Cisco Systems CSCO reported strong momentum in its networking business during the second quarter of fiscal 2026, with revenues reaching $8.29 billion. This marked a 21% year-over-year increase and a 6.8% sequential rise. The growth was driven by solid demand for AI infrastructure and campus networking solutions. Cisco’s expanding portfolio — powered by Silicon One, AI-native security offerings and advanced operating systems — is helping the company strengthen its presence in the rapidly growing AI market.

Cisco’s growth outlook is fueled by strong momentum in its product portfolio. In the fiscal second quarter, networking product orders continued to accelerate, growing more than 20% and marking the sixth straight quarter of double-digit expansion. This performance was driven by broad-based demand across key areas, including service provider routing, data center switching, campus switching, wireless, servers and industrial IoT Solutions.

Cisco is witnessing strong demand for next-generation campus networking solutions, including Wi-Fi 7, smart switches and secure routers. Backed by AI-driven technologies and Silicon One, networking orders rose 20% in the second quarter of fiscal 2026, marking six straight quarters of double-digit growth and supporting continued revenue expansion in fiscal 2026.

Recently, Cisco released its inaugural State of Wireless Report, which highlights a major structural shift in enterprise networking, positioning wireless infrastructure as a core growth engine in the AI era. The report underscores that enterprises are rapidly transitioning from viewing Wi-Fi as basic connectivity to treating it as a strategic asset that directly drives business outcomes.

This shift is fueled by the rapid adoption of AI-driven applications, the proliferation of IoT devices, the increasing use of bandwidth-intensive workloads such as 4K/8K streaming and AR/VR and evolving workplace trends like hybrid work, BYOD and hot-desking. As a result, enterprise wireless networks are now central to real-time decision-making, customer engagement platforms and automated operations. This plays directly into Cisco’s strength in enterprise networking, campus switching and wireless solutions, creating a multi-year upgrade cycle. A key insight of the report is the “multiplier effect,” where wireless investments improve efficiency, productivity, customer engagement and revenues. This positions Cisco as a strategic digital transformation partner rather than just a hardware provider.

CSCO Faces Tough Competition in the Networking Domain

Cisco is facing stiff competition from Arista Networks ANET and Hewlett-Packard HPE in the networking domain.

Arista Networks holds a leadership position in 100-gigabit Ethernet switches and is increasingly gaining market traction in 200 and 400-gigabit high-performance switching products. ANET’s advanced cloud-native software and smart Wi-Fi solutions deliver intelligent application identification, automated troubleshooting and location services. These solutions efficiently support apps like Teams, Zoom and Google Meet. The Arista 2.0 strategy is resonating well with customers, as its modern networking platforms are foundational for the transformation from silos to data centers.

Hewlett Packard Enterprise views AI, Industrial Internet of Things (IoT) and distributed computing as the next major markets. The acquisition of Juniper Networks has elevated Hewlett Packard Enterprise’s competitive stance by expanding its networking domain in AI, cloud and hybrid solutions. Its multi-billion-dollar investment plan for expanding networking capabilities will diversify the business from the server and hardware storage markets and boost margins in the long run.

CSCO Share Price Performance, Valuation & Estimates

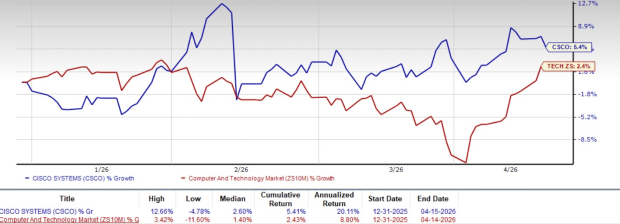

Cisco shares have gained 5.4% in the year-to-date period, outperforming the broader Zacks Computer and Technology sector’s return of 2.4%.

CSCO Stock Outperforms Sector

Image Source: Zacks Investment Research

CSCO stock is trading at a premium, with a trailing 12-month price/book of 6.84X compared with the Zacks Computer Networking industry’s 6.54X. Cisco has a Value Score of D.

CSCO Stock Is Overvalued

Image Source: Zacks Investment Research

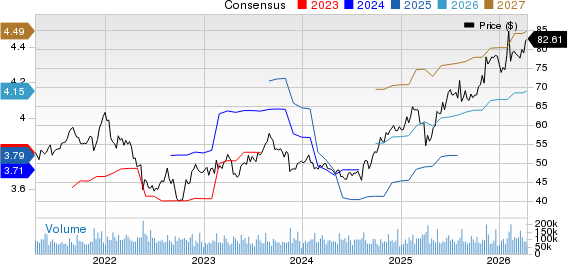

The Zacks Consensus Estimate for third-quarter fiscal 2026 earnings is currently pegged at $1.04 per share, unchanged over the past 30 days, suggesting 8.33% growth from the figure reported in the year-ago quarter.

Cisco Systems, Inc. Price and Consensus

Cisco Systems, Inc. price-consensus-chart | Cisco Systems, Inc. Quote

Cisco currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

5 Stocks Set to Double

Each was handpicked by a Zacks expert as the #1 favorite stock to gain +100% or more in the coming year. While not all picks can be winners, previous recommendations have soared +112%, +171%, +209% and +232%.

Most of the stocks in this report are flying under Wall Street radar, which provides a great opportunity to get in on the ground floor.

Today, See These 5 Potential Home Runs >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Cisco Systems, Inc. (CSCO): Free Stock Analysis Report

Arista Networks, Inc. (ANET): Free Stock Analysis Report

Hewlett Packard Enterprise Company (HPE): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).