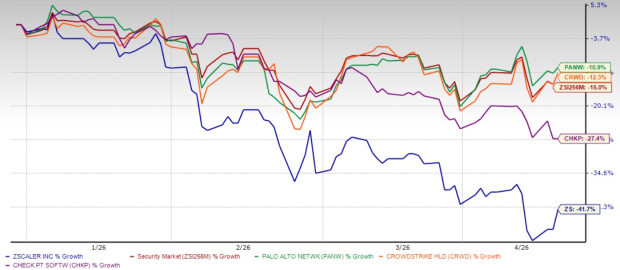

Zscaler, Inc. ZS shares have dropped a steep 41.7% year to date (YTD), making it one of the weakest performers in the broader cybersecurity space. This decline stands out even more when compared with the overall Zacks Security industry, which has plunged 15%. Importantly, this is not a Zscaler-only issue.

Major peers like Palo Alto Networks, Inc. PANW, CrowdStrike Holdings, Inc. CRWD and Check Point Software Technologies Ltd. CHKP have also seen notable corrections. YTD, shares of Palo Alto Networks, CrowdStrike Holdings and Check Point Software have fallen 10.9%, 12.3% and 27.4%, respectively.

Zscaler YTD Price Return Performance

Image Source: Zacks Investment Research

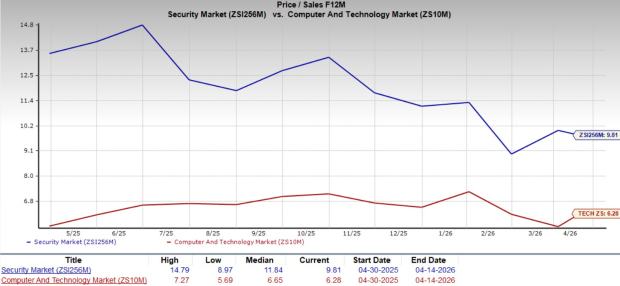

This broader sell-off signals an industry-wide reset rather than a company-specific collapse. Investors seem to have been reassessing their positions amid the increasing competition in the cybersecurity space and the industry’s historically high valuations. Despite the recent sell-off, the Zacks Security industry currently trades at a forward 12-month price-to-sales (P/S) ratio of 9.81, significantly higher than the Zacks Computer and Technology sector’s average of 6.28.

Image Source: Zacks Investment Research

Geopolitical instability, especially the ongoing conflict in the Middle East, is adding another layer of uncertainty. Rising energy prices and inflation concerns are making investors cautious.

Zscaler’s outlook is exposed to ongoing macroeconomic uncertainty and geopolitical tensions that can affect enterprise IT spending. In uncertain economic environments, businesses often delay large IT spending, which can slow new deal activity and expansion revenues. Since Salesforce’s revenues come from enterprise customers, any slowdown in corporate budgets could directly impact growth.

Despite all these headwinds, writing off Zscaler entirely would be short-sighted. The stock’s decline reflects a broader market correction, but not necessarily a broken business. On the valuation front, the recent sell-off has now made Zscaler stock attractive. Compared to its major peers, it trades at a lower P/S ratio than Palo Alto Networks and Check Point Software. At present, Zscaler, Palo Alto Networks, Check Point Software and CrowdStrike have P/S multiples of 5.58, 10.53, 16.93 and 4.83, respectively.

Zscaler’s Resilient Financial Performance

Despite macroeconomic pressures, Zscaler’s financial results remain impressive. In the second quarter of fiscal 2026, revenues soared 26% year over year to $816 million, with emerging products growing at a faster rate than core offerings. Non-GAAP earnings jumped approximately 29.5% to $1.01 per share.

Zscaler’s growing customer base underscores its strong market positioning. At the end of the second quarter, it had 728 customers generating $1 million or more in annual recurring revenues (ARR), with Fortune 500 and Global 2000 companies comprising a substantial portion. At the end of the second quarter, more than 45% of the Fortune 500 companies and approximately 40% of the Global 2000 companies are using Zscaler’s solutions.

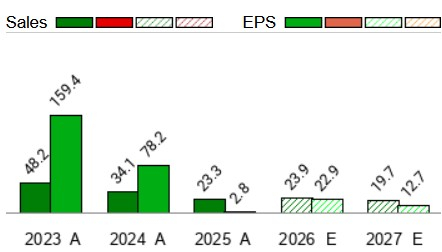

Zscaler is poised to benefit from enterprise migration to cloud environments, the increasing adoption of AI-driven cybersecurity and a recovery in IT spending. Its focus on large-scale enterprise deals and innovation pipeline is expected to drive accelerated growth in 2026 and beyond. The Zacks Consensus Estimate for fiscal 2026 and 2027 indicates strong double-digit revenue and earnings per share growth.

Zscaler Sales And EPS Growth Estimates

Image Source: Zacks Investment Research

Strategic Investments to Fuel Zscaler’s Long-Term Growth

Zscaler remains at the forefront of the cybersecurity space through its innovative efforts. The company’s three main growth areas — AI Security, Zero Trust Everywhere and Data Security Everywhere — have together crossed the $1 billion annual recurring revenue (ARR) milestone, growing faster than the company’s overall business.

AI Security’s ARR is expected to exceed $500 million in fiscal 2026 as enterprises adopt AI Guard and agentic operations. Zero Trust Everywhere has already attracted more than 550 enterprises, achieving its goal of 390 enterprises quarters ahead of the initial target date. Data Security Everywhere is witnessing strong upsell opportunities as most customers use only a few modules today. These three pillars are likely to create strong, diversified drivers for Zscaler’s future growth.

Zscaler is taking an early lead in AI security, a fast-growing area of enterprise demand. The company processed nearly 1 trillion AI transactions in calendar 2025, showing how quickly enterprises are adopting AI. To address new risks like prompt injection and model poisoning, Zscaler launched AI Guard, which is now being tested by large customers.

Its Agentic Operations portfolio is also gaining traction and is expected to contribute significantly to AI Security ARR in fiscal 2026. With the integration of recently acquired Red Canary’s AI technology, Zscaler is building a differentiated AI-powered security operations center solution, positioning itself as a trusted vendor for securing AI applications.

Zscaler’s Z-Flex program is helping the company win bigger and more strategic multi-year deals. Introduced just four quarters ago (the third quarter of fiscal 2025), Z-Flex already delivered more than $290 million in total contract value bookings in the second quarter of fiscal 2026, a 65% sequential increase. The program gives customers the flexibility to adopt multiple modules over time under predictable pricing, making it easier to expand usage. This model encourages long-term commitments, strengthens customer relationships, and supports sustainable growth in fiscal 2026 and beyond.

Conclusion: Hold Zscaler Stock for Now

Although Zscaler faces challenges related to macroeconomic uncertainties, the company’s heavy investment in AI, innovative cybersecurity capabilities and growing adoption of its solutions make the stock worth retaining at present.

Zscaler currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Zacks' Research Chief Picks Stock Most Likely to "At Least Double"

Our experts have revealed their Top 5 recommendations with money-doubling potential – and Director of Research Sheraz Mian believes one is superior to the others. Of course, all our picks aren’t winners but this one could far surpass earlier recommendations like Hims & Hers Health, which shot up +209%.

See Our Top Stock to Double (Plus 4 Runners Up) >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Check Point Software Technologies Ltd. (CHKP): Free Stock Analysis Report

Palo Alto Networks, Inc. (PANW): Free Stock Analysis Report

Zscaler, Inc. (ZS): Free Stock Analysis Report

CrowdStrike (CRWD): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).