The e-commerce industry continues to evolve rapidly as businesses of all sizes increasingly rely on digital storefronts to reach customers. Against this backdrop, Shopify Inc. SHOP and Wix.com Ltd. WIX have emerged as two prominent players, helping merchants build, manage and grow their online presence.

While Shopify has established itself as a leading commerce platform with a strong ecosystem of merchants, payment solutions and fulfillment capabilities, Wix has gained traction through its user-friendly website-building tools and expanding e-commerce offerings. Both companies are benefiting from the ongoing shift toward online selling, but their growth strategies, financial performance and market opportunities differ significantly. As investors look for exposure to the expanding digital commerce market, the question remains: which of these two stocks is currently in a stronger position to deliver long-term value?

The Case for SHOP

Shopify continues to demonstrate exceptional growth at a scale few e-commerce companies can match. In the first quarter of 2026, gross merchandise volume (“GMV”) increased 35% year over year to $101 billion, marking the second consecutive quarter in which merchants sold more than $100 billion worth of goods on the platform. Revenues climbed 34%, while free cash flow reached $476 million. Growth was broad-based across merchant sizes, geographies and sales channels, highlighting the strength of Shopify's ecosystem.

The company is also gaining traction among larger merchants, with the number of businesses generating more than $100 million in annual GMV nearly doubling over the last two years. These trends suggest Shopify is successfully expanding beyond its small-business roots and capturing a larger share of enterprise commerce.

Shopify is positioning itself as a major beneficiary of the AI-driven transformation in commerce. The company has integrated artificial intelligence across its platform, helping merchants automate store management, marketing and operational tasks. Its AI assistant, Sidekick, is seeing strong adoption, with weekly active shops using the tool increasing fourfold year over year.

Management believes Shopify's 20 years of commerce data, spanning millions of merchants and billions of products, provides a significant advantage in building AI-powered solutions. As entrepreneurship becomes more accessible through AI, Shopify expects a larger pool of merchants to enter the market, creating a long-term growth opportunity for the platform.

Shopify's opportunity extends well beyond website creation. The company continues to deepen merchant relationships through payments, financial services, advertising and AI-powered shopping channels. Shopify Payments processed $67 billion in GMV during the quarter, while Shop Pay volume jumped 59% year over year. It is also benefiting from emerging AI commerce channels, with AI-driven traffic to Shopify stores rising eightfold and orders generated through AI searches increasing nearly thirteenfold from the prior year. These initiatives strengthen merchant retention, increase monetization opportunities and reinforce Shopify's position as a comprehensive commerce platform rather than simply an e-commerce software provider.

Despite its strong momentum, Shopify faces growing execution challenges as the commerce landscape evolves. The company is making significant investments in AI-driven commerce, betting that new shopping experiences powered by platforms such as ChatGPT and other AI agents will accelerate merchant growth. However, the pace and economics of this shift remain uncertain. Competition from technology giants, payment providers and other commerce platforms is intensifying as AI reshapes how consumers discover and purchase products.

In addition, Shopify's transaction-based business model remains tied to merchant sales activity, making it vulnerable to slowdowns in consumer spending. To justify its growth narrative, Shopify must continue to attract merchants, expand enterprise adoption and successfully monetize new AI-powered commerce opportunities.

The Case for WIX

Wix is rapidly strengthening its position in the AI-powered website creation market. Management believes the company's two decades of experience in web creation, extensive infrastructure and integrated product ecosystem provide a durable competitive advantage as AI reshapes the industry. During the quarter, Wix introduced its own proprietary large language model to power Wix Harmony, the AI website-building platform.

According to management, the internally developed model delivers faster performance, better user outcomes and lower operating costs than third-party alternatives. Harmony is already helping improve user conversion rates and driving stronger adoption of premium subscriptions and business solutions, reinforcing Wix's ability to monetize AI innovation.

Wix's acquisition of Base44 is creating a meaningful new avenue for growth. The AI-powered application creation platform reached $150 million in annual recurring revenues by mid-May, up sharply from $100 million in early March. Management highlighted strong user demand, improving retention trends and growing monetization across the platform. Base44 is also expanding Wix's addressable market beyond traditional website creation by enabling entrepreneurs and businesses to build custom applications. Combined with healthy cohort performance, higher subscription conversions and strong retention among existing users, Base44 gives Wix another growth driver that could support revenue expansion and market-share gains in the years ahead.

Despite the encouraging AI momentum, Wix continues to face challenges in its partner business. Management acknowledged that partner-related growth slowed more than expected due to smaller customer cohorts and reduced marketing spending in recent quarters. In addition, gross payment volume growth remained soft as small and medium-sized businesses on the platform continued to face macroeconomic pressure. While Wix expects new AI products and platform enhancements to reaccelerate growth eventually, execution risks remain as it works to revive partner momentum and navigate a still-uncertain economic environment.

How Does the Consensus Estimate Compare for SHOP & WIX?

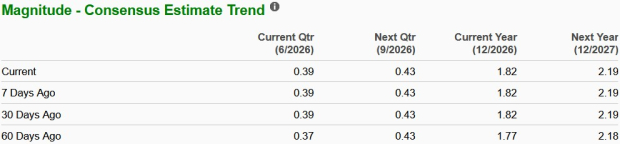

The Zacks Consensus Estimate for Shopify’s 2026 sales and earnings per share (EPS) indicates year-over-year increases of 27.3% and 55.6%, respectively. In the past 60 days, earnings estimates for 2026 have increased from $1.77 to $1.82 per share.

SHOP Earnings Estimate Trend

Image Source: Zacks Investment Research

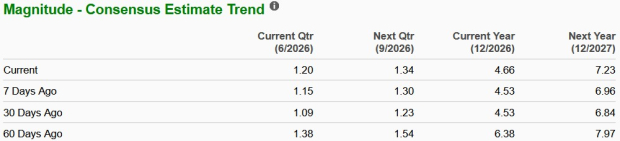

The Zacks Consensus Estimate for WIX’s 2026 sales and EPS implies year-over-year growth of 13.8% and a decrease of 36.3%, respectively. In the past 60 days, earnings estimates for 2026 have decreased from $6.38 to $4.66 per share.

WIX Earnings Estimate Trend

Image Source: Zacks Investment Research

Price Performance & Valuation of SHOP & WIX

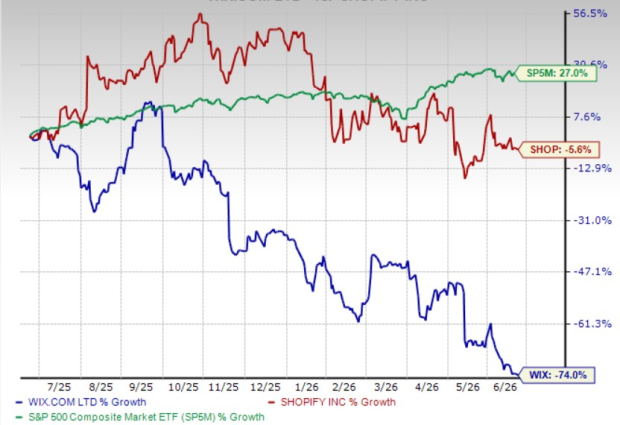

Shopify stock has declined 5.6% in the past year against the S&P 500’s growth of 27%. Meanwhile, WIX’s shares have declined 74% in the same time.

SHOP & WIX Stock Performance

Image Source: Zacks Investment Research

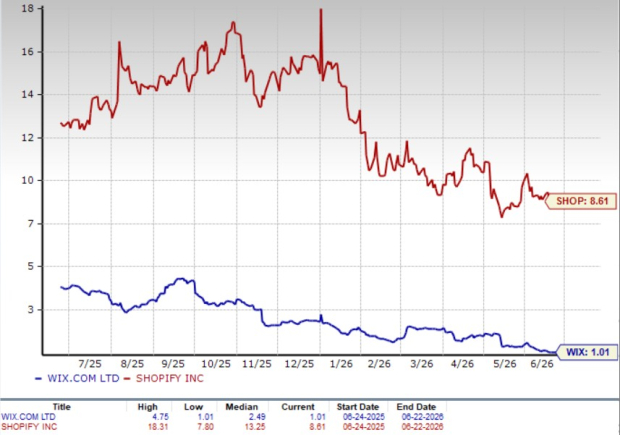

Shopify is trading at a forward 12-month price-to-sales (P/S) ratio of 8.61. Wix's forward 12-month P/S multiple sits at 1.01 over the same time frame.

P/S (F12M)

Image Source: Zacks Investment Research

End Notes

While both Shopify and Wix are benefiting from the growing adoption of AI and digital commerce tools, the former appears to be in a stronger position today. The company is delivering faster revenue growth, expanding its presence among large enterprises and building a broader commerce ecosystem that spans payments, financial services, marketing and AI-driven shopping experiences.

Shopify's growth is also supported by rising earnings expectations and strong momentum across merchant acquisition and engagement. In contrast, Wix remains primarily focused on website creation and is still working through challenges in its partner business while integrating newer growth initiatives such as Base44.

Although Wix offers a more attractive valuation and has executed well on AI innovation, Shopify's larger scale, stronger growth trajectory, expanding commerce capabilities and improving earnings outlook give it a clearer path to long-term value creation. As a result, Shopify appears better positioned to capitalize on the next phase of e-commerce and AI-driven commerce evolution.

Both stocks presently carry a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Research Chief Names "Single Best Pick to Double"

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

This company targets millennial and Gen Z audiences, generating nearly $1 billion in revenue last quarter alone. A recent pullback makes now an ideal time to jump aboard. Of course, all our elite picks aren’t winners but this one could far surpass earlier Zacks’ Stocks Set to Double like Nano-X Imaging which shot up +129.6% in little more than 9 months.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Wix.com Ltd. (WIX): Free Stock Analysis Report

Shopify Inc. (SHOP): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).