Bank of America BAC is scheduled to announce first-quarter 2026 results on April 15, before the opening bell.

One of the biggest banks in the United States, BAC’s performance in 2025 was solid, driven by impressive trading numbers and growth in net interest income (NII). This time also, the company’s performance is expected to have been robust. The Zacks Consensus Estimate for the company’s first-quarter revenues is pegged at $29.64 billion, suggesting 8.3% year-over-year growth.

In the past seven days, the consensus estimate for earnings for the to-be-reported quarter has been unchanged at 99 cents. The figure suggests a 10% rise from the prior-year quarter, as higher NII and solid capital markets business are likely to have supported BAC’s bottom-line growth.

Estimate Revision Trend

Image Source: Zacks Investment Research

Bank of America has an impressive earnings surprise history. The company’s earnings outpaced the Zacks Consensus Estimate in each of the trailing four quarters, the average beat being 7.4%.

Earnings Surprise History

Image Source: Zacks Investment Research

Factors Impacting Bank of America’s Q1 Performance

NII: Per the Fed’s latest data, the demand for commercial and industrial, and consumer loans was impressive in the first quarter, which is expected to have supported overall loan growth for BAC. Likewise, its peers, JPMorgan JPM and Citigroup C, are likely to have recorded a solid lending scenario.

After the rate cuts in 2025, the Federal Reserve kept interest rates unchanged in the to-be-reported quarter. Thus, a solid lending scenario and stabilizing funding/deposit costs are expected to have offered the much-needed support to BAC’s NII.

Bank of America expects NII (tax-equivalent basis) to increase 7% year over year in the quarter. The Zacks Consensus Estimate for NII of $15.67 billion indicates a 7.4% year-over-year increase.

Investment Banking (IB) Fees: Deal-making was impressive in the first quarter despite the Middle Eastern conflict and the ensuing uncertainty about its impact on the economy. While global merger and acquisition (M&A) volume declined year over year, deal value was up as big transactions dominated the space.

Unlike last year, when President Trump’s announcement of ‘Liberation Day’ tariff plans led to a deal drought for several months, this time, companies acknowledged that volatility is part of life, and they will have to do business around it. Lower capital costs and a focus on scale and artificial intelligence (AI) integration drove M&As. Bank of America’s advisory fees are likely to have recorded an improvement.

Also, the first quarter saw decent IPO activity, with issuance volume improving despite fewer companies getting listed. Alternatively, global bond issuance volume was solid. Thus, growth in BAC’s underwriting fees (accounting for almost 40% of total IB fees) is expected to have been strong in the to-be-reported quarter.

The Zacks Consensus Estimate for IB income of $1.71 billion indicates a rise of 12.2% from the prior-year quarter’s actual.

Trading Income: Client activity and market volatility were strong in the first quarter. Major factors that impacted trading business in the quarter included shifting expectations around AI, rising geopolitical tensions, particularly concerns over the Middle East and the risk of an oil shock, persistent inflation concerns and uncertainty around the Fed’s monetary policy stance. Volatility was high in equity markets and other asset classes, including commodities, bonds and foreign exchange. Thus, BAC is likely to have recorded an impressive trading performance this time as well.

The Zacks Consensus Estimate for market making and similar activities of $3.81 billion suggests a 6.3% rise on a year-over-year basis.

Expenses: While Bank of America managed expenses prudently in the past, expansion into new markets by opening financial centers and efforts to digitize operations and upgrade existing financial centers are expected to have kept non-interest expenses elevated in the to-be-reported quarter.

Management anticipates non-interest expenses to rise 4% year over year in the first quarter.

Asset Quality: Bank of America is likely to have set aside a huge amount of money for potential delinquent loans amid a challenging operating backdrop, marked by the Middle East conflict and the apprehensions surrounding the private credit markets.

The Zacks Consensus Estimate for non-performing loans and leases of $6.55 billion implies a 7.7% increase from the prior-year quarter.

What Our Model Reveals About BAC’s Q1 Earnings

Per our proven model, the chances of an earnings beat for BAC are high this time. The combination of a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), 2 (Buy) or 3 (Hold) increases the odds of an earnings beat, which is the case here, as you can see below.

Bank of America has an Earnings ESP of +1.49%. You can uncover the best stocks to buy or sell before they are reported with our Earnings ESP Filter.

The company carries a Zacks Rank #3 at present. You can see the complete list of today’s Zacks #1 Rank stocks here.

BAC’s Price Performance & Valuation Analysis

In the first quarter, BAC shares lost 11.4%, underperforming the S&P 500 Index. In the same time frame, shares of JPMorgan and Citigroup declined 8.7% and 2.8%, respectively.

1Q26 Price Performance

Image Source: Zacks Investment Research

JPMorgan and Citigroup are scheduled to report quarterly numbers on April 14.

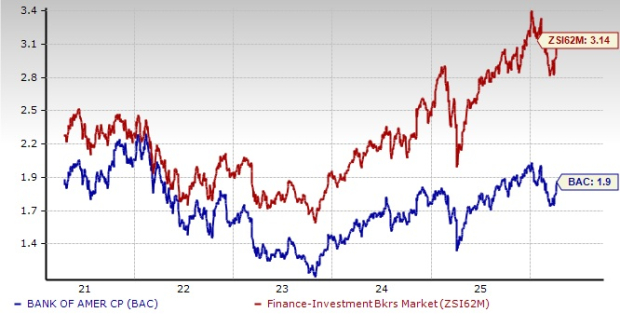

Let us check out the value Bank of America offers investors at current levels. BAC stock is trading at a 12-month trailing price-to-tangible book (P/TB) of 1.90X. This is below the industry’s 3.14X. This shows that the stock is currently inexpensive.

Price-to-Tangible Book (TTM)

Image Source: Zacks Investment Research

The BAC stock is trading at a discount compared with JPMorgan, which has a P/TB of 3.06X. Then again, Citigroup has a P/TB of 1.36X, making it inexpensive compared with Bank of America.

How to Approach BAC Shares Before Q1 Earnings

Given the industry-wide solid lending scenario, along with stabilizing funding costs, Bank of America’s NII growth is expected to be robust in the near term. Management expects NII (FTE basis) to grow 5-7% year over year in 2026.

The company’s aggressive branch expansion across the United States as part of a broader strategy to solidify customer relationships and tap into new markets will further drive NII growth over time. This will also help capitalize on cross-selling opportunities.

Bank of America will continue to benefit from its vast scale, extensive capital markets operations and international footprint (which will drive significant fee income).

However, while Bank of America’s outlook remains constructive, investors may want to avoid rushing to buy the stock. Instead, they should closely watch management’s commentary on how geopolitical risk and market volatility affect performance and how the firm plans to navigate the current environment. Any revisions to BAC’s 2026 guidance for NII, IB, non-interest expenses and asset quality will be especially important, given the recent macro developments. Broader macroeconomic and policy trends that could materially shape the company’s performance trajectory should also be carefully considered.

Existing shareholders may hold BAC stock, given its strong fundamentals and proven resilience. Potential investors should carefully weigh these factors and assess their risk tolerance before initiating new positions.

Quantum Computing Stocks Set To Soar

Artificial intelligence has already reshaped the investment landscape, and its convergence with quantum computing could lead to the most significant wealth-building opportunities of our time.

Today, you have a chance to position your portfolio at the forefront of this technological revolution. In our urgent special report, Beyond AI: The Quantum Leap in Computing Power , you'll discover the little-known stocks we believe will win the quantum computing race and deliver massive gains to early investors.

Access the Report Free Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Bank of America Corporation (BAC): Free Stock Analysis Report

JPMorgan Chase & Co. (JPM): Free Stock Analysis Report

Citigroup Inc. (C): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).