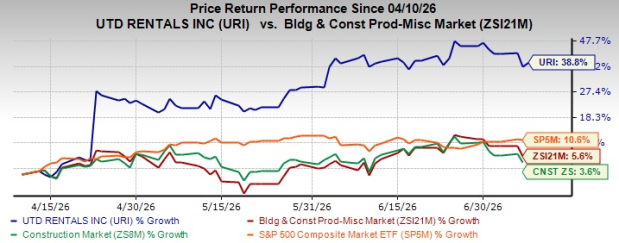

United Rentals, Inc. URI surged 38.8% in the past three months, outperforming the Zacks Building Products - Miscellaneous industry, the broader Zacks Construction sector and the S&P 500 Index.

This Connecticut-based equipment rental company is benefiting from favorable secular trends in non-residential construction, infrastructure modernization, power, manufacturing, mining and data center development, which continue to drive healthy equipment rental demand. Raised 2026 guidance, robust free cash flow generation and disciplined capital allocation are likely to have strengthened investor confidence, supporting the stock's recent outperformance and reinforcing expectations for sustained earnings and shareholder value growth.

Although near-term challenges like elevated restructuring costs, margin pressures and ongoing macroeconomic uncertainties are concerning, the positive industry dynamics and expanding specialty offerings of URI are more than likely to boost mid and long-term growth.

Image Source: Zacks Investment Research

Let’s decode the factors molding United Rentals’ prospects in the upcoming period.

Factors Driving United Rentals’ Growth Momentum

Strong Equipment Rental Demand: United Rentals is benefiting from sustained demand across both construction and industrial markets, reinforcing its long-term growth outlook. During the first quarter of 2026, equipment rental revenues climbed 8.7% year over year to a record $3.42 billion, driven by 2.3% growth in fleet productivity and a 5.7% expansion in average fleet size. Management highlighted robust activity in non-residential construction, infrastructure, power, manufacturing, mining and data centers, while healthcare and industrial manufacturing projects also gained traction.

URI expects to play a key role in the 2026 FIFA World Cup-related projects, adding another growth catalyst. Encouraged by strong customer feedback, particularly for large projects, United Rentals raised its 2026 guidance, expecting total revenues of $16.9-$17.4 billion (from $16.8-$17.3 billion) and higher EBITDA, reflecting confidence in continued demand for equipment rentals and market share gains.

Disciplined Acquisitions & Capital Allocation Efforts: United Rentals continues to strengthen its competitive position through strategic acquisitions while maintaining a disciplined capital allocation framework. Since its founding, the company has completed nearly 250 acquisitions to expand its geographic footprint, specialty offerings and one-stop-shop capabilities. Alongside inorganic growth, management continues investing in fleet expansion, increasing 2026 gross rental capital expenditure guidance to $4.4-$4.8 billion to meet rising customer demand.

Despite these investments, United Rentals generated more than $1 billion in first-quarter 2026 free cash flow and maintained a conservative net leverage ratio of 1.9x, providing ample financial flexibility. The company also returned $500 million to shareholders through dividends and share repurchases during the quarter and plans to repurchase approximately $1.5 billion of stock in 2026, underscoring its balanced approach toward growth investments and shareholder value creation.

Specialty Business Continues to Outperform: United Rentals' Specialty segment remains a major growth engine, supported by expanding product offerings and increasing demand for higher-value rental solutions. Specialty rental revenues surged 13.8% year over year in the first quarter of 2026 to a record $1.19 billion, significantly outpacing the General Rentals business. Growth was broad-based across all specialty lines, with the company opening 17 new greenfield ("cold start") locations during the quarter to expand market reach.

Specialty segment now represents 36.5% of total revenues (as of 2025) and has delivered a robust 20.2% revenue CAGR over the past decade, reflecting sustained customer adoption. Although margins faced temporary pressure from higher depreciation and delivery costs, management continues investing in this business, viewing Specialty as a key driver of long-term revenue growth, differentiation and cross-selling opportunities.

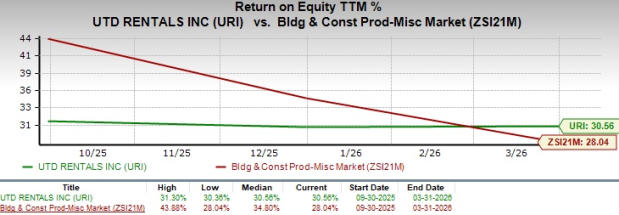

URI’s ROE Position

United Rentals' superior return on equity (ROE) indicates its growth potential. It provides solid investment returns relative to the industry average, as reflected in its current trailing 12-month ROE of 30.56%. This compares favorably with the industry's ROE of 28.04%. The factor mentioned above indicates the company’s efficiency in using its shareholders’ funds, along with its ability to generate profit with minimum capital usage.

Image Source: Zacks Investment Research

Can United Rentals Stay Ahead of Construction Rivals?

United Rentals enjoys a distinct competitive advantage over peers like Armstrong World Industries, Inc. AWI, Masco Corporation MAS and Argan, Inc. AGX because it directly benefits from rising equipment rental demand across virtually every major construction and industrial end market.

While Armstrong World and Masco primarily depend on commercial interior renovation and residential repair and remodeling activity, and Argan's growth is tied largely to power generation and industrial EPC projects, United Rentals serves all these markets simultaneously through its broad equipment rental platform. Strong demand from infrastructure, non-residential construction, manufacturing, data centers, utilities, mining and large industrial projects continues to support fleet utilization and rental pricing.

URI’s unmatched scale, approximately $23 billion rental fleet, extensive North American branch network and rapidly expanding Specialty business further strengthen its competitive position. Coupled with strategic acquisitions, robust free cash flow generation and disciplined capital allocation, these advantages enable United Rentals to outperform renowned peers, like Armstrong World, Masco and Argan, by capturing a broader range of growth opportunities while delivering more resilient earnings across market cycles.

Earnings Estimate Trend of URI

URI’s earnings estimates for 2026 and 2027 have moved downward over the past 30 days to $46.76 and $52.75 per share, respectively. However, the revised estimates for 2026 and 2027 imply year-over-year improvements of 11.2% and 12.8%, respectively.

Image Source: Zacks Investment Research

What is Restricting United Rentals’ Near-Term Prospects?

United Rentals faces several near-term challenges despite its strong operating momentum. It continues to incur restructuring costs tied to branch consolidations and workforce optimization, while the Specialty segment experienced margin pressure from higher depreciation, delivery expenses and a shift toward lower-margin ancillary revenues.

More broadly, management remains exposed to macroeconomic uncertainties, including inflation, elevated interest rates, tariffs, supply-chain disruptions and potential slowdowns in construction or industrial activity. Any weakening in large project spending or customer demand could reduce fleet utilization, pressure rental pricing and moderate revenue growth, potentially weighing on profitability and cash generation.

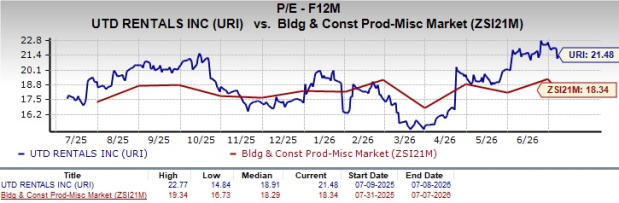

URI Stock Trading at a Premium

URI stock is currently trading at a premium compared with the industry peers, with a forward 12-month price-to-earnings (P/E) ratio of 21.48, as the trend lines suggest below.

Image Source: Zacks Investment Research

Can URI Stock Maintain Its Momentum in the Near Future?

United Rentals remains well-positioned to sustain its long-term growth trajectory, supported by strong demand across non-residential construction, infrastructure, power, manufacturing, mining and data center projects. Its robust fleet utilization and raised 2026 guidance underscore management’s confidence in continued market share gains and earnings growth. The company’s disciplined acquisition strategy, industry-leading rental fleet, strong free cash flow generation and balanced capital allocation further reinforce its competitive advantage.

Although the stock trades at a premium and near-term headwinds, including restructuring costs, margin pressure and macroeconomic uncertainty, could create periodic volatility, these challenges appear manageable given the favorable end-market fundamentals. While recent downward earnings estimate revisions warrant monitoring, forecasts still indicate healthy double-digit earnings growth over the next two years.

Supported by superior return on equity and a current Zacks Rank #2 (Buy), URI stock appears capable of maintaining its market outperformance. Long-term investors can consider buying the stock at current levels rather than waiting for a better opportunity, given its durable growth drivers and resilient business model. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Radical New Technology Could Hand Investors Huge Gains

Quantum Computing is the next technological revolution, and it could be even more advanced than AI.

While some believed the technology was years away, it is already present and moving fast. Large hyperscalers, such as Microsoft, Google, Amazon, Oracle, and even Meta and Tesla, are scrambling to integrate quantum computing into their infrastructure.

Senior Stock Strategist Kevin Cook reveals 7 carefully selected stocks poised to dominate the quantum computing landscape in his report, Beyond AI: The Quantum Leap in Computing Power .

Kevin was among the early experts who recognized NVIDIA's enormous potential back in 2016. Now, he has keyed in on what could be "the next big thing" in quantum computing supremacy. Today, you have a rare chance to position your portfolio at the forefront of this opportunity.

See Top Quantum Stocks Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

United Rentals, Inc. (URI): Free Stock Analysis Report

Masco Corporation (MAS): Free Stock Analysis Report

Armstrong World Industries, Inc. (AWI): Free Stock Analysis Report

Argan, Inc. (AGX): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).