Iron Mountain IRM is a well-established REIT that serves more than 240,000 customers worldwide. Its records storage business generates dependable recurring revenues, while its growing data center, digital solutions and asset lifecycle services are creating new growth opportunities. Recent acquisitions and investments have strengthened its market position and broadened its service offerings.

The company still faces a few challenges. Demand for paper records is gradually declining, while competition can limit pricing power. In addition, its relatively high debt and interest costs, along with currency fluctuations, could weigh on earnings.

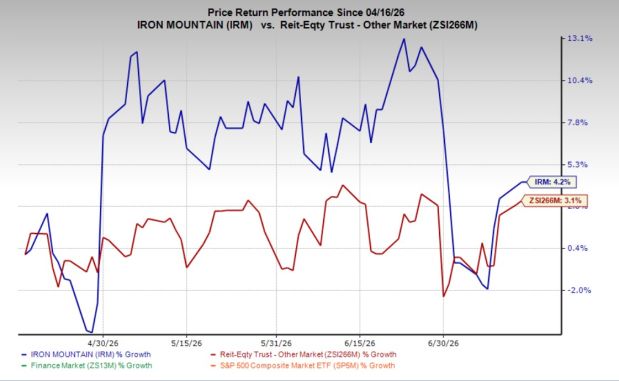

In the past three months, shares of this Zacks Rank #3 (Hold) company have gained 4.2% compared with the industry's growth of 3.1%.

Image Source: Zacks Investment Research

What Aids IRM?

Iron Mountain continues to benefit from the stability of its records storage business, which generates predictable recurring cash flow. In the first quarter of 2026, consolidated storage rental revenues increased 15.5% year over year, while Global Records and Information Management storage rental revenues rose 8.7%. Organic storage rental revenues grew 12.4%. This steady income provides funding for the company's expansion into higher-growth businesses.

The data center business remains Iron Mountain's strongest growth driver. First-quarter 2026 data center revenues climbed 47.1% year over year to $254.7 million, while the adjusted EBITDA margin remained healthy 52.1%. The operating portfolio expanded to 507.2 MW and was 97.2% leased, reflecting solid customer demand.

Growth is also coming from digital solutions and asset lifecycle management. These businesses, including data centers, expanded by more than 50% year over year during the first quarter of 2026, while consolidated service revenues increased 30.6% to $841 million. Recent acquisitions have broadened Iron Mountain's services, further expanding its scale.

The company's financial performance remains strong. First-quarter 2026 revenues rose 21.6% to $1.94 billion, adjusted EBITDA increased 22.1% to $708 million, and AFFO climbed 22.3% to $426 million or $1.43 per share. Management also raised its full-year 2026 outlook, reflecting confidence in continued earnings growth, while steady dividend increases further support the long-term investment case.

What’s Hurting IRM?

Iron Mountain's traditional records storage business faces a long-term challenge as customers continue shifting from paper documents to digital storage. This trend could gradually reduce demand for physical storage and related services, making future growth increasingly dependent on pricing and newer business lines. Intense competition across the records management industry also limits pricing power and can pressure margins.

The company's international operations add another layer of uncertainty. Foreign currency movements can reduce reported revenues and EBITDA, while relatively higher labor costs in some overseas markets can weigh on profitability during slower demand periods.

Iron Mountain also operates with a sizeable debt load. As of March 31, 2026, net debt stood at about $17.0 billion, while first-quarter 2026 net interest expense increased 14.9% year over year to $223.8 million. Rising borrowing expenses can reduce cash flow and limit financial flexibility for future investments.

Stock to Consider

Some better-ranked stocks from the broader REIT industry are Host Hotels & Resorts HST and Vornado Realty Trust VNO, carrying a Zacks Rank #2 (Buy) each at present. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

The Zacks Consensus Estimate for HST’s 2026 FFO per share has moved up marginally to $2.13 over the past month.

The consensus estimate for VNO’s 2026 FFO per share has moved up marginally to $2.34 over the past two months.

Note: Anything related to earnings presented in this write-up represents funds from operations (FFO), a widely used metric to gauge the performance of REITs.

Radical New Technology Could Hand Investors Huge Gains

Quantum Computing is the next technological revolution, and it could be even more advanced than AI.

While some believed the technology was years away, it is already present and moving fast. Large hyperscalers, such as Microsoft, Google, Amazon, Oracle, and even Meta and Tesla, are scrambling to integrate quantum computing into their infrastructure.

Senior Stock Strategist Kevin Cook reveals 7 carefully selected stocks poised to dominate the quantum computing landscape in his report, Beyond AI: The Quantum Leap in Computing Power .

Kevin was among the early experts who recognized NVIDIA's enormous potential back in 2016. Now, he has keyed in on what could be "the next big thing" in quantum computing supremacy. Today, you have a rare chance to position your portfolio at the forefront of this opportunity.

See Top Quantum Stocks Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Iron Mountain Incorporated (IRM): Free Stock Analysis Report

Host Hotels & Resorts, Inc. (HST): Free Stock Analysis Report

Vornado Realty Trust (VNO): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).