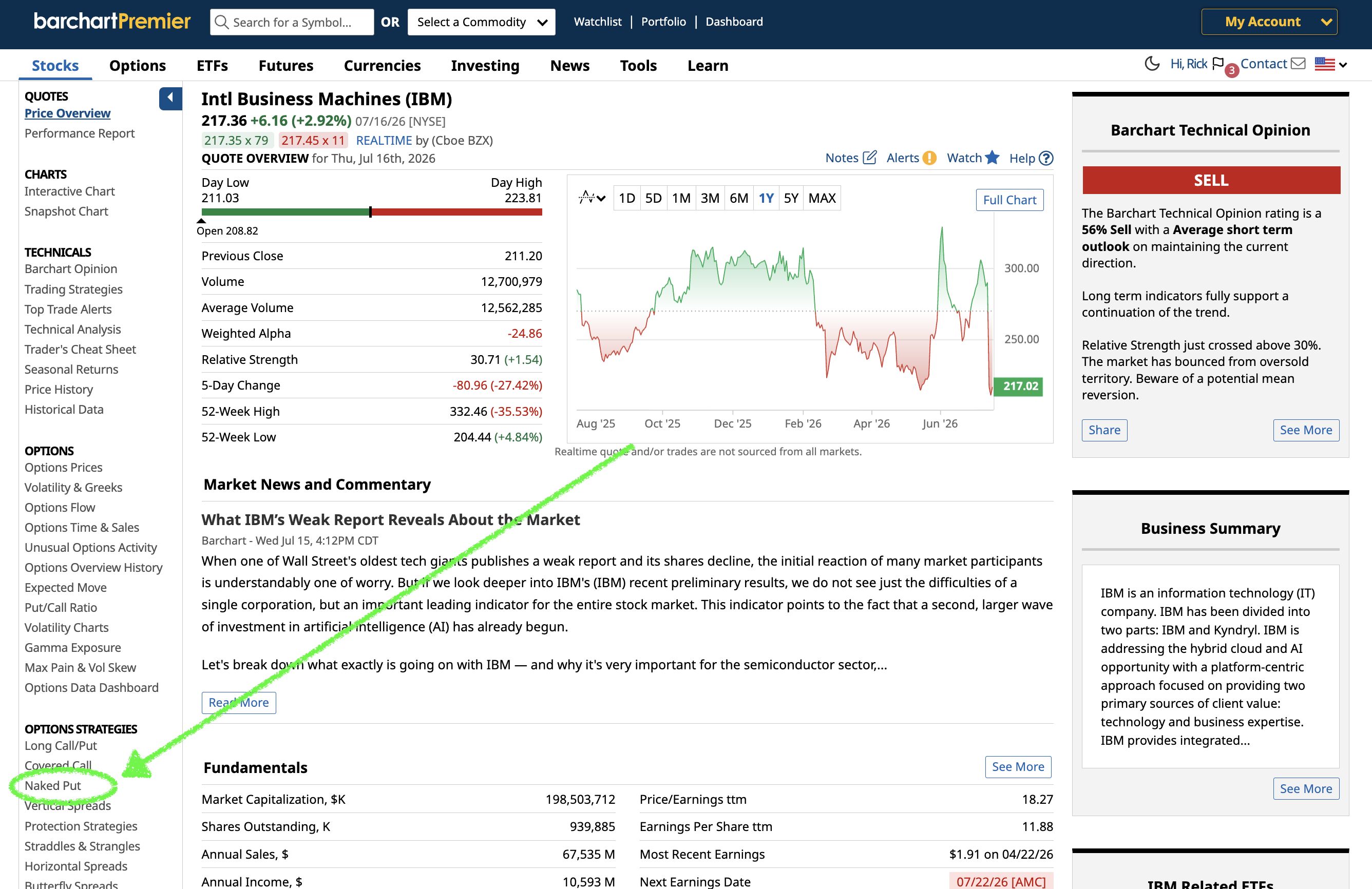

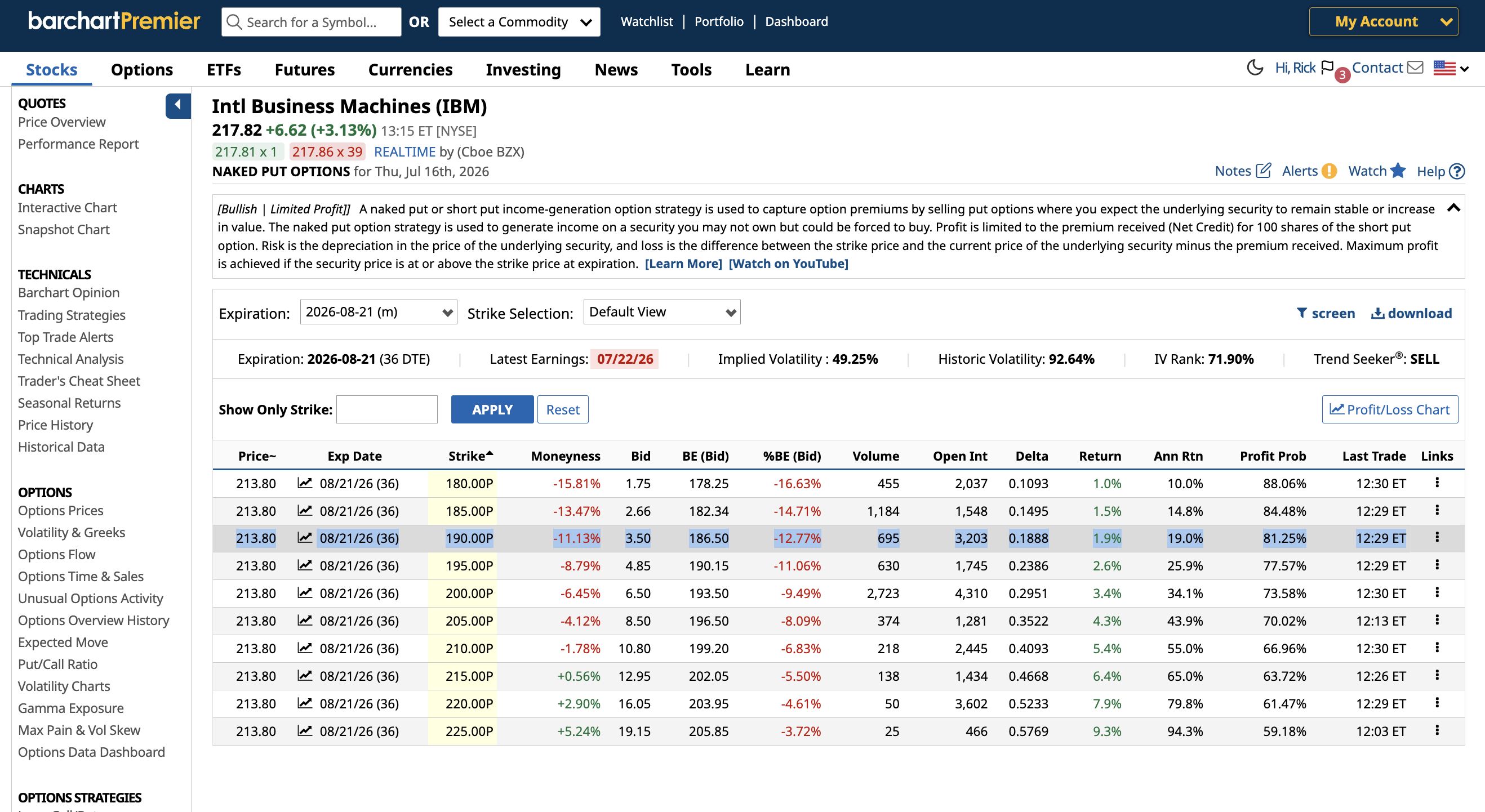

From IBM’s overview page, click Naked Put on the left-hand side, below Option Strategies.

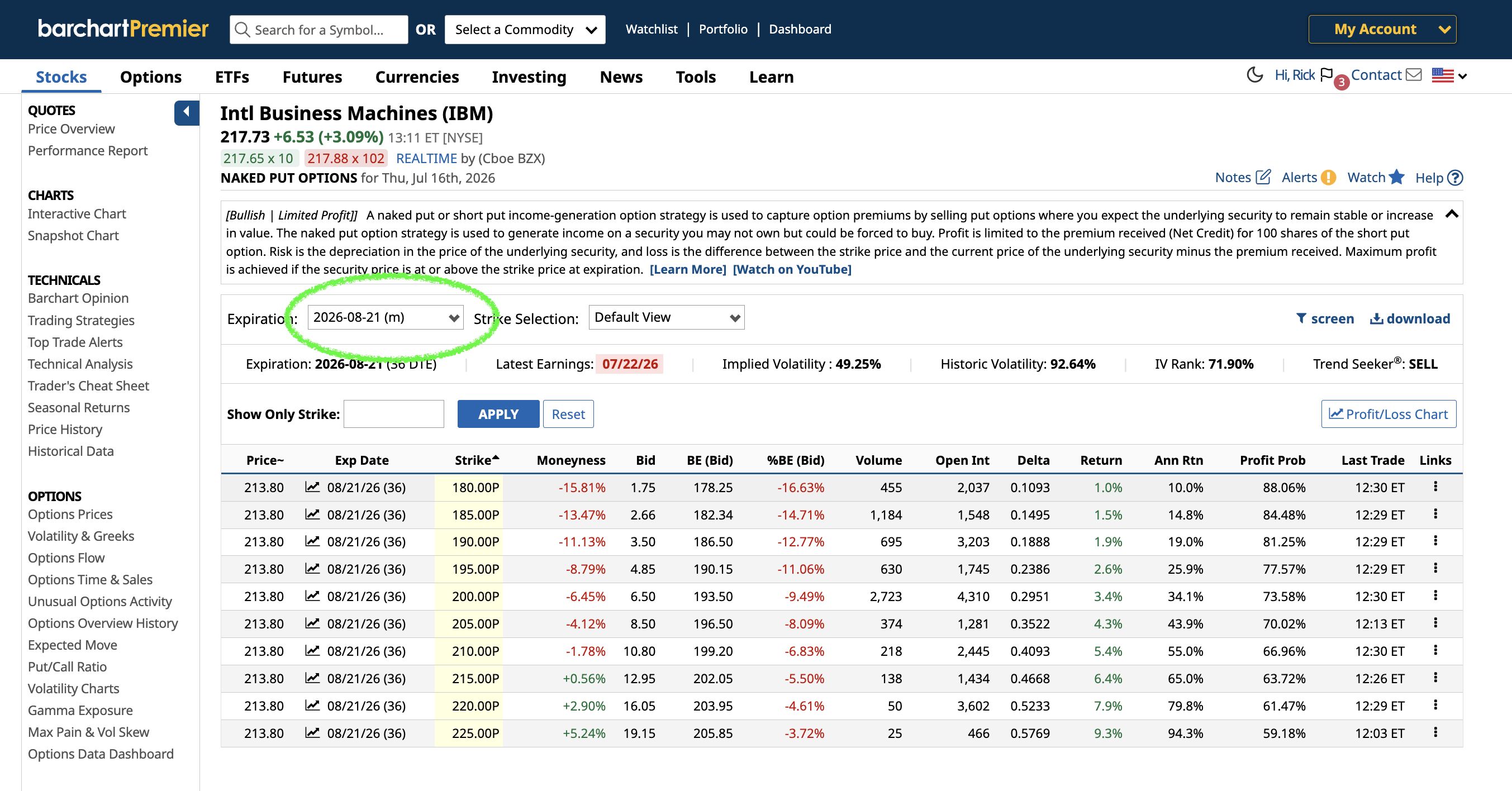

Once there, you can change the expiration date from this drop-down.

I often prefer to sell puts 30-45 days out. This way, I get the benefit of higher premiums because of the additional time value, while still allowing theta decay to work in my favor as expiration approaches.

So here are short put trades expiring on August 21, 37 days away from today.

But how about strike selection?

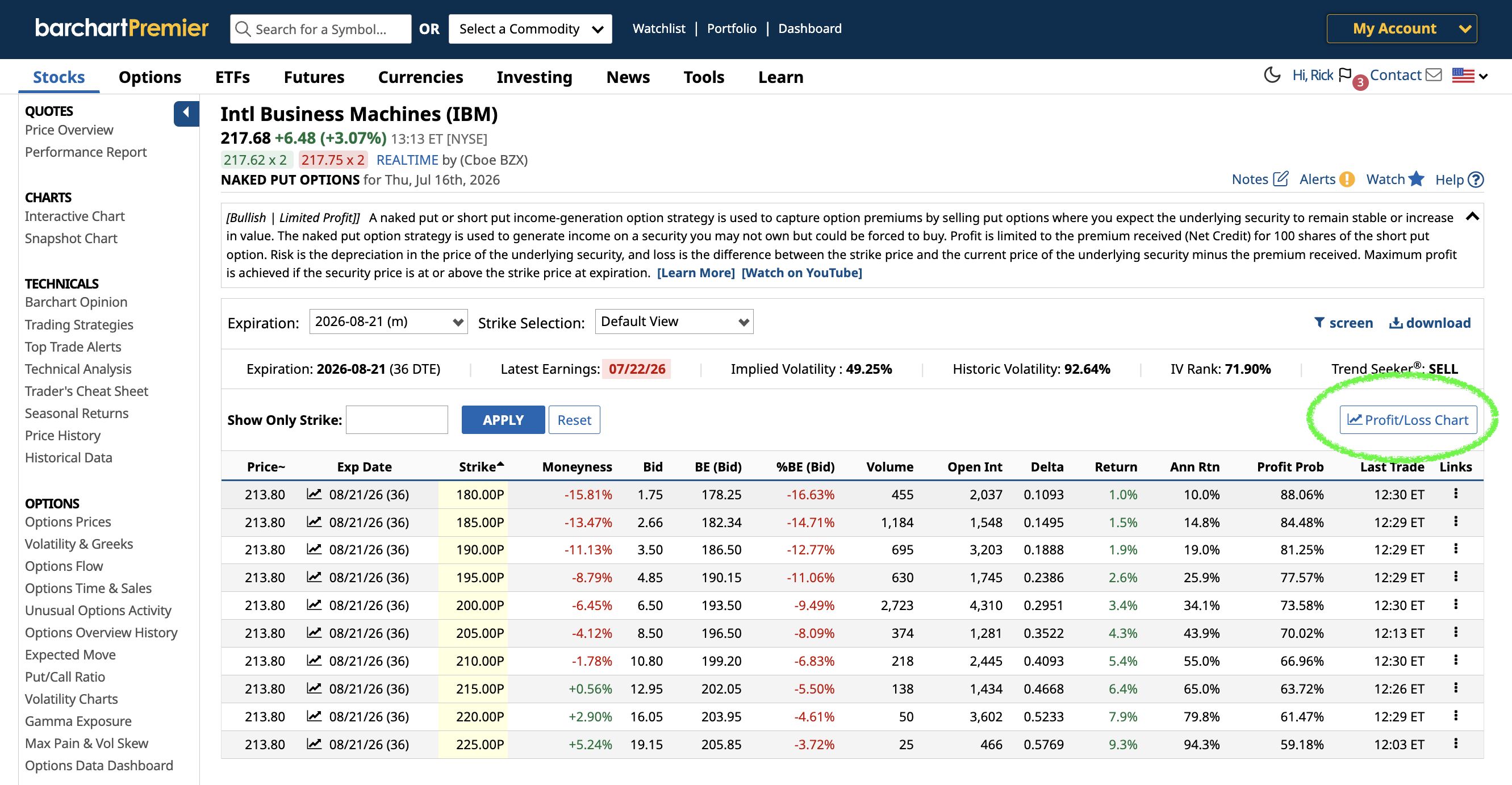

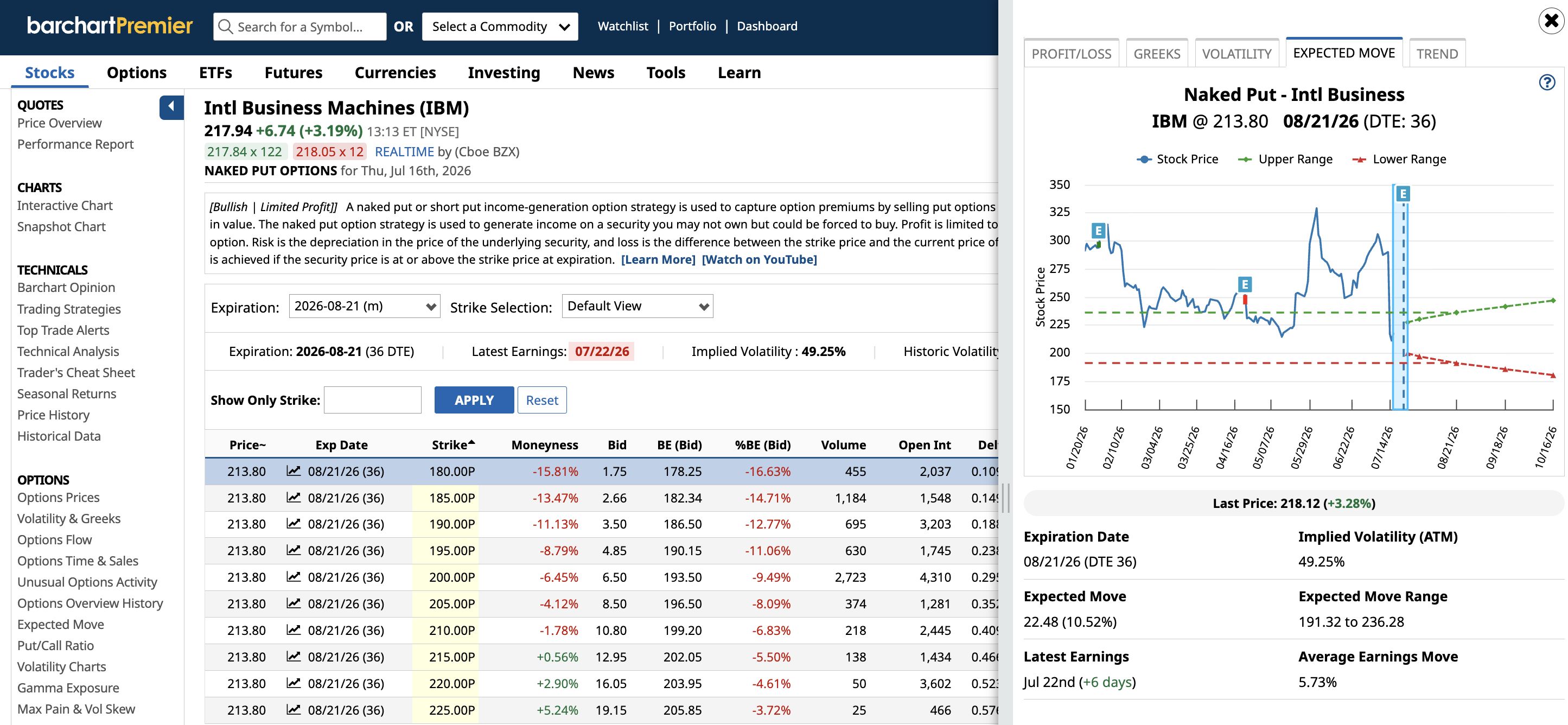

Barchart’s PNL chart feature can help with that. Just click on the Profit/Loss Chart icon here.

From there, click the Expected Move tab. This shows the price range the options market expects IBM to trade within by expiration based on current option prices.

According to this chart, IBM is expected to trade between $191.32 and $236.28 by August 21.

So, I’d set the strike price below that $191 level, let's say $190, so that I’m relatively safe from assignment.

And if we check the 190-strike short put here, I can get $3.50 per share or $350 per contract. Meanwhile, the trade has an 81.25% probability of profit, which is very decent odds.

Now, if I get assigned, I get IBM at a discount to the current price. Also, not bad at all.

But again, the goal is for the put to expire worthless. So, let's say it does. August 21 passes, and IBM stays over $190. Your short put expires worthless, and you get to keep $350. Otherwise, you get to buy 100 shares of IBM at $190.

Of course, if you're happy buying IBM at today's price, why not sell the $215 strike and get paid $1295 per contract? Food for thought.

Conclusion

Your option strategies should always match and adapt to the ongoing market conditions, not the other way around.

With this strategy, you get paid to wait for the stock to maybe come down to your price. And if it does, you got paid for buying it. Can't complain about that.

On the date of publication, Rick Orford did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

AAP’s Unusually Active $62.50 Call Isn’t a Covered Call. It’s a Bullish Bet on a Beaten-Down Stock. IBM Just Had the Worst Day in Its History. Here's How to Get Paid to Buy the Dip. Why Strategy’s (MSTR) Q2 Earnings Test May Help Engineer a Short-Term Pop Micron Technology Bear Call Spread Could Net 16% in Five Weeks