Many of the biggest tech companies are no longer content to rely on outside chipmakers to power their AI ambitions. Instead, firms like Alphabet (GOOG) (GOOGL), Meta Platforms (META), Tesla (TSLA), and now Alibaba (BABA) are designing more of their own silicon in-house, a shift that can give them greater control over performance, cost, and supply at a time when demand for AI computing is exploding.

Alibaba is the latest example here. The Chinese tech giant and China Telecom are launching a data center in southern China that will use 10,000 of Alibaba’s Zhenwu chips, a clear sign that the company wants to build out its own AI infrastructure rather than depend entirely on foreign suppliers.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

With China racing to strengthen its domestic AI ecosystem amid U.S. chip restrictions, Alibaba’s move could give BABA stock a stronger long-term story for investors looking for an AI name with both scale and strategic relevance.

A Tech Powerhouse Expanding Beyond E-Commerce

Alibaba Group Holding remains one of China’s most important internet and cloud franchises. The company sits at the intersection of e-commerce, cloud computing, and semiconductors, with businesses that span Taobao, Tmall, and one of the country’s largest cloud platforms. It is also pushing deeper into AI, both through software and hardware, as it works to build more of its own technology stack in-house.

That strategy is becoming more visible as Alibaba is expanding its AI footprint with Qwen 3.6-Plus, an “agentic” large language model (LLM) designed to carry out multi-step tasks on its own. It has also integrated Ele.me into Taobao Instant Commerce, while Alibaba Cloud rolled out a next-generation Linux system aimed at training trillion-parameter models.

At the hardware level, T-Head continues to develop new processors, showing the company’s effort to vertically integrate more of its core infrastructure. Management has also pointed to a $100 billion AI and cloud revenue target over the next five years, signaling how central these businesses have become to the longer-term story.

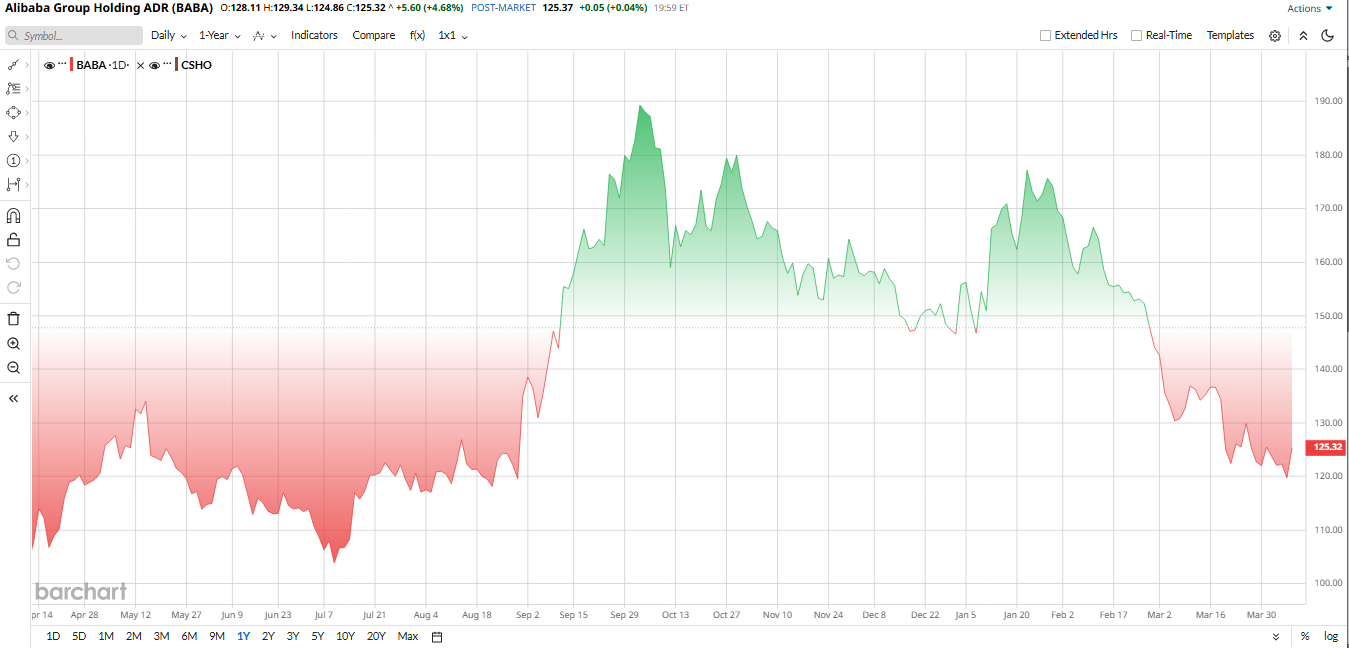

The stock, however, has been anything but steady. BABA rallied late last year on optimism around chip policy and cloud momentum, then gave back much of those gains in early 2026. Shares are still down roughly 15% year-to-date (YTD). Technicals show a mixed picture, with the stock above its 50-day moving average but well below its 200-day.

Valuation looks reasonable rather than cheap. Alibaba’s trailing price-to-earnings ratio is around 25.7 times, which is below its 10-year median and roughly in line with broader growth-tech peers. Its price-to-sales ratio of about 1.9 times also sits slightly below the industry average. That leaves BABA looking fairly valued, with upside likely tied more to execution in AI and cloud than to a deep valuation discount.

www.barchart.com

www.barchart.com What Happened With the AI Chip Cluster?

On April 8, Alibaba and China Telecom said they flipped the switch on a new AI data center in Shaoguan, Guangdong. The facility packs 10,000 of Alibaba’s in-house Zhenwu AI chips into a single, networked cluster. According to reports, this “fully domestic” system can train huge models with hundreds of billions of parameters and is designed to expand to 100,000 chips. Alibaba Cloud touted the project as a shift from “high-end performance breakthroughs to large-scale industrial implementation” of AI.

Investors took this news as a catalyst, and BABA stock jumped several percent on the day of the announcement, but most analysts say the impact is largely long-term. This cluster showcases Alibaba’s technical leadership and reduces reliance on foreign hardware, but it won’t show up as near-term revenue. Think of it as bolstering Alibaba’s cloud/AI moat. In the short run, it’s a positive for Alibaba’s strategic positioning, but not an instant earnings catalyst.

Alibaba Misses Q3 Earnings Estimate

Alibaba’s most recent quarter showed a clear split between growth and profitability. The company missed analysts' estimates on both top and bottom lines but still managed to generate revenue of $40.7 billion, rising just 2% year-over-year (YoY), though growth was closer to 9% excluding divestitures.

The standout was the Cloud Intelligence Group. Cloud revenue surged 36% YoY to about $6.2 billion, from strong demand tied to AI workloads. Meanwhile, newer initiatives are gaining traction. The Taobao Instant Commerce unit, which focuses on food and grocery delivery, grew roughly 56% as Alibaba continues to push deeper into quick commerce.

That said, this growth is coming at a cost. Heavy spending on AI infrastructure, logistics, and user incentives weighed significantly on profitability. Net income dropped 66% YoY to $2.3 billion, while adjusted earnings per share came in at about $1.01, down 67%.

Cash generation also weakened. Free cash flow declined 71% to roughly $1.6 billion as the company ramped up investments across its ecosystem. Still, Alibaba ended the quarter with a solid $80.1 billion in cash and equivalents, giving it ample flexibility to continue funding its long-term AI and commerce strategy.

CEO Eddie Wu put a bright spin on the results, saying, “AI is and will continue to be one of our primary growth engines,” and noted that Alibaba’s consumer-facing Qwen app already has 300 million monthly users completing real tasks.

CFO Toby Xu similarly emphasized that the AI/cloud boom “gives us confidence to scale investments.” Alibaba did not give formal guidance for the next quarter or year, but analysts note that the bulk of its tech investments, from chips to logistics, will keep profit growth subdued in 2026, with a rebound expected only in 2027.

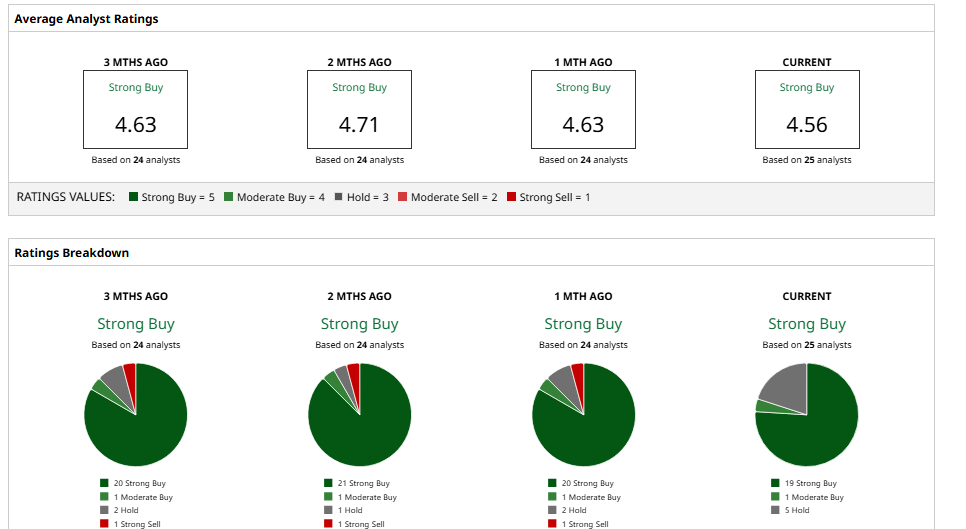

What Analysts Say About BABA Stock?

Wall Street’s take on Alibaba is mostly bullish on the long-term opportunity, even if there’s debate in the near term. Morgan Stanley recently reiterated “Overweight” on BABA stock with a $180 12-month target, noting that the in-house chip launch “reinforces Alibaba’s position across the AI technology stack.”

Bank of America likewise kept its “Buy” rating, with a price target of $180, emphasizing Alibaba’s heavy AI investments. Tiger Brokers even upgraded Alibaba to “Buy” with a $175 target, citing “accelerating momentum in AI and cloud technology.”

On the flip side, some firms have trimmed targets after the latest miss, e.g., Jefferies cut its target to $212 from $225 and Mizuho to $190, noting weak consumer spending.

Overall, Barchart’s consensus among analysts is a Strong Buy, with an average 12-month target near $183, implying roughly 50% upside from current levels. In other words, many see Alibaba’s deep pockets and AI push as undervalued today, though most expect patience is needed as big investments play out.

www.barchart.com

www.barchart.com On the date of publication, Nauman Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Alibaba Just Unveiled a Massive AI Chip Cluster. Does That Make BABA Stock a Buy Here? Foldable iPhones Are Reportedly Still on Track for September. Should You Buy AAPL Stock Here? As Meta Platforms Unveils Muse Spark, Should You Buy META Stock Now? Wedbush: What You Need to Know About the Latest ‘Victory’ for Apple Stock