Oil has been on a knife-edge in 2026, with strikes on Iran’s Kharg Island briefly pushing Brent crude (QAM26) above $110 and a very tenuous ceasefire stirring fresh worries about traffic through the Strait of Hormuz. That same flashpoint has fueled talk that a serious squeeze in shipments could even send prices toward $200 a barrel, turning every headline into a new risk check for global energy names.

Shell (SHEL) is right in the middle of that story. The company says strong oil trading should give its Q1 numbers a boost, even as it lowers its gas output outlook because of the Iran situation. That mix of higher crude prices, softer production guidance, and capital moving out of the region is an odd backdrop for a stock that is already up more than 20% this year and still yields about 3.1%.

More Yield, Less Trap: Sign up free to get Barchart’s daily Dividend Investor newsletter straight to your inbox.

The real question now is whether this ceasefire and cooling Middle East risk make SHEL more appealing or more vulnerable at these levels. Let’s dive in.

SHEL’s Solid Financial Footing

Shell is a UK‑based energy giant that produces and sells oil, natural gas, and liquefied natural gas (LNG) across global markets.

Its New York–listed stock trades at $91.18 as of the afternoon of April 9, up 24% so far in 2026 and 42% over the past year.

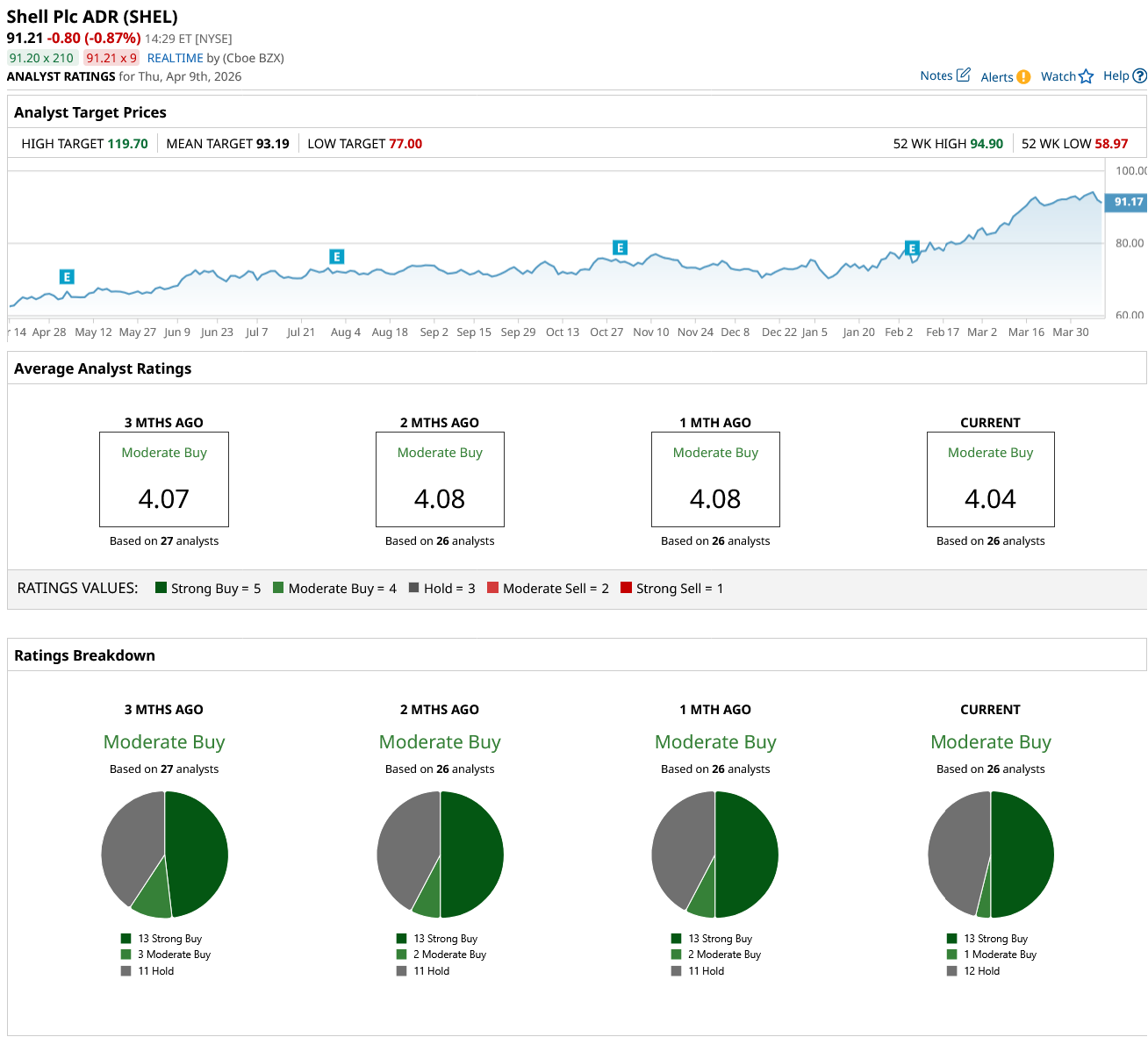

www.barchart.com

www.barchart.com SHEL stock still looks reasonably priced, trading at 14.96x trailing earnings and 6.04x price‑to‑cash‑flow, versus sector medians of 16.79x and 7.39x. It has a market value of about $266.6 billion and offers a forward annual dividend of $2.98 per share, which works out to a 3.2% yield.

Their fourth-quarter 2025 results, released in late January, showed adjusted earnings of $3.256 billion, down from $3.661 billion a year earlier and about 40% below the prior quarter. That worked out to $1.14 per share, short of the $1.21 Wall Street was looking for and the weakest quarterly profit since early 2021.

Shell’s cash flow told a stronger story. Its operating cash flow for 2025 came in at $42.86 billion, up 28.24% year-over-year (YoY). However, its net cash flow dropped to -$8.89 billion after a 46.84% decline driven by heavy investment and money returned to shareholders.

Even so, the board still kept its foot on the pedal for buybacks, approving another $3.5 billion repurchase program for the first quarter of 2026.

SHEL’s Strategic Phase

Shell is quietly putting together a long‑term growth plan rather than just riding short‑term oil moves. It recently signed a deal with Greek group Metlen (MTLPF) to supply and trade between 0.5 and 1.0 billion cubic meters of LNG a year from 2027 to 2031. Those volumes will move through the Revithoussa and Alexandroupolis terminals in Greece and into the Vertical Gas Corridor. The goal is to strengthen gas supply into southern and central Europe as the region continues to shift away from Russian volumes.

There is also a big push underway offshore Nigeria. The company plans to invest an extra $20 billion in the proposed Bonga South West deepwater project, on top of about $7 billion already spent in the country since 2023. That follows a final investment decision on Bonga North.

The field holds more than 300 million barrels of recoverable resources and targets peak output of roughly 110,000 barrels per day before the end of the decade. These projects come with support from Nigeria’s government and offer a long pipeline of higher‑margin barrels. They can help cushion any hit from lower gas output linked to Middle East issues.

Venezuela adds another possible growth leg. The U.S.‑driven thaw there has reopened the door to new oil investment. At a White House meeting with President Donald Trump, CEO Wael Sawan said the company is “ready to go” and already sees “a few billion dollars’ worth of opportunities” once licenses are approved.

What Wall Street Expects From SHEL Next

Analysts are not brushing off Shell’s rally as a quick trade on Iran headlines. The first‑quarter report is due on May 1, and the Street is looking for earnings of $1.86 per share, just ahead of the $1.84 booked in the same period last year. That points to a small but positive YoY growth rate of about 1.09%.

This steady outlook supports a consensus “Moderate Buy” view on SHEL stock from 26 analysts, signaling cautious support rather than hype. The average target price sits at $93.19, implying only about 2% upside from here. That tiny gap suggests many on the Street think Shell has largely “earned” its 2026 gains already.

www.barchat.com

www.barchat.com Conclusion

SHEL looks like a sensible hold for investors who already own it and a buy‑on‑weakness idea for anyone looking to add energy exposure. The mix of a roughly 3.2% yield, ongoing buybacks, and steady earnings expectations points to a slight tilt toward more upside than downside over the next year. Shell’s next move will likely depend on how its Q1 report stacks up and whether strong oil trading can keep offsetting lower gas output as the Iran ceasefire settles in.

On the date of publication, Ebube Jones did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Up 24% in 2026 and Yielding 3.1%, How Should You Play SHEL Stock Amid an Iran Ceasefire? The Selloffs in ServiceNow and Salesforce Stocks Are Disconnected, Says Wedbush. Should You Buy the Dips? Wedbush Is Bullish on Magnificent 7 Amid the 2-Week Ceasefire. Nvidia Is the Top-Rated Stock to Buy Now. Tech Stocks Are Experiencing Historic 50-Year Weakness. Should You Buy the Dip in This 1 ETF?