The medical supply industry has entered the second half of 2026 from a position of strength, supported by resilient healthcare utilization, rising specialty care demand, increasing adoption of digital technologies and continued migration of patient care toward lower-cost outpatient settings.

Across major industry participants, management highlighted healthy procedure volumes, growing investment by healthcare providers, expanding specialty pharmaceutical utilization and stronger demand for technology-enabled workflow solutions. At the same time, companies continue to modernize supply chains through automation and AI while investing in value-added services that improve efficiency for providers and patients. However, the industry is not without challenges. Tariff-related cost pressures, pricing changes tied to healthcare policy, uneven demand in certain product categories and macroeconomic uncertainty continue to create operational complexity.

Companies with diversified business models, technology leadership, specialty exposure and disciplined capital allocation appear well positioned to capitalize on these favorable industry tailwinds through the remainder of 2026. Per a Markets and Markets report, the global medical supplies industry is expected to reach $163.5 billion by 2027, at a CAGR of 3.4% in the 2022-2027 period. Industry participants, such as McKesson MCK, Cardinal Health CAH, West Pharmaceutical Services WST, Align Technology ALGN and Henry Schein HSIC, are likely to ride on the favorable macro trends amid lingering tariff risks.

Industry Description

The global dental industry consists of companies that design, develop, make and market dental products, such as consumables, laboratory products and specialty items. Some of these companies also offer software and systems for practice management, patient education and office administration. Dental stocks have been drawing attention amid a recovery in sales following the weakness caused by pandemic-induced disruptions. The market has been recovering and maintaining its position.

Dental care is provided based on the advice and recommendations of the American Dental Association and the Centers for Disease Control and Prevention. Thanks to the rebound seen among companies in this space, patient volumes have been increasing steadily following the removal of COVID-19 restrictions.

Major Trends Shaping the Future of the Medical Dental Supplies Industry

Specialty Care and Outpatient Healthcare Support Industry Growth: Healthcare delivery continues shifting toward specialty therapies, community-based care and non-acute treatment settings, creating sustained demand for medical distribution and support services. Specialty pharmaceuticals, oncology services, home-based care, ambulatory surgical centers and precision medicine remain among the industry's fastest-growing segments.

Companies are expanding provider networks, investing in specialty capabilities and strengthening patient access platforms to benefit from higher-acuity care migrating outside traditional hospitals. This structural transition supports long-term volume growth while increasing demand for integrated distribution, logistics and patient support solutions.

AI, Automation and Digital Innovations: Medical supply companies are increasingly leveraging AI, automation and cloud-based platforms to improve provider productivity, optimize supply chains and enhance patient engagement. Investments range from AI-enabled inventory planning and automated distribution centers to digital treatment planning, practice management software and workflow automation.

These technologies are helping providers improve efficiency, reduce administrative burdens and expand patient access while allowing distributors to enhance operational resilience and margins. As healthcare systems prioritize productivity improvements, technology-enabled service offerings are becoming an increasingly important source of competitive advantage and long-term growth.

Increasing Burden of Oral Diseases and an Aging Population: The U.S. dental equipment market is structurally supported by demographic aging and rising disease prevalence. Older cohorts account for a disproportionate share of restorative and surgical procedures, reflecting a higher incidence of caries, periodontal disease, and tooth loss. With the 65+ population expanding, demand visibility remains strong, reinforcing procedure volumes and equipment utilization across practices.

Growing Awareness and Emphasis on Preventive Care: Rising awareness of oral hygiene and preventive care is shifting demand toward early-stage interventions. Increased utilization of fluoride treatments, sealants, and prophylaxis products reflects a broader transition toward prevention-focused dentistry, supporting recurring revenue streams within consumables.

Minimally Invasive and Cosmetic Dentistry Trends: Patient preference is increasingly skewed toward minimally invasive and aesthetic procedures, including whitening and veneers. This trend is expanding demand for specialized materials and precision equipment, while also increasing procedure frequency and average spend per patient.

Expansion of Dental Clinics and Group Practices: The ongoing expansion of dental clinics, DSOs, and hospital-based practices is structurally increasing equipment demand. Higher patient throughput, standardized treatment protocols, and procurement efficiencies are driving consistent product utilization across growing care networks.

Regional Market Growth Drivers: Emerging markets, particularly in Asia-Pacific, are exhibiting above-average growth due to rising healthcare expenditure, improving access, and supportive policy frameworks. Dental tourism and expanding middle-class demand are further accelerating equipment adoption in these regions

Policy Changes and Ongoing Cost Inflation: Despite healthy demand, companies continue navigating an increasingly complex operating environment. Tariffs, healthcare policy changes, pharmaceutical pricing reforms under the Inflation Reduction Act, higher freight costs and inflationary pressures remain important headwinds.

Several companies also cited softer demand in select product categories, such as respiratory diagnostics following a mild flu season, while competitive pricing in certain technology markets continued to weigh on margins. Although management remains confident in mitigating these pressures through pricing actions, productivity initiatives and supply-chain improvements, these headwinds are likely to remain through the second half of 2026.

Zacks Industry Rank

The Zacks Medical Dental Supplies industry falls within the broader Zacks Medical sector.

It carries a Zacks Industry Rank #68, which places it in the top 28% of 243 Zacks industries.

The group’s Zacks Industry Rank, which is basically the average of the Zacks Rank of all member stocks, indicates dull near-term prospects. Our research shows that the top 50% of the Zacks-ranked industries outperform the bottom 50% by a factor of more than 2 to 1.

Before we present a few dental supply stocks that you may want to consider for your portfolio, let’s take a look at the industry’s recent stock-market performance and valuation picture.

Industry Performance

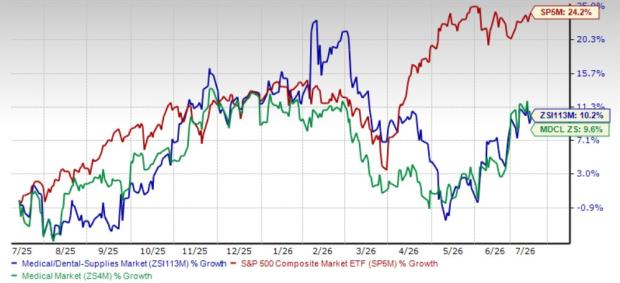

The industry has outperformed its sector but underperformed the S&P 500 composite in the past year.

Stocks in this industry collectively gained 10.2% compared with the Zacks Medical sector’s rise of 9.6%. The S&P 500 has surged 24.2% in the same time frame.

One-Year Price Performance

Industry's Current Valuation

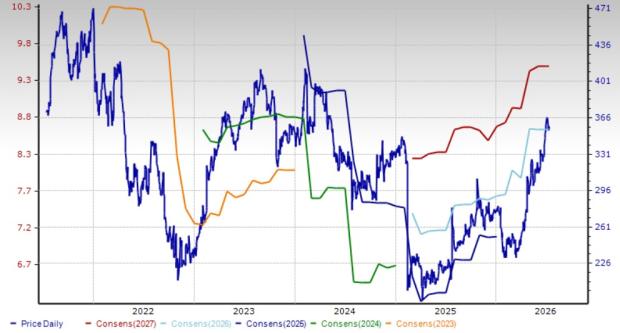

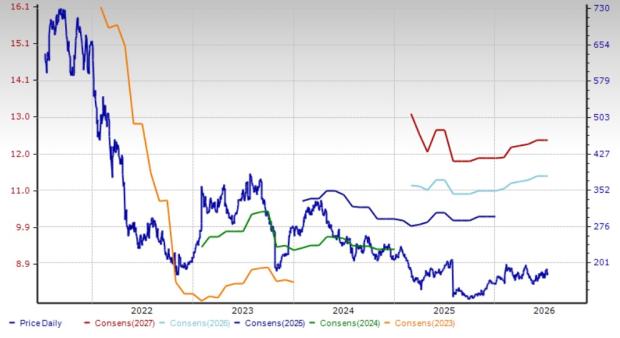

On the basis of the forward 12-month price-to-earnings (P/E), which is commonly used for valuing medical stocks, the industry is currently trading at 16.83X compared with the S&P 500’s 21.23X and the sector’s 21.07X.

Over the past five years, the industry has traded as high as 21.75X and as low as 15.53X, with the median being 18.44X, as the charts show.

Price-to-Earnings Forward Twelve Months (F12M)

Price-to-Earnings Forward Twelve Months (F12M)

5 Key Dental Supply Picks

McKessonremains one of the strongest beneficiaries of the industry's accelerating shift toward specialty care and technology-enabled healthcare services. The company continues to expand its oncology and multispecialty ecosystem through the integration of Core Ventures and PRISM Vision, broadening its presence across community oncology, retina and ophthalmology.

Management also highlighted continued momentum in biopharma services, where rising demand for access and affordability programs, particularly for complex specialty therapies, is strengthening its value proposition. AI-enabled workflow tools, automation and advanced distribution capabilities are further improving physician productivity, patient access and supply-chain efficiency. Investments in AI-powered inventory planning, highly automated distribution centers and technology infrastructure are expected to support operating leverage while enhancing service reliability.

McKesson's disciplined capital allocation, robust free cash flow generation and continued investment in automation reinforce confidence in sustained earnings growth. However, the company continues to operate in a dynamic policy environment, with pharmaceutical pricing reforms, evolving utilization patterns and continued investments in technology infrastructure likely to influence near-term profitability.

The Zacks Consensus Estimate for fiscal 2027 revenues indicates an improvement of 7.3% from the year-ago reported figure, while the same for earnings implies a rise of 13.2%. MCK carries a Zacks Rank #2 (Buy) at present. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Price and Consensus: MCK

Cardinal Healthhas entered the second half of 2026 with strong momentum, driven by broad-based pharmaceutical demand and rapid expansion across its higher-growth businesses. Specialty pharmaceuticals remain the primary growth engine, with specialty revenues expected to exceed $50 billion during fiscal 2026, supported by robust demand for oncology therapies, GLP-1 products and branded medicines.

Beyond pharmaceutical distribution, the company continues to benefit from accelerating growth in At-Home Solutions, Nuclear and Precision Health Solutions and OptiFreight Logistics, reflecting increasing demand for decentralized care, theranostics and healthcare supply-chain optimization. Strategic acquisitions, including Advanced Diabetes Supply, are expanding Cardinal Health's chronic care capabilities while strengthening its long-term growth platform.

Operational discipline and resilient execution have also enabled the company to navigate complex market conditions effectively. Nevertheless, tariff-related costs remain a significant headwind for the Global Medical Products and Distribution segment, while the Navista goodwill impairment underscores execution risks within certain growth initiatives. Future performance will also depend on continued success in managing supply-chain costs and evolving healthcare policy changes.

The Zacks Consensus Estimate for fiscal 2026 revenues indicates an improvement of 15.1% from the year-ago reported figure, while the same for earnings implies a rise of 30.7%. CAH carries a Zacks Rank #2 at present.

Price and Consensus: CAH

West PharmaceuticalServices remainswell positioned to benefit from long-term growth in biologics and high-value injectable therapies, supported by sustained demand for advanced drug containment and delivery solutions. Management emphasized continued strength across its High-Value Products portfolio, with increasing customer adoption of premium components and proprietary delivery technologies driving favorable product mix and margin expansion.

The company's strategy is also supported by healthy demand for biologics, expanding capacity investments and growing participation in next-generation injectable medicines. This positions West Pharma to capitalize on structural trends in pharmaceutical innovation. Operational improvements and disciplined manufacturing execution continue to strengthen profitability while reinforcing customer relationships with leading biopharma companies.

However, management acknowledged that macroeconomic uncertainty, customer inventory normalization in selected product categories and the pace of new drug commercialization could create periodic revenue variability. Despite these risks, West Pharma's innovation-led portfolio, diversified customer base and focus on high-value solutions provide a solid foundation for continued growth through the remainder of 2026.

The Zacks Consensus Estimate for 2026 revenues indicates an improvement of 8.4% from the year-ago reported figure, while the same for earnings implies a rise of 18%. WST carries a Zacks Rank of 2 at present.

Price and Consensus: WST

Align Technologyis well positioned to benefit from the continued digitization of orthodontics and the growing adoption of clear aligner therapy. The company delivered record Invisalign case shipments in the first quarter, supported by broad-based growth across adults, teens and younger patients, while international markets continued to outpace North America. Management also highlighted strong momentum in dental service organizations (DSOs), which are increasingly adopting Align Technology's integrated digital platform to improve clinical workflows and patient conversion.

The expanding installed base of iTero scanners, rising adoption of exocad software and the rollout of restorative treatment solutions further strengthen Align Technology's digital ecosystem and create opportunities beyond orthodontics. Financing programs, doctor subscription models and treatment planning services are also improving affordability, clinician confidence and utilization, supporting long-term case growth. However, softer patient traffic in parts of the U.S. retail channel, pricing pressure from lower-cost scanner offerings and uneven macroeconomic conditions across certain markets remain key challenges to monitor through the remainder of 2026.

The Zacks Consensus Estimate for 2026 revenues indicates an improvement of 3.7% from the year-ago reported figure, while the same for earnings implies a rise of 8.1%. ALGN carries a Zacks Rank #2 at present.

Price and Consensus: ALGN

Henry Scheinhas entered the second half of 2026 with improving operating momentum, supported by market share gains, expanding digital capabilities and a sharpened focus on operational excellence. Management sees healthy demand across dental markets, with continued investments by dental service organizations (DSOs) and practitioners supporting equipment, merchandise and specialty product sales.

The company's integrated portfolio — including distribution, specialty products, practice management software and value-added services — positions it to benefit from customers' increasing focus on productivity and workflow optimization. AI-enabled practice management solutions, cloud-based software adoption and ongoing value creation initiatives are expected to drive margin expansion while strengthening customer engagement. Growth in value implants, home solutions and non-acute care channels provides additional tailwinds, while restructuring initiatives and supply-chain efficiencies should further enhance profitability.

Nevertheless, Henry Schein continues to face pricing pressure in digital equipment from new market entrants, softer demand for respiratory diagnostic products following a mild flu season, and cost inflation from higher freight and merchandise prices. Effective execution of its transformation initiatives will remain critical to sustaining earnings growth through the rest of 2026.

The Zacks Consensus Estimate for 2026 revenues indicates an improvement of 4.1% from the year-ago reported figure, while the same for earnings implies a rise of 7%. HSIC carries a Zacks Rank of 2 at present.

Price and Consensus: HSIC

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company's customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren't winners but this one could far surpass earlier Zacks' Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

McKesson Corporation (MCK): Free Stock Analysis Report

Align Technology, Inc. (ALGN): Free Stock Analysis Report

Cardinal Health, Inc. (CAH): Free Stock Analysis Report

Henry Schein, Inc. (HSIC): Free Stock Analysis Report

West Pharmaceutical Services, Inc. (WST): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).