The global technology sector rarely stays calm when economic signals start shifting, and earnings season only amplifies that tension. Big enterprise names usually take the first hit, and International Business Machines Corporation (IBM) now finds itself squarely in focus after Needham & Company trimmed expectations.

The firm cut its price target on IBM stock by 14.7% ahead of its Q1 fiscal 2026 results due on Wednesday, Apr.22, after market close. Analyst David Grossman reworked his 2026 model to account for a messy mix of crosscurrents.

More Yield, Less Trap: Sign up free to get Barchart’s daily Dividend Investor newsletter straight to your inbox.

He factored in potential pressure from the U.S.-Iran war upon software and services growth, even as the early closing of the Confluent acquisition adds a clear tailwind. However, foreign exchange movements remain a meaningful drag.

Grossman now sees 2026 constant currency revenue growth landing between 4.5% and 5%, just under the 5% consensus and company guidance. He expects pre-tax income (PTI) margins to expand by 100 basis points year-over-year (YOY), EPS to reach $12.38, up 7%, and free cash flow to climb by $1 billion, also up 7%. The numbers line up broadly with the Street's current standing.

Also, he projects Q1 to come in as expected, given the quarter’s usual softness, its early placement in the year, and a macro backdrop that leaves little room for bold revisions. Still, IBM is holding its ground. The company continues to lean into its defensive strengths, with growth building through software additions like Hashi and Confluent, while a richer software mix and tighter execution steadily push PTI margins higher.

Against this backdrop, Needham’s recalibration reads less like a warning and more like a reset in expectations, keeping the long-term story intact while acknowledging the noise in the near term.

About IBM Stock

Based out of Armonk, New York, IBM has seen enough tech cycles to know how to outlast most of them. The company builds software, runs IT consulting, and still sells hardware, all aimed at helping businesses clean up and modernize how they actually complete work.

With a market cap of about $216.46 billion, IBM’s lineup, which includes Red Hat, watsonx, and those ever-reliable mainframes, keeps some of the world’s most critical data moving across industries.

Yet, the stock has not shown much urgency. Over the last 52 weeks, shares have gained only 0.53%, hinting at a lack of real long-term momentum. More recently, things have tilted south as the stock has dropped 22.1% year-to-date (YTD) and slipped another 7.77% in just the past month.

www.barchart.com

www.barchart.com Valuation looks reasonable. IBM stock is currently trading at 19.10 times forward adjusted earnings, which places it at a discount to the broader industry.

Where IBM really sticks to its script is income. The company has paid dividends for 26 straight years, handing out $6.72 per share annually for a yield of 2.83%. It paid its most recent quarterly dividend of $1.68 per share on March 10 to shareholders on record as of Feb. 10.

IBM Surpasses Q4 Earnings

IBM delivered a strong finish to fiscal 2025. On Jan. 28, it reported Q4 fiscal 2025 results that pushed the stock nearly 5.13% higher in the following trading session. Revenue grew 12.2% YOY to $19.69 billion, beating analyst estimates of $19.21 billion. Adjusted EPS increased 15.3% to $4.52, ahead of the Street’s forecast of $4.29.

Software has become the backbone of the business, now contributing approximately 45% of total revenue, up from about 25% in 2018. During the quarter, software revenue rose 14% YOY to $9 billion. Consulting revenue reached $5.3 billion with 3.4% growth, while infrastructure revenue climbed 20.6% to $5.1 billion.

Non-GAAP adjusted EBITDA increased 16.1% YOY to $6.5 billion. Non-GAAP income from continuing operations rose 16.7% to $4.3 billion, while adjusted free cash flow expanded 22.6% to $7.6 billion during the quarter.

Looking ahead, management expects revenue to grow more than 5% in fiscal year 2026 and anticipates an additional $1 billion increase in free cash flow. And, the company reported that its generative AI book of business exceeded $12.5 billion in 2025 and confirmed that it remains on track to deliver its first large-scale quantum computer by 2029.

On the other hand, analysts expect Q1 fiscal year 2026 EPS to grow 13.1% YOY to $1.81. For the full fiscal year 2026, the bottom line is projected to reach $12.42, reflecting a 7.2% increase, followed by another rise to $13.35 in fiscal year 2027, representing 7.5% growth.

What Do Analysts Expect for IBM Stock?

Wall Street has dialed down expectations, but it has not turned away. Needham & Company lowered its price target on the IT giant to $290 from $340 ahead of IBM’s first quarter results on April 22, signaling tempered expectations in the near term.

Along similar lines, JPMorgan Chase & Co. analyst Brian Essex also held a “Neutral” rating and trimmed his price target from $317 to $283.

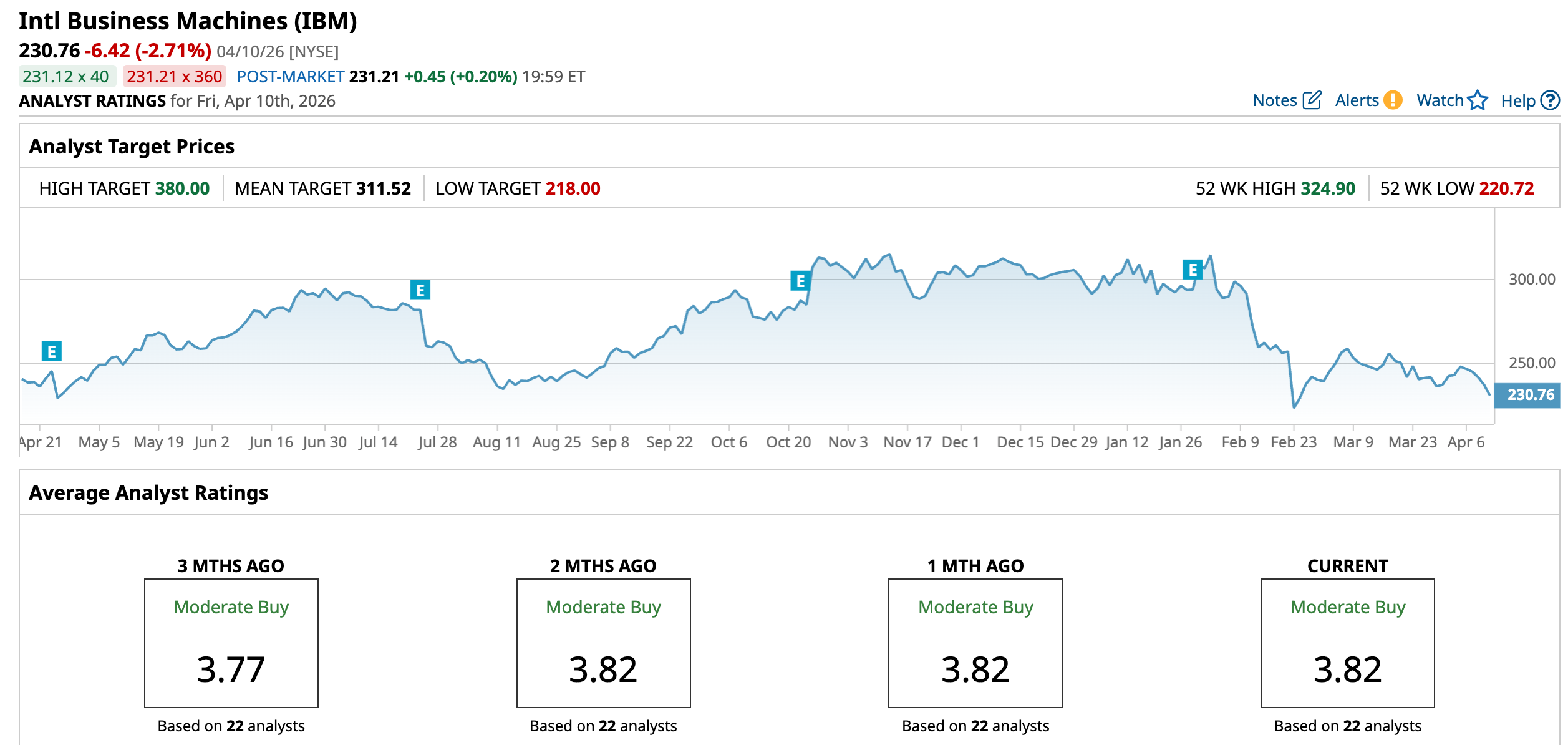

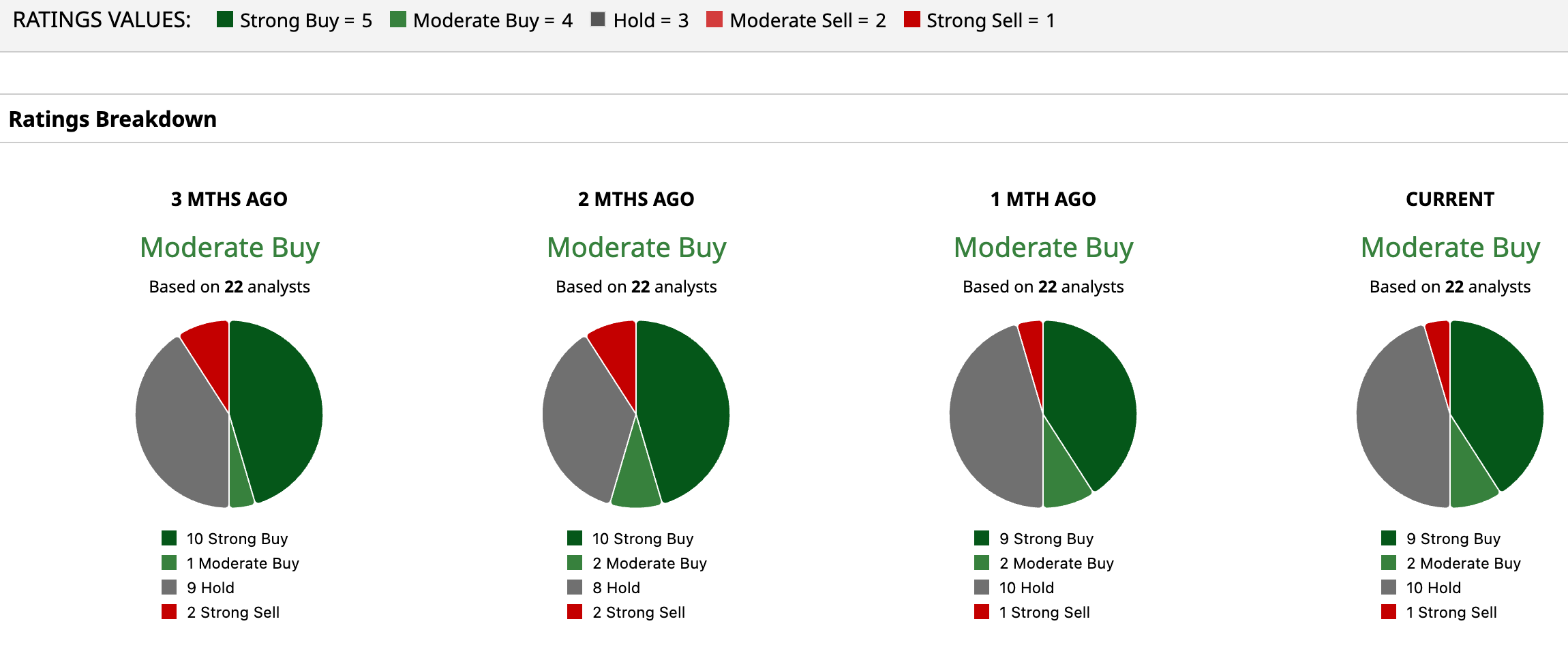

Despite these revisions, IBM stock continues to hold an overall “Moderate Buy” rating. Among 22 analysts covering the stock, nine rate it “Strong Buy,” two assign “Moderate Buy,” 10 recommend “Hold,” and one maintains a “Strong Sell.”

The broader consensus still points to meaningful upside owing to improving fundamentals. The average price target of $311.52 represents potential upside of 35%. Meanwhile, the Street-high target of $380 suggests a gain of 64.67% from current levels.

www.barchart.com

www.barchart.com  www.barchart.com

www.barchart.com On the date of publication, Aanchal Sugandh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Why Needham Analysts Slashed Their Price Targets on IBM Stock Ahead of Earnings 3 Top Stocks to Buy to Invest in Anthropic’s Project Glasswing Dear IBM Stock Fans, Mark Your Calendars for April 22 ConocoPhillips vs. EOG: 1 of These Energy Stocks Is Cheaper and Pays You More. Which One?