Micron Technology, Inc. MU has delivered a sharp improvement in profitability, driven largely by the ongoing artificial intelligence (AI) boom. The company’s non-GAAP gross margin improved 1,730 basis points to 56.8% in the first quarter of fiscal 2026 and increased 3,700 basis points to 74.9% in the second quarter.

Micron Technology’s third-quarter non-GAAP gross margin guidance of 81% signals continued expansion. Strong pricing, richer product mix and operating leverage are likely to continue aiding profitability expansion.

AI demand is the biggest driver. AI servers require significantly higher memory content, especially DRAM and high-bandwidth memory (HBM). This allows Micron Technology to sell premium products at higher prices, directly supporting margins. At the same time, industry supply remains tight, with demand still exceeding available capacity through 2026. This imbalance keeps pricing firm and reduces the risk of sudden margin pressure.

Micron Technology is shifting toward high-margin products like HBM and advanced DRAM nodes, while maintaining cost discipline. These efforts are improving efficiency and sustaining profitability.

Overall, strong AI demand, tight supply and a favorable product mix suggest Micron Technology’s margin expansion can continue, at least in the near term.

How Do MU’s Semiconductor Peers Compare on Margins?

NVIDIA Corporation NVDA and Advanced Micro Devices, Inc. AMD are key players benefiting from the AI boom, though their margin profiles differ from Micron Technology.

NVIDIA leads the AI ecosystem with its graphics processing units, and its margins are significantly higher due to strong pricing power and software-driven revenues. In the last reported financial results for the fourth quarter of fiscal 2026, NVIDIA reported a non-GAAP gross margin of 75.2%, a 170-basis-point year-over-year expansion, supported by high demand for AI accelerators.

Advanced Micro Devices is also gaining from AI server demand, especially with its EPYC central processing units and AI accelerators. In the fourth quarter of 2025, Advanced Micro Devices’ gross margin expanded 290 basis points year over year to 57%.

Micron’s Price Performance, Valuation and Estimates

Shares of Micron Technology have surged around 571.7% over the past year compared with the Zacks Computer – Integrated Systems industry’s return of 132.6%.

Micron One-Year Price Return Performance

Image Source: Zacks Investment Research

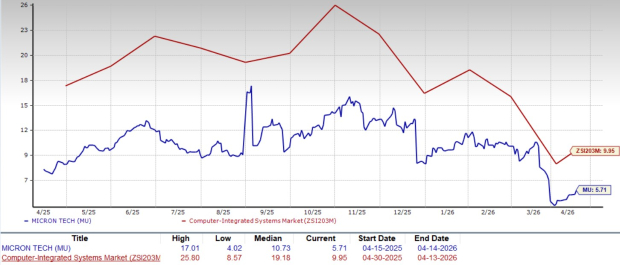

From a valuation standpoint, MU trades at a forward price-to-earnings ratio of 5.71, significantly lower than the industry’s average of 9.95.

Micron 12-Month Forward P/E Ratio

Image Source: Zacks Investment Research

The Zacks Consensus Estimate for Micron Technology’s fiscal 2026 and 2027 earnings implies a year-over-year increase of 604% and 63.9%, respectively. Bottom-line estimates for fiscal 2026 and 2027 have been revised upward in the past 30 days.

Image Source: Zacks Investment Research

Micron Technology currently sports a Zacks Rank #1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

5 Stocks Set to Double

Each was handpicked by a Zacks expert as the #1 favorite stock to gain +100% or more in the coming year. While not all picks can be winners, previous recommendations have soared +112%, +171%, +209% and +232%.

Most of the stocks in this report are flying under Wall Street radar, which provides a great opportunity to get in on the ground floor.

Today, See These 5 Potential Home Runs >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Advanced Micro Devices, Inc. (AMD): Free Stock Analysis Report

Micron Technology, Inc. (MU): Free Stock Analysis Report

NVIDIA Corporation (NVDA): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).