About the Industry

The Zacks Oil and Gas - US E&P industry consists of companies primarily based in the domestic market and focused on the exploration and production (E&P) of oil and natural gas. These firms find hydrocarbon reservoirs, drill oil and gas wells, and produce and sell these materials to be refined later into products such as gasoline, fuel oil, distillate, etc. The economics of oil and gas supply and demand are the fundamental drivers of this industry. In particular, a producer’s cash flow is primarily determined by the realized commodity prices. In fact, all E&P companies' results are vulnerable to historically volatile prices in the energy markets. A change in realizations affects their returns, causing them to alter their production growth rates. The E&P operators are also exposed to exploration risks where drilling results are comparatively uncertain.

4 Key Trends to Watch in the Oil and Gas - US E&P Industry

Higher Oil Prices Can Quickly Lift Cash Flow : The U.S. exploration and production industry remains highly sensitive to oil prices. When crude prices rise, producers usually see a direct benefit because each barrel sold brings in more cash. That can improve margins, fund drilling, support debt reduction and leave more room for shareholder returns. Current geopolitical tensions also keep attention on energy security and a reliable domestic supply. This helps U.S. producers because local barrels become more valuable when global supply feels uncertain. For investors, the key attraction is simple: if oil stays firm, many producers can generate strong free cash flow without needing aggressive production growth.

Rising Costs and Obligations Limit Upside : The industry still faces meaningful cost and liability pressures. Diesel, power, equipment, labor, maintenance, workovers and facility upgrades can become more expensive when activity improves or oil prices rise. Offshore operators also carry large decommissioning and asset-retirement obligations, which can absorb cash that might otherwise go to growth or shareholder returns. Some producers are still focused on reducing debt, so stronger cash flow may be directed toward balance-sheet repair instead of aggressive drilling. For investors, this creates a practical limit on upside. Higher commodity prices help, but they do not remove the need for spending discipline and careful liability management.

Better Efficiency Supports Returns Through Cycles : A more disciplined operating model is becoming a strength for U.S. exploration and production companies. Many producers are focusing less on growth at any cost and more on lower spending, better well performance, workovers, recompletions and selective infrastructure upgrades. This can make each dollar of capital work harder. Low-decline assets are also useful because they require less spending just to keep production steady. For investors, this matters because the industry can create value even when commodity prices are choppy. Strong cost control, careful capital allocation and a focus on free cash flow can make earnings more durable over time.

Weak Natural Gas Prices to Drag Results : Not every part of the commodity mix is supportive. In some U.S. basins, natural gas prices have been weak, and local pricing can sometimes fall far below benchmark levels. This can force producers to curtail gas volumes or accept poor realized prices. Even oil-focused companies can feel the pressure because many wells produce associated gas along with crude. Lower gas and NGL values can reduce total revenue per barrel of oil equivalent and hurt reported production economics. For investors, the risk is that strong oil prices may not fully offset weak gas markets, especially in areas with limited takeaway capacity.

Zacks Industry Rank Indicates Positive Outlook

The Zacks Oil and Gas - US E&P industry is a 34-stock group within the broader Zacks Oil - Energy sector. The industry currently carries a Zacks Industry Rank #104, which places it in the top 42% of 247 Zacks industries.

The group’s Zacks Industry Rank, which is basically the average of the Zacks Rank of all the member stocks, indicates fairly strong near-term prospects. Our research shows that the top 50% of the Zacks-ranked industries outperforms the bottom 50% by a factor of more than 2 to 1.

The industry’s position in the top 50% of the Zacks-ranked industries is a result of improving earnings outlook for the constituent companies in aggregate. Looking at the aggregate earnings estimate revisions, it appears that analysts are becoming optimistic about this group’s earnings growth potential. As a matter of fact, the industry’s earnings estimates for 2026 have gone up 34.6% in the past year.

Considering the encouraging dynamics of the industry, we will present a few stocks that you may want to consider for your portfolio. But it’s worth taking a look at the industry’s shareholder returns and current valuation first.

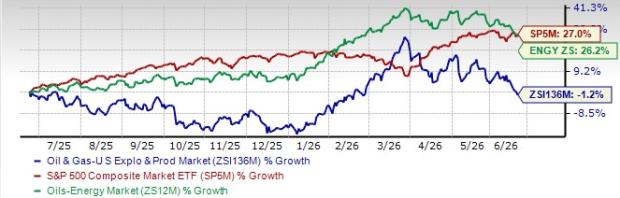

Industry Underperforms Sector and S&P 500

The Zacks Oil and Gas - US E&P industry has fared worse than the broader Zacks Oil - Energy Sector and the Zacks S&P 500 composite over the past year.

The industry has moved down 1.2% over this period against the broader sector’s increase of 26.2%. Meanwhile, the S&P 500 has gained some 27%.

One-Year Price Performance

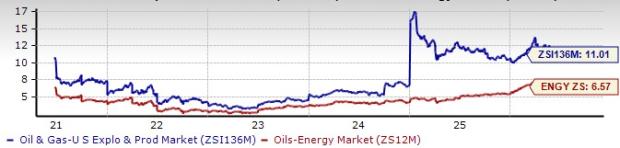

Industry's Current Valuation

Since oil and gas companies are debt-laden, it makes sense to value them based on the EV/EBITDA (Enterprise Value/ Earnings before Interest Tax Depreciation and Amortization) ratio. This is because the valuation metric takes into account not just equity but also the level of debt. For capital-intensive companies, EV/EBITDA is a better valuation metric because it is not influenced by changing capital structures and ignores the effect of noncash expenses.

On the basis of the trailing 12-month enterprise value-to-EBITDA (EV/EBITDA), the industry is currently trading at 11.01X, lower than the S&P 500’s 18.62X. It is, however, well above the sector’s trailing 12-month EV/EBITDA of 6.57X.

Over the past five years, the industry has traded as high as 17.10X and as low as 3.42X, with a median of 6.08X.

Trailing 12-Month Enterprise Value-to EBITDA (EV/EBITDA) Ratio (Past Five Years)

3 Stocks to Focus On

W&T Offshore: W&T Offshore is a Houston-based oil and gas company focused on the Gulf of America. Founded in 1983 by Tracy Krohn, it has been listed on the NYSE since 2005 under the ticker WTI. Over four decades, the Zacks Rank #2 (Buy) company has grown from a small independent operator into a seasoned offshore player, mainly through acquisitions and selective drilling.

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

The company operates across 48 offshore fields and holds a large acreage base in shallow and deepwater areas. Its strategy is simple: improve existing assets, control costs, add reserves, and pursue smart acquisitions. With strong technical experience, operating production, and a focus on cash flow, W&T Offshore aims to support steady long-term growth.

The Zacks Consensus Estimate for the company’s 2026 earnings per share indicates 67.6% year-over-year growth. Over the past 60 days, the Zacks Consensus Estimate for W&T Offshore’s 2026 loss has narrowed from 32 cents per share to 12.

Price and Consensus: WTI

Ring Energy: Ring Energy is a Texas-based oil and gas company focused on conventional assets in the Permian Basin, mainly the Central Basin Platform and Northwest Shelf. It uses modern drilling and completion methods to improve older fields, extend well life and raise recovery. The #2 Ranked company operates more than 96,000 net acres and has built a large, mostly operated asset base.

Its strategy centers on steady cash flow, disciplined spending and lower operating costs. Ring has more than 500 identified drilling locations, over 10 years of inventory and a reserve life above 20 years. Recent results show production in line with guidance, cost reductions and continued positive adjusted free cash flow.

The Zacks Consensus Estimate for the company’s 2026 earnings per share indicates 57.9% year-over-year growth. Over the past 60 days, the Zacks Consensus Estimate for Ring Energy’s 2026 earnings has moved up from 22 cents per share to 30 cents.

Price and Consensus: REI

APA: APA Corporation explores for and produces oil and natural gas through subsidiaries in the United States, Egypt and the United Kingdom, while also pursuing offshore opportunities in Suriname and other areas. Its portfolio is anchored by the Permian Basin and Egypt, giving the Zacks Rank #3 (Hold) company a steady operating base and room for long-term growth.

APA focuses on safe, efficient and responsible operations, backed by financial discipline. It plans to return at least 60% of free cash flow to investors through dividends and share buybacks, while reducing debt. Growth plans include first oil from Suriname’s GranMorgu project in mid-2028 and continued cost savings across operations.

The Zacks Consensus Estimate for the company’s 2026 earnings per share indicates 48.5% year-over-year growth. Over the past 60 days, the Zacks Consensus Estimate for APA’s 2026 earnings has moved up from $4.28 per share to $5.60.

Price and Consensus: APA

Research Chief Names "Single Best Pick to Double"

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

This company targets millennial and Gen Z audiences, generating nearly $1 billion in revenue last quarter alone. A recent pullback makes now an ideal time to jump aboard. Of course, all our elite picks aren’t winners but this one could far surpass earlier Zacks’ Stocks Set to Double like Nano-X Imaging which shot up +129.6% in little more than 9 months.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

APA Corporation (APA): Free Stock Analysis Report

W&T Offshore, Inc. (WTI): Free Stock Analysis Report

Ring Energy, Inc. (REI): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).