According to a report by the Financial Times, Facebook parent Meta (META) is building an AI bot resembling its CEO, Mark Zuckerberg. Set to be an internal tool to offer feedback and ideate with employees, the bot will be trained on Zuckerberg's public appearances, tone, thoughts about the company's strategy, and mannerisms. The initiative is aligned with the company's broader ambitions of developing photorealistic 3D avatars that can interact in real time.

This development is not a novel one from the stable of Meta. In 2024, the company's AI Studio platform enabled creators to create AI versions of themselves to communicate with their fanbases via DMs. Although that did not pick up, naysayers should take note of another noteworthy development in the interim.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

ZuckBot & Moltbook: The Possibilities

Last month, Meta acquired Moltbook, a social media platform for generative AI platforms. Built over a weekend through vibe-coding by Matt Schlicht and Ben Parr, it had 2.3 million AI agents on its platform within the first few weeks. With over 700,000 posts and 12 million comments, Moltbook had captured the imagination of the AI world.

However, its fall was as fast as its rise, as humans deserted the platform. A major security issue that exposed over a million credentials and 6,000 email addresses also did not help. Thus, Meta's acquisition of the company certainly raised eyebrows.

But, dig deep, and Meta has now onboarded a duo that has strong expertise in the attention economy. Now a part of the Alex Wang-led Meta Superintelligence Labs (MSL), the co-founders of Moltbook are expected to be valuable additions to MSL. While Schlicht was the CEO of Octane AI, a platform that used AI to assist e-commerce brands and was famous for growing rapper Lil Wayne's Facebook following to over 30 million in a short span of time, before Moltbook, Ben Parr was the co-editor and editor-at-large of the global media and entertainment platform, Mashable.

Coming back to “ZuckBot,” the development should not be seen in isolation, as in combination with Moltbook, there can be some interesting things to look forward to.

For instance, this creates an opportunity for a wholly new enterprise service. Meta can use the Zuckerberg clone as a proof of concept to sell corporate digital twins to other large companies. While the avatars handle human interaction, the Moltbook infrastructure acts as a registry where these corporate bots can verify identities and coordinate tasks securely. This transforms what could be a simple chatbot enhancement into a complete business operating system.

The value proposition for shareholders is also exciting. Meta relies heavily on consumer advertising today. Entering the enterprise software space opens a fresh revenue stream. Enterprise software companies typically trade at higher valuation multiples because of predictable subscription models. Furthermore, deploying this technology internally justifies the projected $135 billion in capital expenditures for 2026. By showing that its massive infrastructure investments have tangible commercial applications outside the metaverse, Meta can build investor confidence.

Metronomic Financials

Meta delivered another strong set of financial results in Q4 2025, returning to form after a one-time tax-related earnings miss in the prior quarter.

Revenue reached $59.9 billion, up 24% year-over-year (YoY), supported by a 6% increase in average price per ad. Earnings per share rose 11% to $8.88, beating the Street consensus of $8.21. Over the past nine quarters, Meta has beaten earnings estimates in eight of them.

The longer-term track record remains impressive, with revenue and earnings compounding at annual rates of 27.34% and 32.27%, respectively, over the past decade.

Notably, daily active people across the Family of Apps grew 7% YoY to 3.58 billion, while operating cash flow for the quarter stood at $36.2 billion. The company ended December with $81.6 billion in cash and equivalents, significantly higher than its short-term debt of $2.2 billion and even exceeding its long-term debt of approximately $59 billion, reflecting balance sheet strength.

In terms of guidance for Q1 2026, Meta guided revenue to a range of $53.5 billion to $56.5 billion. At the midpoint, this implies roughly 30% YoY growth.

However, the elevated valuation remains a concern. The forward P/E of 20.89, P/S of 6.35, and P/CF of 11.74 are all above sector medians of 13.76, 1.18, and 7.36. Yet, the forward PEG ratio of 0.94 sits below the sector median of 1.14, suggesting META stock appears relatively attractive when growth is considered.

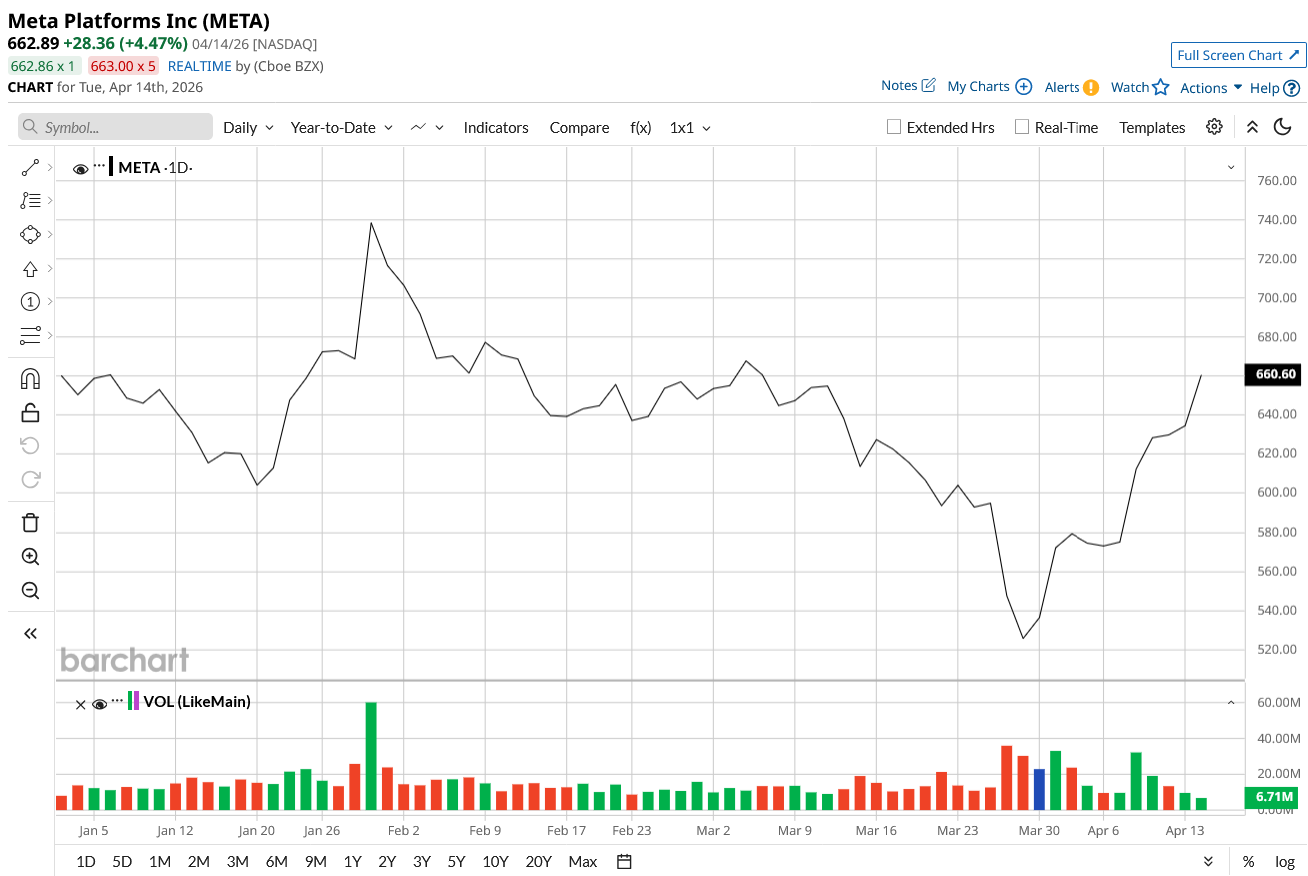

Valued at a market cap of $1.6 trillion, META stock is down 0.35% on a year-to-date (YTD) basis.

www.barchart.com

www.barchart.com Analyst Opinion on META Stock

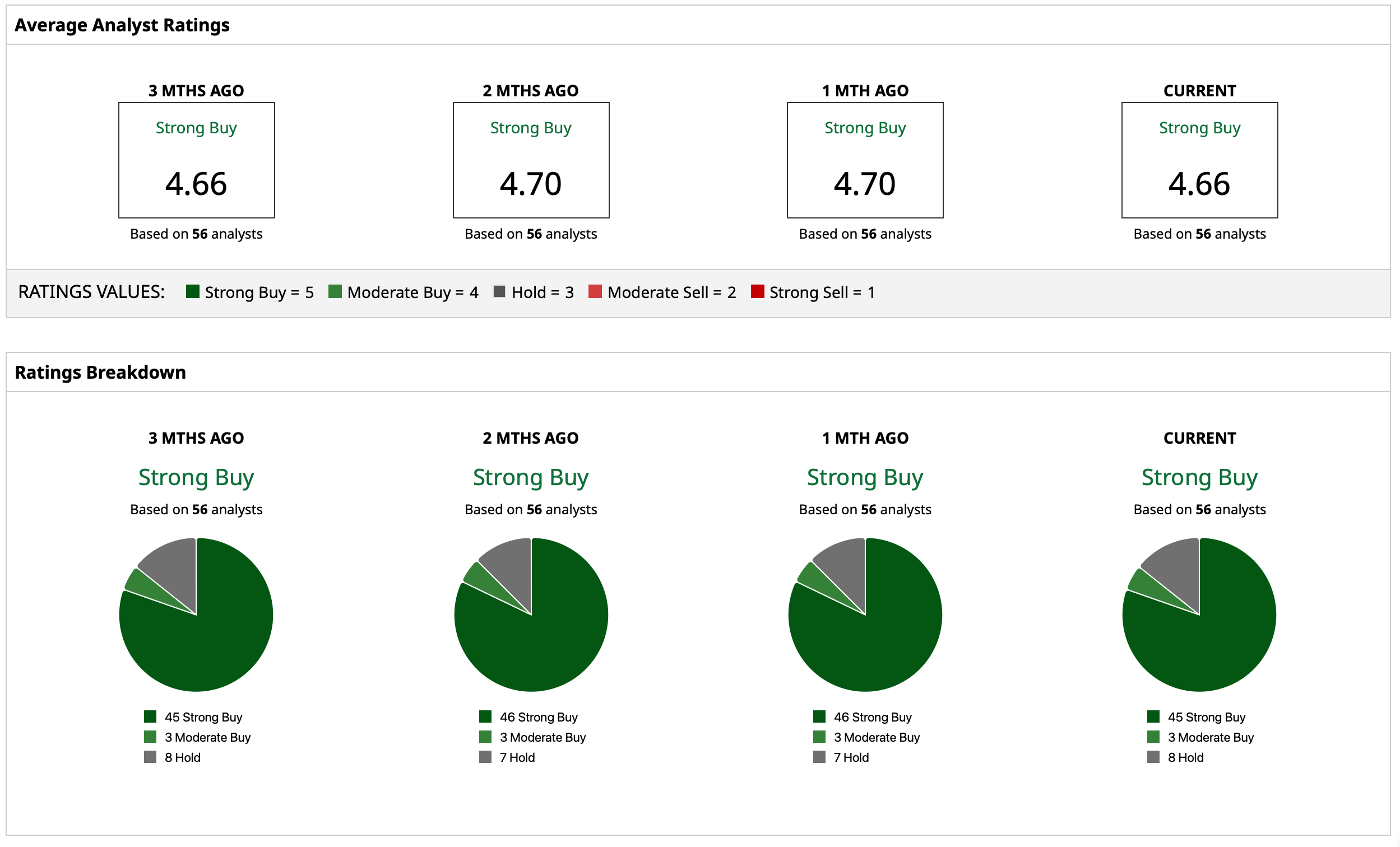

Thus, analysts have attributed a consensus rating of “Strong Buy” for META stock, with a mean target price of $856.25. This denotes an upside potential of about 29% from current levels. Out of 56 analysts covering the stock, 45 have a “Strong Buy” rating, three have a “Moderate Buy” rating, and eight have a “Hold” rating.

www.barchart.com

www.barchart.com On the date of publication, Pathikrit Bose did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

As Intel and Google Team Up on Infrastructure, Which Is the Better Tech Stock to Buy? Cathie Wood Is Buying the Palantir Stock Dip. Should You? Why Citi Analysts Are Betting IBM Stock Can Gain Nearly 20% From Here 2% Inflation Is Holding the Federal Reserve Hostage: This Is What the Stock Market Desperately Needs to Keep Growing