WM’s WM top line benefits from continued demand for its expertise, robust infrastructure and asset network in managing waste. Strategic buyouts, optimized pricing and strict cost management drive profitability and operational efficiency. WM’s steady returns and minimal price fluctuations, combined with the company’s shareholder-friendly policies, enhance its investment appeal.

However, weak liquidity and elevated leverage erode profitability, limit expansion and weaken overall financial performance. The stock’s slow price appreciation makes it unappealing to momentum traders chasing quick, short-term profits.

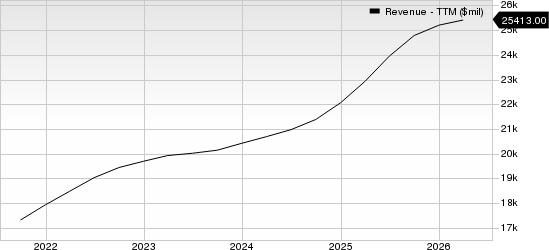

How Is WM Faring?

WM provides collection, transfer, recycling, resource recovery and disposal services to residential, commercial, industrial and municipal customers. The company strengthens its position in the waste management industry through its robust waste collection, recycling and disposal infrastructure, enabling it to generate steady revenues and maintain lasting partnerships with its clients. This competitive advantage over its rivals has contributed to sustained growth, with the company’s revenues increasing at a compound annual growth rate of 7.1% from 2021 to 2025.

Waste Management, Inc. Revenue (TTM)

Waste Management, Inc. revenue-ttm | Waste Management, Inc. Quote

The company’s optimized pricing and efficient cost management strategies are key drivers of its continued margin growth. By optimizing routes, enhancing service delivery and boosting operational efficiency, WM eliminates unnecessary costs, facilitating margin expansion. The company ensures that pricing aligns with the quality, reliability and demand for its services, while integrating modern technology and process improvements to reduce costs and boost service reliability and customer satisfaction.

Strategic acquisitions, such as Stericycle, which specializes in collecting and disposing of regulated medical waste, add complementary platforms in the medical waste sector, boosting margins and expanding the company’s market presence. The company recorded a $653 million increase in net cash driven by recent buyouts in 2025.

WM’s steady returns and low-volatility business nature appeal to long-term investors and those seeking stability during market fluctuations. The company’s sustainability initiatives and innovations, such as converting landfill gas into renewable energy, position it as a leader in the green economy, attracting environmental, social and governance-focused investors.

WM has demonstrated a strong commitment to its shareholders through consistent dividend payments. It paid dividends of $1.1 billion, $1.2 billion and $1.3 billion in 2023, 2024 and 2025, respectively. Such moves instill investor confidence and enhance shareholder value.

Meanwhile, a stable industry with consistent demand results in steady but modest stock price movements. This enables WM to generate stable revenues and achieve gradual expansion, but it limits the potential for rapid, exponential growth. This makes the stock unattractive to momentum investors.

WM’s recent buyouts and ongoing investments in renewable energy have burdened it with a significant debt load. Allocating a large portion of its cash flow to service these debts, including interest payments and principal repayment, impairs profitability and execution.

WM reported mixed first-quarter 2026 results. The company reported adjusted earnings of $1.81 per share, which topped the Zacks Consensus Estimate by 3.4% and increased 8.4% from the year-ago quarter. Revenues of $6.23 billion marginally missed the consensus estimate but rose 3.5% year over year.

WM currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here

Stocks to Consider

A couple of better-ranked stocks in the Waste Removal Services industry are Veralto Corporation VLTO and GFL Environmental Inc. GFL.

Veralto Corporation carries a Zacks Rank #2 (Buy) at present. It has a long-term earnings growth expectation of 8.4%. VLTO delivered a trailing four-quarter earnings surprise of 4.9%, on average.

GFL Environmental Inc. also holds a Zacks Rank of 2 at present. It has a long-term earnings growth expectation of 23.6%. GFL's earnings beat estimates in two of the last four reported quarters, matched once and missed once, with the surprise being 23.8%, on average.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company's customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren't winners but this one could far surpass earlier Zacks' Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Waste Management, Inc. (WM): Free Stock Analysis Report

GFL Environmental Inc. (GFL): Free Stock Analysis Report

Veralto Corporation (VLTO): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).