BP p.l.c. BP is a well-known energy major with operations across upstream and downstream segments of the oil and gas industry. Since BP generates a significant portion of revenues from its upstream operations, the company's business model is highly sensitive to crude oil prices. As a result, fluctuations in crude prices impact BP's revenues, cash flows and margins.

Since late February, geopolitical escalation and the effective closure of the critical Strait of Hormuz have severely constrained global energy supplies, driving crude oil prices to surge. Although a peace deal is anticipated in a few days, West Texas Intermediate (“WTI”) crude prices remain near $80 per barrel, according to oilprice.com. Consequently, BP operates in a highly favorable commodity-price environment that supports elevated profit margins.

The U.S. Energy Information Administration (“EIA”) also projects a sustained favorable pricing environment in its short-term energy outlook also. The EIA estimates that WTI crude prices will average $88.32 per barrel in 2026. This is significantly higher than the $65.40 per barrel recorded in 2025. With WTI prices remaining elevated, BP is well-positioned to leverage its upstream portfolio for stronger cash flows.

Will YPF & CVE Benefit From Higher Crude Prices?

As major energy players focused on exploration and production,YPF Sociedad Anónima YPF and Cenovus Energy Inc. CVE have business models that are exposed to crude price volatility. YPF benefits from high-quality upstream assets concentrated in Argentina’s Vaca Muerta shale, while Cenovus operates a highly diversified portfolio across Canada and the United States. By virtue of these extensive asset bases, YPF and CVE are well-positioned to benefit from elevated crude prices.

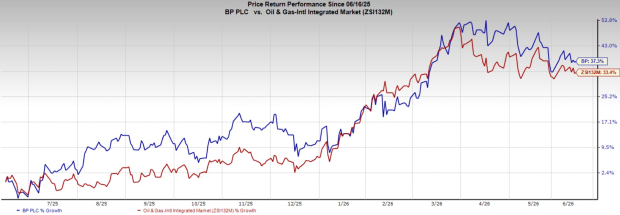

BP’s Price Performance, Valuation & Estimates

BP shares have gained 37.3% over the past year compared with 33.4% growth of the industry.

From a valuation standpoint, BP trades at a trailing 12-month enterprise-value-to-EBITDA (EV/EBITDA) of 3.18X. This is below the broader industry average of 6.4X.

The Zacks Consensus Estimate for BP’s 2026 earnings has remained constant over the past seven days.

Image Source: Zacks Investment Research

BP currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company's customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren't winners but this one could far surpass earlier Zacks' Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

BP p.l.c. (BP): Free Stock Analysis Report

YPF Sociedad Anonima (YPF): Free Stock Analysis Report

Cenovus Energy Inc (CVE): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).