Dollar General Corporation’s DG first-quarter fiscal 2026 results indicate that its margin recovery efforts are gaining momentum. While sales growth remained steady, the more notable development was the continued expansion in profitability, driven by multiple operational initiatives rather than top-line acceleration alone.

Gross margin improved 65 basis points year over year to 31.6%, reflecting benefits from higher inventory markups, lower shrink and reduced inventory damages. These gains more than offset increased markdown activity and higher transportation costs. Management highlighted that shrink mitigation remained a significant contributor, delivering a 28-basis-point reduction versus last year despite already lapping a 61-basis-point improvement in the prior-year quarter.

The improvement was not limited to one area. Dollar General pointed to stronger category management, better inventory controls and lower damages as additional drivers of margin expansion. Management said pricing was not a meaningful contributor to first-quarter markup gains, suggesting the increase stemmed primarily from operational execution rather than broad-based price increases.

The gross margin improvement flowed through to operating results. Operating margin expanded 40 basis points to 5.9%, while operating profit climbed 10.8% year over year. This performance came despite higher-than-anticipated fuel costs, underscoring the strength of the company’s internal margin initiatives.

Management also expressed confidence that margin drivers such as shrink reduction, damage improvement, supply-chain productivity, category management and DG Media Network growth still have room to contribute going forward. The first quarter, therefore, reinforced that Dollar General’s margin expansion story is being supported by a broader and more durable set of operational levers.

How Dollar General Compares With Walmart and Target

Walmart Inc. WMT reported a 6-basis-point increase in the consolidated gross profit rate to 24.3%, supported by favorable merchandise and business mix, including growth in higher-margin advertising operations. At the U.S. segment level, Walmart delivered a 29-basis-point gross margin jump, benefiting from inventory management, digital advertising growth and improved category mix. Management also highlighted that general merchandise contributed favorably to gross margin expansion for the first time in 18 quarters, underscoring the improving profitability profile at Walmart.

Meanwhile, Target Corporation TGT posted a first-quarter gross margin rate of 29%, up from 28.2% a year ago. The improvement was driven by lower markdown rates, stronger advertising and other non-merchandise revenue streams, and better productivity across supply chain facilities. Target also expanded its adjusted operating margin rate to 4.5% from 3.7% last year, reflecting the benefits of improved merchandise profitability. While Target continues to invest in labor, training and marketing, its latest results indicate that operational improvements are helping offset these costs.

What the Latest Metrics Say About Dollar General

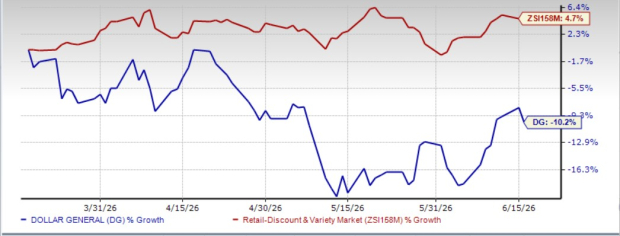

Dollar General has seen its shares tumble 10.2% over the past three months against the industry’s rise of 4.7%.

Image Source: Zacks Investment Research

From a valuation standpoint, Dollar General's forward 12-month price-to-earnings ratio stands at 14.97, lower than the industry’s ratio of 32.05. However, it is trading below its 12-month median level of 17.29.

Image Source: Zacks Investment Research

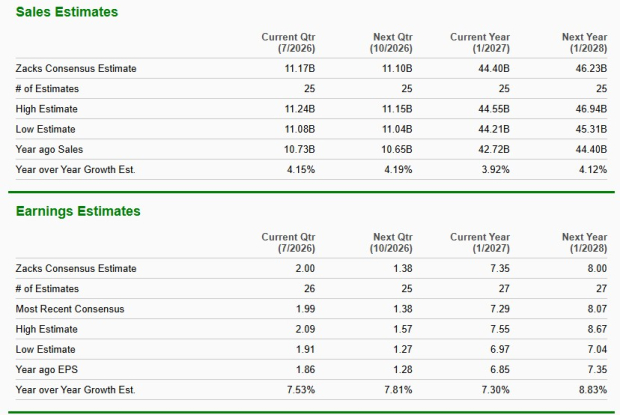

The Zacks Consensus Estimate for Dollar General’s current financial-year sales and earnings per share implies year-over-year growth of 3.9% and 7.3%, respectively. For the next fiscal year, the consensus estimate indicates a 4.1% rise in sales and 8.8% growth in earnings.

Image Source: Zacks Investment Research

Dollar General currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Beyond Nvidia: AI's Second Wave Is Here

The AI revolution has already minted millionaires. But the stocks everyone knows about aren't likely to keep delivering the biggest profits. AI’s second wave is moving from infrastructure to implementation and these companies are at the forefront of this transition, positioned to become what Amazon and Google were to the internet era.

See Stocks Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Target Corporation (TGT): Free Stock Analysis Report

Walmart Inc. (WMT): Free Stock Analysis Report

Dollar General Corporation (DG): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).