Target Corporation TGT stock has witnessed an impressive rally so far this year, reflecting renewed investor confidence in the retail giant’s growth prospects and operational resilience. Target, which competes with Walmart Inc. WMT, Costco Wholesale Corporation COST and Dollar General Corporation DG, has benefited from improving traffic trends, disciplined inventory management, a stronger merchandising strategy and ongoing investments in its omnichannel capabilities.

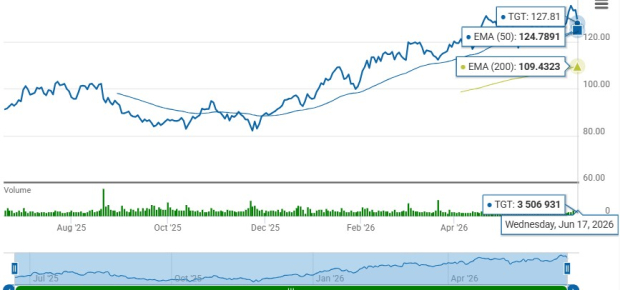

Closing yesterday’s trading session at $127.81, Target Corporation has rallied 30.7% year to date compared with the industry’s rise of 14.1% and the S&P 500’s gain of 10%. The stock has also surpassed key retail peers, with Walmart and Costco up 6% and 11.9%, while Dollar General has declined 18.2%.

TGT Year-to-Date Stock Performance

Image Source: Zacks Investment Research

The key question now is whether there is further room to run, or if investors should begin taking profits after the strong move.

While the fundamental story remains encouraging, the stock’s recent move also warrants a look at its technical setup. Momentum indicators can help investors assess whether Target’s rally is still supported by market strength, or if the stock may be approaching a pause after its sharp advance.

Does Target’s Technical Momentum Suggest More Upside?

Target’s technical setup remains supportive, with the stock trading above its 50-day moving average of $124.79, signaling strong near-term momentum. TGT is also trading above its 200-day moving average of $109.43, suggesting that the recent rally is backed by a broader uptrend rather than a short-lived spike.

Image Source: Zacks Investment Research

Decoding Target

Target has emerged as one of the most compelling turnaround stories in retail, supported by a clear strategic vision, strengthening customer engagement, and a renewed focus on long-term growth. The company is executing a broad transformation centered on merchandising, store operations, digital capabilities and customer experience. These initiatives are resonating with consumers, positioning Target to capture market share and drive sustainable growth.

One of the most encouraging aspects of Target is the strength of its merchandising strategy. Management has sharpened its focus on high-opportunity categories such as beauty, health and wellness, food, baby, home and toys, where the company enjoys strong brand credibility and consumer loyalty. By introducing new products, refreshing assortments more frequently and creating trend-driven offerings that appeal to families and younger shoppers, Target is rebuilding its reputation as a destination for style and value. Target added around 1,500 new health and wellness items and plans to refresh about 40% of that assortment this year while introducing 3,000 new food items.

Target’s omnichannel ecosystem remains another major competitive advantage. The company has successfully integrated its stores, digital platforms and fulfillment capabilities into a seamless shopping experience that meets customers wherever they choose to shop. Same-day fulfillment services, digital growth initiatives and membership offerings are driving stronger customer engagement while reinforcing convenience and loyalty. At the same time, Target’s extensive store network serves as both a shopping destination and a fulfillment engine, allowing the company to deliver speed and efficiency while maintaining attractive economics.

The company continues to expand its store footprint, remodel existing locations and invest in high-return growth opportunities across its business. At the same time, it benefits from a growing mix of higher-margin revenue streams, including advertising, marketplace services and membership programs, which provide additional earnings diversification beyond traditional retail sales. Combined with a strong balance sheet, a long history of returning capital to shareholders and management’s confidence in the company’s long-term outlook, these factors make Target an attractive investment opportunity for investors seeking a blend of growth, profitability and durable competitive advantages.

Target now expects net sales growth of around 4% for fiscal 2026 compared with its earlier expectation of about 2% growth. However, management noted that Target faced its easiest comparison in the first quarter and will face a tough comparison in the second quarter, including the anniversary of last year’s Nintendo Switch 2 launch. Management further suggested that higher tax refunds likely helped consumer spending in the first quarter, with that benefit expected to fade over the rest of the year.

Here’s How Estimates Shape Up for Target

Over the past 30 days, the Zacks Consensus Estimate for the current fiscal year has risen by 30 cents to $8.35. For the current quarter, the consensus estimate has increased by 34 cents to $8.89.

Image Source: Zacks Investment Research

Does Target Tick the Boxes for Value Investing?

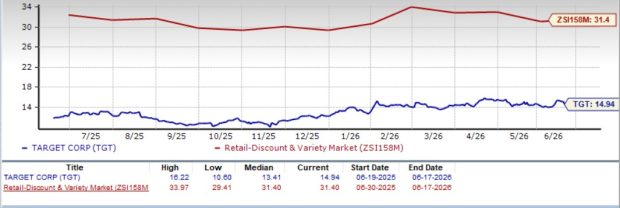

Target is currently trading at a forward 12-month price-to-earnings (P/E) ratio of 14.94. This represents a meaningful discount to the broader industry average of 31.40 and remains fairly below the S&P 500’s forward multiple of 21.34. However, the stock is trading above its one-year median P/E of 13.41.

Target is trading at a discount to Walmart (with a forward 12-month P/E ratio of 38.98) and Costco (43.82) but at a premium to Dollar General (14.31).

Image Source: Zacks Investment Research

How to Play Target Stock: Buy, Hold or Take Profits?

Target’s rally appears well-supported by improving fundamentals, stronger execution and a clearer long-term strategy, but the sharp year-to-date gain leaves less room for error. The company’s merchandising reset, omnichannel strength, store investments and improving earnings outlook make the stock attractive for long-term investors, while its discounted valuation versus retail peers adds to the appeal. However, tougher comparisons ahead, fading consumer tailwinds and ongoing execution risks suggest that chasing the stock aggressively after its strong run may not be prudent. Current investors may consider holding the stock to participate in the turnaround, while new investors could look for a better entry point or accumulate gradually on pullbacks rather than buying all at once.

Target currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Radical New Technology Could Hand Investors Huge Gains

Quantum Computing is the next technological revolution, and it could be even more advanced than AI.

While some believed the technology was years away, it is already present and moving fast. Large hyperscalers, such as Microsoft, Google, Amazon, Oracle, and even Meta and Tesla, are scrambling to integrate quantum computing into their infrastructure.

Senior Stock Strategist Kevin Cook reveals 7 carefully selected stocks poised to dominate the quantum computing landscape in his report, Beyond AI: The Quantum Leap in Computing Power .

Kevin was among the early experts who recognized NVIDIA's enormous potential back in 2016. Now, he has keyed in on what could be "the next big thing" in quantum computing supremacy. Today, you have a rare chance to position your portfolio at the forefront of this opportunity.

See Top Quantum Stocks Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Target Corporation (TGT): Free Stock Analysis Report

Walmart Inc. (WMT): Free Stock Analysis Report

Dollar General Corporation (DG): Free Stock Analysis Report

Costco Wholesale Corporation (COST): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).