Alibaba Group BABA is offering $1.5 billion to acquire Chinese grocery delivery firm Pupu, initiating a bidding war as part of a broader campaign to wrest market share from online commerce rival Meituan. The proposed price is more than double an earlier $600 million bid from Sun Art Retail, a former Alibaba affiliate now backed by private equity firm DCP Capital.

Founded in Fujian province, Pupu operates as one of China's leading instant grocery delivery platforms, generating annual revenues exceeding RMB 30 billion and running a rapid 30-minute delivery network across key cities in Fujian, Guangdong, Sichuan and Hubei provinces. The proposed acquisition reflects Alibaba's accelerating pivot toward supply-chain depth over pure platform economics — a direct response to intensifying rivalry with Meituan and JD.com in local commerce.

This strategic push aligns with what Alibaba's fourth-quarter fiscal 2026 results already reveal about the company's spending direction. Quick commerce revenues in the fourth quarter of fiscal 2026 surged 57% year over year to RMB 19,988 million, driven by order growth following the rollout of Taobao Instant Commerce in late April 2025. For full-year fiscal 2026, quick commerce revenues reached RMB 78,520 million, up 47% year over year. However, adjusted EBITA fell 84% year over year to RMB 5,102 million, and non-GAAP net income declined nearly 100%, with free cash flow swinging to an outflow of RMB 17,300 million, attributed primarily to investments in quick commerce and cloud infrastructure.

The timing is complicated by a fresh regulatory overhang. Alibaba shares fell as much as 6.5% in Hong Kong — their biggest single-session decline in nearly three months — after the Beijing branch of SAMR summoned the company along with JD.com JD, PDD Holdings PDD, ByteDance and Xiaohongshu over alleged false advertising during the 618-midyear shopping festival. The summons highlighted Beijing's broader campaign against ruinous price wars and misleading promotional tactics, pushing platforms to pivot from aggressive discounting toward innovation and quality services.

For Alibaba, the Pupu bid signals confidence in its instant retail strategy even as near-term profitability faces pressure. Whether regulators ultimately clear the deal — and whether Alibaba can integrate Pupu's regional supply chain at scale — will shape how effectively this capital-intensive gamble pays off against a tightening competitive and regulatory landscape.

How JD.com and PDD Holdings Stack Up

Alibaba's quick commerce push mirrors the strategic calculus of its two U.S.-listed rivals. JD.com has been scaling its food delivery arm steadily, with JD Food Delivery improving unit economics and narrowing sequential losses every quarter since launch, while JD Retail posted a record operating margin of 5.6% in the first quarter of 2026. JD.com, however, remains focused on organic build-out rather than large acquisitions. PDD Holdings, meanwhile, has signaled that supply chain investment is the company’s core strategic priority heading into its next decade, committing significant long-term resources even at the expense of near-term profitability. Both JD.com and PDD Holdings were among the platforms summoned by SAMR over 618 promotional practices, placing all three companies under similar regulatory clouds as each navigates its own path in China's fiercely contested local commerce arena.

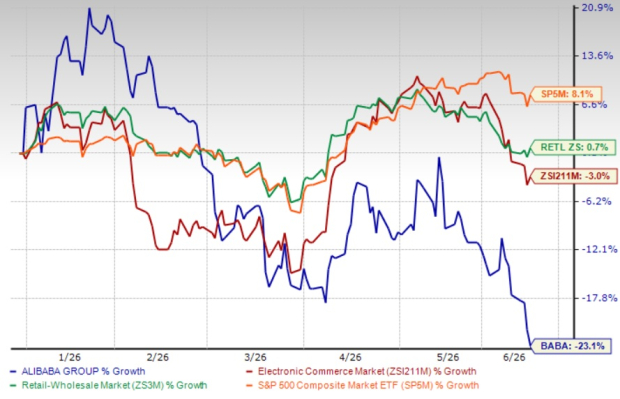

BABA’s Share Price Performance, Valuation & Estimates

BABA shares have lost 23.1% in the year-to-date period, underperforming the Zacks Internet – Commerce industry and the Zacks Retail-Wholesale sector, respectively.

BABA’s YTD Price Performance

Image Source: Zacks Investment Research

From a valuation standpoint, BABA stock is currently trading at a trailing 12-month Price/Earnings ratio of 35.66X compared with the industry’s 29.42X. BABA has a Value Score of D.

BABA’s Valuation

Image Source: Zacks Investment Research

The Zacks Consensus Estimate for fiscal 2027 earnings is pegged at $7.38 per share, down 4.3% over the past 60 days, indicating a 89.72% year-over-year increase.

Alibaba Group Holding Limited Price and Consensus

Alibaba Group Holding Limited price-consensus-chart | Alibaba Group Holding Limited Quote

Alibaba currently has a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Beyond Nvidia: AI's Second Wave Is Here

The AI revolution has already minted millionaires. But the stocks everyone knows about aren't likely to keep delivering the biggest profits. AI’s second wave is moving from infrastructure to implementation and these companies are at the forefront of this transition, positioned to become what Amazon and Google were to the internet era.

See Stocks Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

JD.com, Inc. (JD): Free Stock Analysis Report

Alibaba Group Holding Limited (BABA): Free Stock Analysis Report

PDD Holdings Inc. Sponsored ADR (PDD): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).