In the evolving automotive industry, suppliers are increasingly defined by their ability to adapt to technologically advanced vehicles, rising content per vehicle and shifting OEM priorities. Magna International MGA and Lear Corporation LEA are two notable players in this space. While Magna operates with a broad, diversified portfolio spanning multiple vehicle systems, Lear remains more focused on seating, with a growing presence in electrical systems. As industry dynamics grow more complex and cost pressures intensify, let’s take a closer look to assess which supplier is better positioned to navigate the auto landscape.

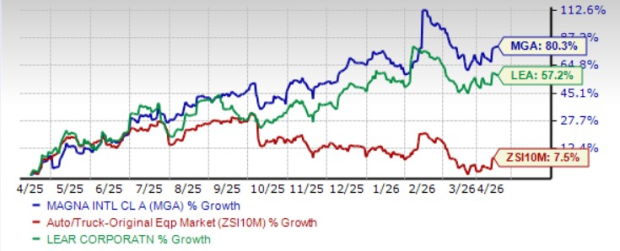

Both companies have outperformed the broader industry over the past year, with Magna leading Lear.

1-Year Price Comparison

Each is currently supported by distinct strengths. Magna benefits from its diversified portfolio, strong booking momentum, strategic technology partnerships, margin expansion and consistent shareholder-friendly capital allocation. Lear, on the other hand, is gaining from strategic acquisitions, new business wins and disciplined capital returns.

Against this backdrop, the key question is: which stock holds the edge at current levels?

The Case for Magna

Magna’s outlook is supported by solid execution and strong visibility into future growth. The company expects to outperform global vehicle production, driven by new program launches and rising content per vehicle. With key wins across both traditional automakers and newer EV players, Magna is building a diversified growth pipeline. Its order book remains a key strength, with a large portion of business already secured for the next few years, providing stability even in a volatile environment.

MGA’s margins are also trending in the right direction. Magna has been improving profitability through tighter cost control and operational efficiencies. The adoption of digital tools, automation and AI-led processes is helping streamline operations, while ongoing restructuring efforts are improving plant utilization and reducing overhead costs. These initiatives have already driven consistent margin expansion, with further gains expected. Magna’s adjusted EBIT margin improved to 5.6% in 2025 and is guided to expand further to 6-6.6% this year.

The company is also well-positioned in areas like ADAS, electrification and power electronics. As vehicles become more software-driven and feature-rich, Magna stands to benefit from higher content per vehicle and growing demand for advanced components. Its collaboration with NVIDIA and advancements in AI-powered safety solutions further strengthen this positioning.

Financially, Magna remains strong, with solid liquidity and a consistent track record of returning capital through dividends and buybacks. At the end of 2025, Magna had over $5.1 billion in liquidity, including over $1.6 billion in cash. In the fourth quarter of 2025, MGA announced a hike in its quarterly dividend, marking the 16th consecutive year of hikes.

Overall, a combination of growth visibility, improving margins and exposure to key industry trends puts Magna in a strong position in the current environment.

The Case for Lear

Lear’s growth strategy is centered on strengthening its core businesses through targeted acquisitions and execution. Recent deals have enhanced its vertical integration in seating, allowing the company to offer more complete, higher-value solutions. Its positioning as a full-seat supplier with integrated thermal comfort systems is a key differentiator, with this segment expected to scale meaningfully over the next few years.

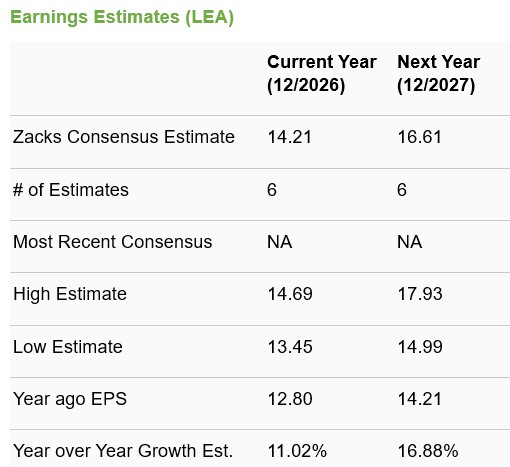

The company’s order momentum also remains strong. Lear continues to secure new business across both Seating and E-Systems, with wins from major global automakers as well as leading Chinese OEMs. These program awards not only support future revenue growth but also provide a clearer path to margin improvement as production ramps up. In 2025, the company won more than $1.4 billion in E-Systems awards, which are expected to support improved margins with the launch of the programs in the coming years. In 2026 and 2027, the company expects approximately $600 million and $725 million, respectively, of net new business.

Operationally, Lear is focused on driving consistent improvement through its internal efficiency initiatives. Ongoing investments in automation and process optimization are generating tangible cost savings, with more benefits expected in the coming years.

Financial discipline is another key strength.Lear maintains a strong cash generation profile and continues to return a significant portion of capital to shareholders through dividends and share buybacks. Supported by a strong cash generation profile, the company expects free cash flow conversion to exceed 80%, enabling share repurchases of more than $300 million in 2026.

Overall, Lear’s focused business model, improving operational efficiency and steady flow of new business position it as a stable player, with clearer near-term execution visibility despite broader industry challenges.

Our Take: MGA Over LEA

Both Magna and Lear are solid investment options, but Magna holds the edge. While Lear offers focused execution and better near-term visibility, Magna’s broader exposure to ADAS, electrification and power electronics positions it for more diversified growth. Its improving margin profile, stronger liquidity and consistent shareholder returns further strengthen the case.

Lear’s disciplined model provides stability, but its narrower scope limits upside relative to Magna’s multi-segment leverage. In an industry demanding both resilience and adaptability, Magna appears better positioned to deliver more balanced and sustainable long-term returns.

While MGA currently sports a Zacks Rank #1 (Strong Buy), LEA carries a Zacks Rank #2 (Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

Beyond Nvidia: AI's Second Wave Is Here

The AI revolution has already minted millionaires. But the stocks everyone knows about aren't likely to keep delivering the biggest profits. Little-known AI firms tackling the world's biggest problems may be more lucrative in the coming months and years.

SeeWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Magna International Inc. (MGA): Free Stock Analysis Report

Lear Corporation (LEA): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).