Berkshire Hathaway (BRK.A) (BRK.B) has once again tapped Japan’s bond market, raising 272.3 billion yen—roughly $1.7 billion—in a multi-tranche offering that marks the company’s third-largest yen deal on record. The transaction is notable not only for its size but also because it represents the first such issuance since Greg Abel officially took over the reins from Warren Buffett. That alone has drawn attention from investors eager to see how Abel will deploy Berkshire’s capital in his early tenure as CEO.

For investors, this deal is about more than just bond math. It offers an early glimpse into how Greg Abel may approach capital allocation at Berkshire. So what does this $1.7 billion move really signal, and what implications could it have for Berkshire’s strategy going forward? Let’s take a closer look.

Join 200K+ Subscribers: Find out why the midday Barchart Brief newsletter is a must-read for thousands daily.

About Berkshire Hathaway Stock

Berkshire Hathaway Inc., based in Omaha, Nebraska, is a diversified holding company. It operates under a decentralized management structure, granting its many subsidiaries considerable autonomy in their operations. Berkshire’s insurance division includes property, casualty, life, accident, and health insurance, as well as reinsurance services. Its freight rail transportation business is run through BNSF Railway, one of the largest railroad networks in North America. In the utilities segment, Berkshire Hathaway Energy produces and delivers electricity from a range of sources, including natural gas, coal, wind, and solar. Berkshire also engages in manufacturing, service, and retail businesses. Its market cap currently stands at $1.03 trillion.

Shares of the conglomerate have fallen 5.4% on a year-to-date (YTD) basis. The weak performance comes as Berkshire is arguably the most defensive megacap stock in the market, with its $373 billion cash pile representing nearly 40% of its market capitalization.

www.barchart.com

www.barchart.com A Deep Dive Into Berkshire’s $1.7 Billion Sale of Yen Bonds

Last Friday, Berkshire Hathaway issued 272.3 billion yen ($1.7 billion) in yen-denominated bonds, marking its first such offering since Greg Abel assumed leadership from his legendary predecessor, Warren Buffett.

The six-tranche deal included maturities spanning from three to 30 years, according to Bloomberg. The 10-year notes were reportedly priced at a spread of 90 basis points above benchmarks, carrying a 3.084% coupon. This represents a significant increase in borrowing costs compared to Berkshire’s previous yen deal in November 2025, where the 10-year coupon was 2.422%. At this point, let’s take a closer look at what drove this difference and what it could mean for Berkshire.

The first key point to highlight is that the “benchmarks” referenced in the previous paragraph are TONA-based yen mid-swaps rather than Japanese Government Bond (JGB) yields. Because JGB yields were historically suppressed by Yield Curve Control, market participants shifted to TONA (Tokyo Overnight Average) mid-swaps as a more transparent, market-driven reference for corporate and foreign debt. When a foreign issuer such as Berkshire Hathaway sells yen-denominated bonds, the pricing is quoted as a spread over the swap rate. Put simply, the final interest rate, or coupon, is determined by adding a fixed premium (or margin) to the benchmark swap rate. In this equation, TONA-based yen mid-swaps act as a proxy for the risk-free rate. That said, we can calculate the implied risk-free rate at the time of Berkshire’s issuance by subtracting the 90-basis-point margin from the 3.084% coupon, which results in 2.184%. This also confirms that the “benchmarks” were not 10-year JGB yields, which were trading in the range of 2.396% to 2.442% last Friday.

Now, let’s turn to the most interesting component in determining the final interest rate—the fixed premium, or spread, paid over the swap rate. The spread foreign bond issuers pay over TONA-based yen mid-swaps acts as a direct measure of risk perception and market liquidity in Japan’s financial sector. In other words, the spread is a barometer for investor confidence. Increased volatility in the Japanese bond market often causes spreads over TONA to widen as investors demand higher risk premiums. And that was clearly the case with Berkshire’s issuance this month. Japan’s 10-year government bond yields climbed to their highest levels since 1997 earlier this week, as concerns that rising energy prices stemming from the Middle East conflict will accelerate inflation fueled expectations of a rate hike from the Bank of Japan as early as this month. Japan’s 10-year yields have been in an uptrend since early April through last Friday, and spreads on Berkshire’s notes moved higher as well. According to Bloomberg, the spread was around 85 basis points for the 10-year note when first discussed on April 3, then widened to 85–90 basis points on April 7 and further to 88–90 basis points on April 8.

In a reflection of bond market volatility, Berkshire’s 10-year notes were priced at a yield higher than those of lower-rated Samurai issuers such as Credit Agricole SA and the Republic of Poland, both of which accessed the Samurai market earlier this year. Still, the deal was heavily subscribed, demonstrating strong investor demand for high-grade foreign issuers in Japan. It marked Berkshire’s third-largest yen issuance on record, trailing only its 430 billion yen debut in 2019 and a 281.8 billion yen offering in October 2024.

To sum up, Berkshire’s 10-year bonds had a higher coupon this time because both the risk-free rate and the margin were higher than during its previous sale in November. The higher coupon means Berkshire will pay more to service its debt. The risk-free rate was higher because the Bank of Japan raised its short-term policy rate by 25 basis points to 0.75% in December 2025, driving up benchmark JGB yields and, in turn, the swap rate, as the two tend to move in tandem. The Iran war, which triggered a surge in oil prices and heightened inflation concerns, further pressured Japanese government bonds while also leading investors to demand higher risk premiums.

Why Did Greg Abel Make Berkshire’s Third-Largest Yen Deal on Record?

Berkshire’s yen bond offerings are closely monitored by investors amid speculation that the proceeds could be used to increase its holdings in Japanese companies. Over the past year, the conglomerate increased its equity stakes in Japanese trading houses Itochu Corp. (ITOCY), Mitsubishi Corp. (MUFG), and Mitsui & Co. (MITSY). In late March, it agreed to invest roughly 300 billion yen in insurer Tokio Marine Holdings (TKOMY). According to a filing with the U.S. Securities and Exchange Commission, the proceeds will be used primarily to refinance Berkshire’s yen bonds maturing in 2026 and to finance a portion of its investment in Tokio Marine Holdings. Notably, two bonds totaling 133.9 billion yen are scheduled to mature this month.

By borrowing in yen to fund Japanese assets, Berkshire creates a “natural hedge” against currency fluctuations. This allows the company to invest in Japanese firms without being exposed to a potential weakening of the yen. And over the past month, it has become clear why this is important. The U.S.-Israel war with Iran has placed renewed pressure on the yen, with the currency weakening beyond 160 per dollar in late March for the first time since July 2024.

Last but not least, you may be wondering why Berkshire didn’t simply wait for bond market volatility tied to the Iran war to ease to secure a tighter spread. Well, we already have part of the answer in the SEC filing—namely, the need to refinance yen bonds maturing in 2026, including two that come due this month. And the second key point is that, at the start of April, traders were pricing in more than a 70% chance of a BOJ rate hike this month. If that were to materialize, the risk-free rate would rise further, potentially leading to an even higher coupon.

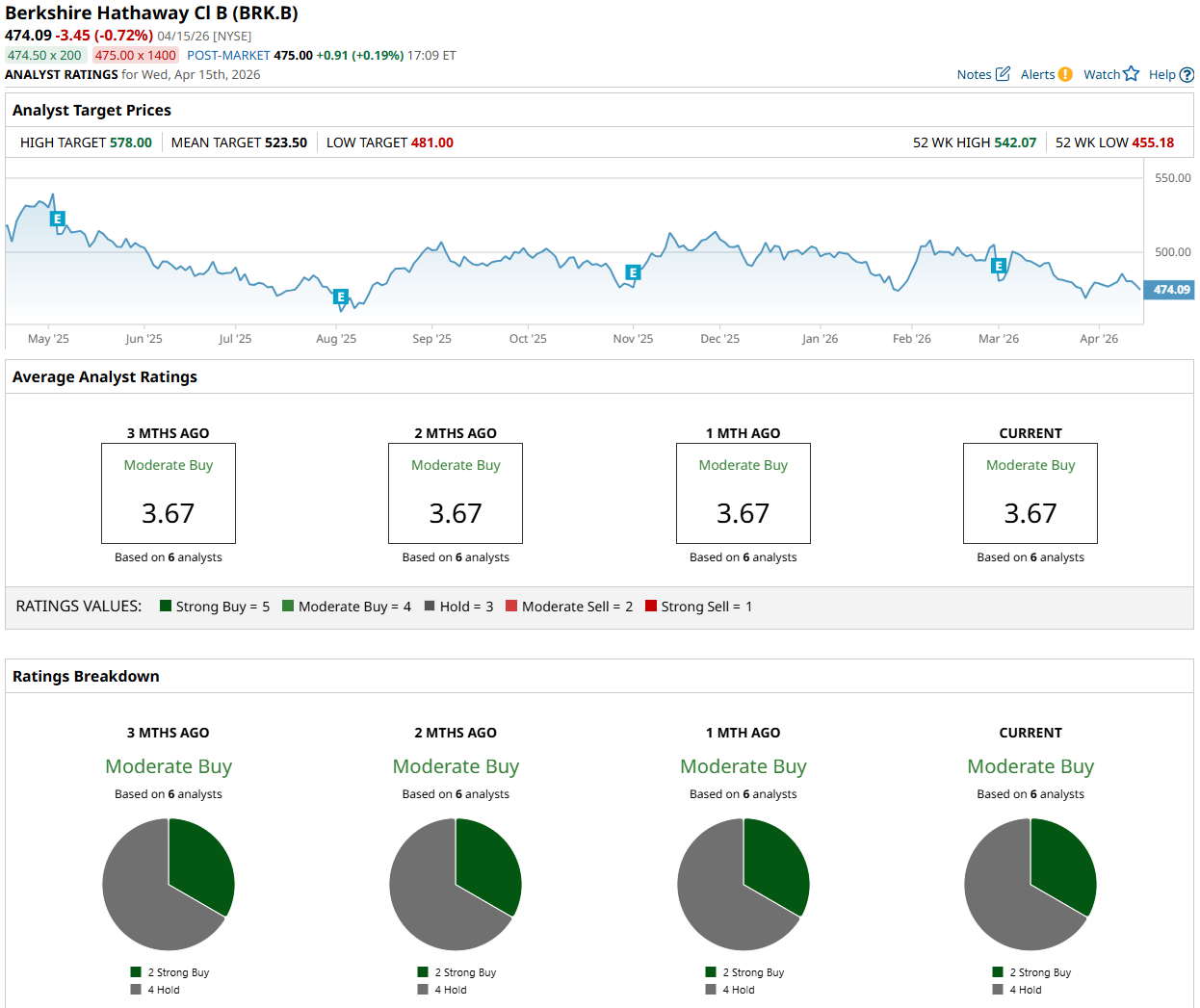

What Do Analysts Expect for BRK Stock?

Wall Street analysts have a consensus rating of “Moderate Buy” on Berkshire’s Class B shares. Among the six analysts covering the stock, two assign a “Strong Buy” rating, while the remaining four advise holding. The average price target for BRK.B stock is $523.50, implying a potential upside of 10.4% from current levels.

www.barchart.com

www.barchart.com On the date of publication, Oleksandr Pylypenko did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

How Should You Trade Marvell Technology Stock at New Record Highs? Coca-Cola Stock Is Typically a Defensive Name. Options Data Says It’s Time to Go on the Offense. Apple CEO Tim Cook Just Bought Another 25,000 Shares of Nike Stock. Should You Load Up on NKE Too? Berkshire Hathaway Just Sold $1.7 Billion in Yen Bonds. What Does That Mean and Why Did New Greg Abel Make the Company’s Third-Largest Yen Deal Ever?