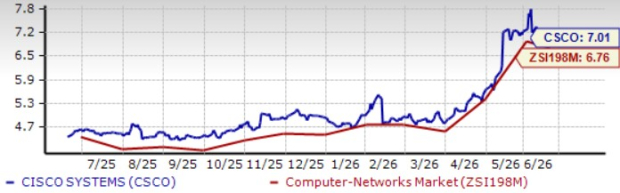

Cisco Systems CSCO shares are trading at a premium, as suggested by the Value Score of F. In terms of the forward 12-month price/sales, CSCO is trading at a premium of 7.01X, higher than the Zacks Computer Networking industry’s 6.76X and Hewlett Packard Enterprise’s HPE 1.3X. However, Cisco shares are trading at a discount compared with Arista Networks ANET and Broadcom AVGO. In terms of the forward 12-month P/S, Arista Networks and Broadcom shares are trading at 16.78X and 13.61X, respectively.

CSCO Stock’s Valuation

Image Source: Zacks Investment Research

So, is the Cisco stock a buy at this level? Let’s find out.

AI Push & Strong Networking Portfolio Aids Cisco’s Prospects

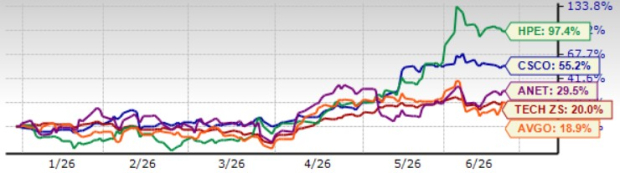

Year to date (YTD), CSCO shares have appreciated 55.2%, outperforming the broader Zacks Computer & Technology sector, as well as Broadcom and Arista Networks, but lagging Hewlett Packard Enterprise. The broader sector, Hewlett Packard Enterprise, Arista Networks and Broadcom have jumped 20%, 97.4%, 29.5% and 18.9%, respectively, over the same time frame.

CSCO Stock’s Price Performance

Image Source: Zacks Investment Research

The outperformance can be attributed to strong AI revenues. Cisco raised its fiscal 2026 AI infrastructure order target from $5 billion to approximately $9 billion, reflecting stronger-than-expected hyperscaler demand. YTD, AI infrastructure orders have already reached $5.3 billion, exceeding the original annual target with one quarter remaining. The company expects to recognize approximately $4 billion in AI infrastructure revenues from hyperscalers in fiscal 2026. Cisco expects at least $6 billion of AI-related revenues in fiscal 2027, indicating strong visibility into future growth.

Cisco is benefiting from a multi-year networking refresh cycle as third-quarter fiscal 2026 enterprise data center switching orders grew more than 40%, campus networking orders reached record levels, and wireless orders increased more than 40% year over year. CSCO believes AI-driven traffic growth will force enterprises to modernize networks over the next several years. The Acacia optics business generated more than $1 billion of orders in the third quarter of fiscal 2026 and is expected to grow over 200% in fiscal 2026, positioning Cisco to capture a larger share of AI networking spend.

The company’s refreshed security portfolio is gaining traction, with double-digit order growth in core security products and strong firewall momentum. The company is leveraging its unique position across networking, security, identity, and observability to address emerging AI security needs, including agentic AI security, AI Defense, Hypershield, and Zero Trust Access. Cisco’s management noted five consecutive quarters of high firewall win rates and expects security growth to improve exiting fiscal 2026.

Cisco’s proprietary Silicon One architecture has been a key differentiator. The company has secured multiple hyperscaler design wins and expects all high-end systems across its portfolio to be powered by Silicon One by fiscal 2029.

CSCO Offers Positive Q4 & FY26 Guidance

Cisco expects non-GAAP earnings between $1.16 per share and $1.18 per share for the fourth quarter of fiscal 2026. Revenues are expected to be in the range of $16.7-$16.9 billion.

The Zacks Consensus Estimate for CSCO’s fourth-quarter fiscal 2026 revenues is pegged at $16.85 billion, indicating growth of 14.9% on a year-over-year basis. The consensus mark for CSCO’s earnings is currently pegged at $1.17 per share, unchanged over the past 30 days, indicating year-over-year growth of 18.2%.

Cisco Systems, Inc. Price and Consensus

Cisco Systems, Inc. price-consensus-chart | Cisco Systems, Inc. Quote

For fiscal 2026, CSCO expects revenues to be in the $62.8-$63 billion range compared with $56.7 billion reported in fiscal 2025. Non-GAAP earnings are expected between $4.27 per share and $4.29 per share compared with $3.81 per share reported in fiscal 2025.

The Zacks Consensus Estimate for CSCO’s fiscal 2026 revenues is pegged at $62.95 billion, indicating growth of 11.1% from fiscal 2025. The consensus mark for CSCO’s fiscal 2026 earnings is currently pegged at $4.28 per share, up by a penny over the past 30 days, indicating year-over-year growth of 12.3%.

Here’s Why CSCO Stock is a Buy Right Now

Cisco is emerging as a major beneficiary of AI infrastructure spending, enterprise network modernization, AI security adoption, and its differentiated Silicon One platform. The company is seeing some of the strongest demand trends in its history, with broad-based order growth across networking, AI infrastructure, optics, and security. These trends are expected to help the stock rally and bode well for CSCO’s long-term prospects. These also justify the current premium valuation.

CSCO currently carries a Zacks Rank #2 (Buy), suggesting that it is the right time to start accumulating the stock. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company's customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren't winners but this one could far surpass earlier Zacks' Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Cisco Systems, Inc. (CSCO): Free Stock Analysis Report

Broadcom Inc. (AVGO): Free Stock Analysis Report

Arista Networks, Inc. (ANET): Free Stock Analysis Report

Hewlett Packard Enterprise Company (HPE): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).