Bristol Myers Squibb BMY is navigating a revenue mix shift as growth products portfolio now assumes a larger role in the business, helping mitigate the impact of declining sales from mature products facing generics.

The growth portfolio — including Opdivo, Opdivo Qvantig, Orencia, Yervoy, Reblozyl, Camzyos, Breyanzi, Opdualag, Zeposia, Sotyku, Krazati and Cobenfy — is becoming central to top-line resilience. Sales from this segment rose 12% in the first quarter of 2026, lifting its contribution to 54% of total revenues from 49.7% in the first quarter of 2025. This shift signals improving revenue durability and supports a more favorable long-term growth outlook.

Within this mix, Reblozyl, Breyanzi, Opdualag, Qvantig and Cobenfy propelled growth in the first quarter.

Opdivo Qvantig (nivolumab and hyaluronidase-nvhy- subcutaneous formulation) has witnessed strong uptake across all approved tumor types in the United States.

Other key drugs are contributing to revenue growth, though at varying stages of maturity.

Opdualag sales remain robust, particularly in the United States, where it continues to serve as a standard of care in first-line melanoma.

Reblozyl recorded strong sales growth, driven by continued adoption in both first-line and second-line treatment settings for patients with myelodysplastic syndrome (MDS)-associated anemia.

Breyanzi continues to deliver solid growth, driven by ongoing uptake across its approved large B-cell lymphoma indications in both the United States and international markets. The strong performance highlights sustained demand for the therapy and supports expectations for continued commercial expansion.

Camzyos continues to gain traction in the cardiovascular market, supported by growing demand and increased adoption among eligible patients.

In immunology, Sotyktu remains an important growth driver. The recent approval in psoriatic arthritis expands its commercial opportunity and strengthens BMY’s presence in rheumatology. Additional upside could come from ongoing phase III programs in systemic lupus erythematosus and Sjögren’s disease, which may further broaden the drug’s addressable market, if successful.

Newer therapies like Cobenfy also add optionality to the long-term story, with early launch traction and potential label expansions positioning it as a future growth lever.

The transition is not without challenges. The legacy portfolio — including Eliquis, Revlimid, Pomalyst, Sprycel and Abraxane — still represents 46% of revenues and continues to face significant erosion due to loss of exclusivity for four drugs (Revlimid, Pomalyst, Sprycel and Abraxane).

BMY’s Competition in Oncology Space

Oncology is a key therapeutic area of focus for Bristol Myers, which is developing and delivering transformational medicines in this space.

The company competes with big pharma giants like Merck MRK and Pfizer PFE in this space.

The immuno-oncology space is dominated by pharma giant MRK’s blockbuster drug Keytruda (pembrolizumab).

Keytruda is approved for several types of cancer and alone accounts for around 55% of MRK’s pharmaceutical sales. Merck is currently working on different strategies to drive long-term growth of Keytruda.

Pfizer is one of the largest and most successful drugmakers in the field of oncology. It has an innovative oncology product portfolio of antibody-drug conjugates (ADCs), small molecules, bispecifics and other immune-oncology biologics that treat a wide range of cancers, including breast cancer, gastrointestinal cancer, genitourinary cancer, hematology-oncology, and thoracic cancers, which includes lung cancer.

Pfizer’s position in oncology was strengthened with the addition of Seagen.

The company inked a licensing agreement with 3SBio for the development, manufacturing and commercialization of SSGJ-707, a bispecific antibody targeting PD-1 and VEGF, outside China.

BMY’s Price Performance, Valuation & Estimates

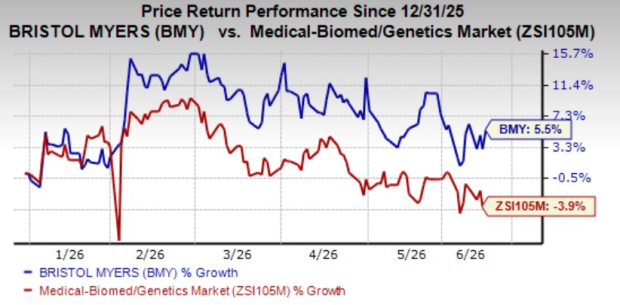

Shares of Bristol Myers have gained 5.5% year to date against the industry’s decline of 3.9%.

Image Source: Zacks Investment Research

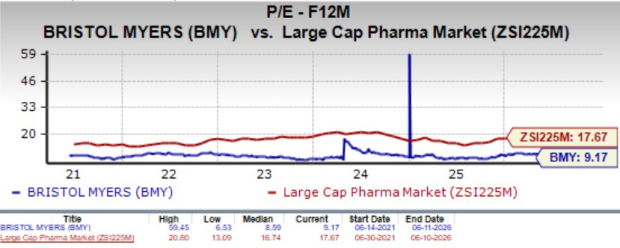

From a valuation standpoint, BMY is trading at a discount to the large-cap pharma industry. Going by the price/earnings ratio, shares currently trade at 9.17x forward earnings, higher than its mean of 8.59x but lower than the large-cap pharma industry’s 17.67x.

Image Source: Zacks Investment Research

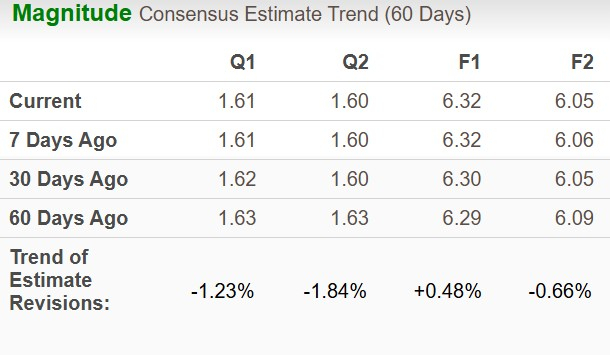

The Zacks Consensus Estimate for 2026 EPS has moved north to $6.32 from $6.29 in the past 60 days, while that for 2027 has moved south to $6.05 from $6.09 in the same time frame.

Image Source: Zacks Investment Research

BMY currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Beyond Nvidia: AI's Second Wave Is Here

The AI revolution has already minted millionaires. But the stocks everyone knows about aren't likely to keep delivering the biggest profits. AI’s second wave is moving from infrastructure to implementation and these companies are at the forefront of this transition, positioned to become what Amazon and Google were to the internet era.

See Stocks Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Bristol Myers Squibb Company (BMY): Free Stock Analysis Report

Pfizer Inc. (PFE): Free Stock Analysis Report

Merck & Co., Inc. (MRK): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).