Jabil Inc. JBL used its third-quarter fiscal 2026 earnings call to press a more ambitious AI growth case, while also lifting its full-year outlook. Management’s message centered less on the quarter’s beat and more on how capacity, customer wins and mix could drive the next leg of expansion.

The setup for fiscal 2027 was the clearest takeaway. Executives pointed to another year of AI-led growth, rising margins and disciplined capital spending, even as they acknowledged supply chain constraints and plant ramps still need to be managed carefully.

JBL Leans Harder Into AI Demand

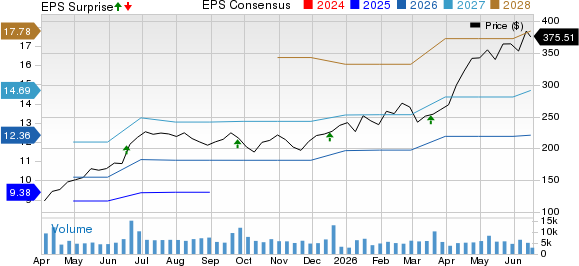

Chief financial officer Gregory Hebard said third-quarter revenues rose to about $8.75 billion, up 12% year over year, while core earnings per share climbed to $3.16 from $2.55 a year earlier. Those results came in above the Zacks Consensus Estimate of $8.63 billion for revenues and $3.12 for EPS, reflecting a surprise of 1.4% and 1.3%, respectively.

Jabil, Inc. Price, Consensus and EPS Surprise

Jabil, Inc. price-consensus-eps-surprise-chart | Jabil, Inc. Quote

Hebard stressed that the upside was broad-based across revenues, margin and free cash flow, rather than driven by one isolated pocket of strength. Core operating margin reached 5.8% in the quarter, with Intelligent Infrastructure standing out at 6.1%.

Chief executive officer Mike Dastoor built on that point, saying AI infrastructure demand remained extremely strong and that Jabil’s full-year AI-related revenue outlook is now materially above where management stood 90 days earlier.

Jabil Raises 2026 Targets Again

The company raised its fiscal 2026 outlook to about $35 billion in revenues, roughly 5.8% core operating margin, about $12.7 in core EPS and more than $1.4 billion in adjusted free cash flow. That compares with the prior view for $34 billion in revenues and more than $1.3 billion in free cash flow.

For the fourth quarter, Hebard guided for revenues of $9.2-$10 billion and core EPS of $3.8-$4.2, with core operating margin around 6.4% at the midpoint. Management tied that outlook to continued AI program strength, customer ramp timing and improving conditions in automotive and some consumer-linked areas.

The message was not simply that estimates moved up. Jabil believes its diversified model is now producing faster growth, a better mix and stronger cash generation at the same time.

JBL Sees AI Growth Carrying Into 2027

Dastoor’s most important forward-looking statement was that AI-related revenues should grow in fiscal 2027 at a percentage rate similar to fiscal 2026, but off a much larger base. AI-related revenues are now expected to reach about $13.6 billion this year, up from $9 billion in fiscal 2025.

He also said Jabil won a third hyperscale customer in the third quarter. In Q&A, Dastoor told a Goldman Sachs analyst that the new hyperscaler could contribute a few hundred million dollars in fiscal 2027 and scale to $1 billion and beyond in fiscal 2028.

That early 2027 signal came with limits. Dastoor cautioned that final full-year guidance will depend on component availability, mix, ramp timing, free cash flow priorities and portfolio choices, with fuller numbers coming at Jabil’s September investor briefing.

Jabil Expands Capacity Without Chasing an OEM Model

A JPMorgan analyst pressed management on the sharp step-up implied in fourth-quarter Intelligent Infrastructure revenues. Dastoor said about a couple hundred million dollars of finished goods slipped from the third quarter into the fourth quarter, while another roughly $300 million of upside is spread across the business rather than tied only to the third hyperscaler.

Capacity was another focal point. Hebard said Jabil is adding roughly 10% to its global footprint and still expects total capital spending to remain within 1.5% to 2% of revenues, reinforcing management’s asset-light framing.

Dastoor said new capacity is coming online in North Carolina, Memphis, India and other locations, with North Carolina expected to ramp through early calendar 2027. He also framed the proposed Adani partnership in India as a longer-term fiscal 2028 opportunity tied to AI racks, servers, networking and power infrastructure.

JBL Uses Q&A to Defend Margins

Questions from Fox Advisors and Stifel centered on whether new plants and customer ramps could dilute profitability. Dastoor acknowledged some temporary ramp inefficiencies but said the mix is improving, utilization should rise through fiscal 2027, and higher-value offerings such as power, liquid cooling and silicon photonics are helping the margin profile.

He went further in Q&A than in the prepared remarks, saying he is confident Jabil can move to 6%-plus core operating margin in fiscal 2027. Hebard added that fourth-quarter seasonality tends to make the fourth quarter the strongest margin period, so investors should not read that run rate as the full shape of next year.

A Barclays analyst also asked about supply chain risk. Dastoor said shortages remain a factor in areas such as high-bandwidth memory and certain interconnect components, but he indicated those constraints are already reflected in management’s thinking for fiscal 2027.

Jabil Leaves Investors With a Growth Blueprint

Coming out of the call, management’s tone was confident but measured. The company highlighted strong AI demand, improving performance in automotive and Connected Living, and a model that it believes can support faster growth without a sharp jump in capital intensity.

The bigger point was strategic. Dastoor repeatedly framed Jabil as expanding through capabilities across compute, storage, networking, power and cooling, rather than moving toward a product-heavy OEM structure. That posture shaped both the fiscal 2027 commentary and the way management discussed new hyperscaler and India opportunities.

JBL’s Zacks Signals Still Favor the Bull Case

JBL currently carries a Zacks Rank #2 (Buy), along with a Value Score of C, Growth Score of B, Momentum Score of A and VGM Score of A. A Zacks Rank #1 (Strong Buy) or 2 stock paired with a Style Score of A or B offers the strongest near-term performance profile, while the VGM Score reflects a blended view of value, growth and momentum traits. You can see the complete list of today’s Zacks #1 Rank stocks here.

That combination suggests JBL’s strongest signal comes from momentum and its all-around VGM profile rather than pure value. Even so, the Zacks Rank can change as earnings estimate revisions adjust after the quarter, so the current setup is best viewed as a favorable but still fluid signal.

Research Chief Names "Single Best Pick to Double"

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

This company targets millennial and Gen Z audiences, generating nearly $1 billion in revenue last quarter alone. A recent pullback makes now an ideal time to jump aboard. Of course, all our elite picks aren’t winners but this one could far surpass earlier Zacks’ Stocks Set to Double like Nano-X Imaging which shot up +129.6% in little more than 9 months.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Jabil, Inc. (JBL): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).