American Eagle Outfitters, Inc. AEO has a valuation that can draw attention, but the investment case is not one-sided. Aerie is growing quickly, profitability is improving and full-year guidance points to further recovery.

The caution is just as visible. Tariffs, higher advertising spend and softer American Eagle brand trends keep the stock in a balanced risk-reward setup.

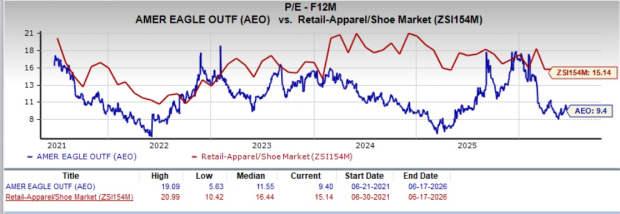

AEO Looks Cheap on Forward Earnings

AEO trades at 9.4X forward 12-month earnings, below the Zacks sub-industry at 15.14X. The stock also sits below its five-year median multiple of 11.6X, giving investors a valuation discount to consider.

That discount can become more meaningful if execution improves across the portfolio. Abercrombie & Fitch Co. ANF and Gap Inc. GAP also sit in the specialty apparel conversation, where investors are weighing brand heat, consumer demand and margin durability.

Image Source: Zacks Investment Research

A lower multiple alone does not make AEO a buy. It does, however, create a clearer path for rerating if the company converts Aerie’s growth and cost actions into steadier operating income.

American Eagle Has Better Profit Potential

First-quarter fiscal 2026 results showed that the profit base is improving. Revenues rose 10% year over year to $1.20 billion, while earnings of 14 cents per share topped the Zacks Consensus Estimate of 11 cents.

Gross margin expanded to 38.2%, up 860 basis points from the prior-year period. Merchandise margins improved 710 basis points, helped by the comparison with last year’s inventory write-down.

Buying, occupancy and warehousing costs leveraged 150 basis points on higher sales and cost-optimization efforts. AEO also swung to operating income of $28 million from an operating loss of $85 million a year earlier.

AEO Guidance Supports the Bull Case

The forward view supports the argument that profit recovery is not only a first-quarter event. For fiscal 2026, management expects comparable sales to rise in the mid-single digits and operating income of $390 million to $410 million.

The second-quarter outlook also points to positive earnings momentum. AEO expects operating income of $45 million to $50 million, despite tariff costs and planned advertising investments.

This guidance matters because the market is not just evaluating Aerie’s current momentum. Investors are also testing whether AEO can convert better sales, tighter costs and stronger inventory discipline into more consistent profitability.

American Eagle Outfitters, Inc. Price, Consensus and EPS Surprise

American Eagle Outfitters, Inc. price-consensus-eps-surprise-chart | American Eagle Outfitters, Inc. Quote

American Eagle’s Risks Can Limit Upside

The risk side starts with the American Eagle brand. First-quarter revenues and comparable sales for the brand declined 2%, with weakness concentrated in women’s bottoms, including denim.

Management is refining the bottom's architecture and using chase capabilities ahead of back-to-school. Until those actions show broader traction, AE’s softer store conversion and category misses remain watch points.

Tariffs are another pressure point. Management expects tariffs to hurt the second-quarter gross margin by 150-200 basis points, while total ending inventory rose 27% at cost with units up only 5%.

Selling, general and administrative expenses are also moving higher. They rose 11% in the first quarter, and the second-quarter outlook calls for mid-teens growth, primarily tied to continued advertising investments.

AEO’s Rating Signals Fit a Hold Debate

The bottom line is that this Zacks Rank #3 (Hold) company looks more interesting than clean. The valuation discount and profit recovery are real positives, but tariffs, advertising costs and the AE brand reset keep the setup from looking like an unqualified buy. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

For investors using Zacks tools, the Zacks Rank and Zacks Style Scores should serve as confirmation points. A favorable Zacks Rank, particularly Zacks Rank #1 or Zacks Rank #2 (Buy), paired with Style Scores of A or B, would strengthen the case for fresh buying interest.

A Zacks Rank #3 profile would fit the current debate better, as it would suggest a stock that merits monitoring while execution risk remains. Weaker rank signals or soft Style Scores would argue for patience, even with the shares trading at a discount.

Research Chief Names "Single Best Pick to Double"

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

This company targets millennial and Gen Z audiences, generating nearly $1 billion in revenue last quarter alone. A recent pullback makes now an ideal time to jump aboard. Of course, all our elite picks aren’t winners but this one could far surpass earlier Zacks’ Stocks Set to Double like Nano-X Imaging which shot up +129.6% in little more than 9 months.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Abercrombie & Fitch Company (ANF): Free Stock Analysis Report

American Eagle Outfitters, Inc. (AEO): Free Stock Analysis Report

The Gap, Inc. (GAP): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).