The negative sentiment around software stocks does not seem to be going anywhere. As the likes of Anthropic's Claude come up with new capabilities frequently, software skeptics' obituaries keep increasing in number. Predicting the irrelevance of their services or offerings as tools like OpenClaw and Codex see increasing adoption by the day, software companies are expected to find it tough going for them.

Adding to the clamor recently has been major brokerage Piper Sandler, which lowered its price target on Microsoft (MSFT) to $500 from $600, still implying an upside potential of roughly 22% from current levels.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

What remains indisputable, though, is that Microsoft remains a behemoth. Its market cap of close to $3 trillion and its AI prowess make it hard to believe that, at the current juncture, Microsoft will suddenly become irrelevant. What does that mean for MSFT stock as an investment option? Let's find out.

Financials Do Justice To Microsoft's Megacap Status

Setting aside what the naysayers are saying, a look into Microsoft's financials aptly reflects why it has been held in such high regard among market participants for several decades now. While over the past 10 years, the company has grown its revenue and earnings at CAGRs of 13.24% and 16.12%, respectively, its market cap has soared 10x in the same period.

Further, the results for the most recent quarter saw the company surpassing revenue estimates by a billion dollars, along with its earnings reporting a beat for the ninth consecutive time.

Microsoft's revenue for Q2 2026 came in at $81.3 billion, a rise of 16.7% from the previous year. The burgeoning cloud segment continued to report strong growth at 26% on a YoY basis to $51.5 billion as commercial remaining performance obligation increased 110% to $625 billion, not bad for a company perceived to become irrelevant.

Earnings also increased. This time by 23.6% from the year-ago period to $4.14 per share, coming in ahead of the consensus estimate of an EPS of $3.90. For Q3 2026, the company expects revenue to be between $80.65 billion and $81.75 billion, with Wall Street estimates for the same being around $81.4 billion.

Meanwhile, in Q2 2026, Microsoft's net cash from operations was at $35.8 billion. This was a rise from the prior year's figure of $22.3 billion. Overall, Microsoft ended 2025 with a cash balance of $24.3 billion, much higher than its short-term debt levels of $4.8 billion.

Moreover, the recent drawdown in the stock (down 14% on a YTD basis) has brought the company's valuation to comfortable levels. While its forward P/S at 8.90 is a bit far away from the sector median of 3.04, its forward P/E and P/CF of 23.52 and 17.81 are within the range of the sector medians of 22.84 and 17.56, respectively.

www.barchart.com

www.barchart.com Ignore Microsoft at Your Own Peril

Microsoft is executing a massive capital expenditure expansion, committing over $120 billion for fiscal 2026. This aggressive ramp-up represents a massive leap from the roughly $80 billion deployed in 2025. Recent quarterly figures highlight this urgency, with fiscal second quarter 2026 capex hitting an eye-watering $37.5 billion, primarily directed at processing units and facility builds. For instance, to support Azure cloud growth, which recently jumped 39%, the tech giant is acquiring huge land parcels like a 3200-acre Wyoming site.

Further, to counter the likes of OpenClaw and Codex, Microsoft is using its massive capex budget to secure absolute dominance in raw compute power. By building gigawatt-scale facilities and pouring funds into hyperscale infrastructure alongside OpenAI, the company aims to offer decentralized agents an inescapable foundation. Thus, instead of fighting the localized wave head-on, Microsoft is positioning Azure as the ultimate utility provider, betting that even the most nimble, self-hosted tools will eventually require its massive computing grid to process complex enterprise workloads.

As such, Microsoft has introduced its new Microsoft 365 E7 Frontier Suite, which is scheduled to become available at the beginning of May. This offering combines the core security features of the E5 plan with the complete capabilities of Copilot, along with the innovative Agent 365 control plane. The development marks a significant move away from traditional per-user licensing toward value-driven AI-based subscriptions. In this model, the higher pricing is supported by the ability to automate various business workflows effectively.

In addition, Microsoft has launched Copilot Cowork, which enables AI to serve as a proactive member of a team instead of operating merely as a standard chatbot. This new tool can handle extended tasks and complex multi-step processes that develop gradually over time. These capabilities are supported by Work IQ, a fresh organizational memory system designed to analyze communication habits and previous choices made within the company.

Furthermore, through the creation of its own specialized silicon technology, Microsoft is working to limit its dependence on Nvidia (NVDA) over the long term. This effort centers on the Maia 200 AI accelerator chips, which are expected to help safeguard the company’s profit margins in the years ahead. Microsoft has also embraced a multi-model approach, allowing Copilot to choose the most suitable artificial intelligence model for each particular task. This includes incorporating the Claude model when advanced reasoning is required. The introduction of the MAI foundational models further demonstrates the company’s plan to compete aggressively with OpenAI and Google (GOOG) (GOOGL), not only in distributing models but also in developing them internally.

Overall, projections indicate that Azure AI could generate an extra $25.7 billion in revenue during 2026. The broader sovereign AI sector and the entire cloud computing market are anticipated to expand to $156.2 billion in the same year. Microsoft is positioning itself to benefit from this growth by making targeted investments in regional infrastructure. Examples include a commitment of $10 billion in Japan as well as additional initiatives in Singapore and across Europe.

Analyst Opinion on MSFT Stock

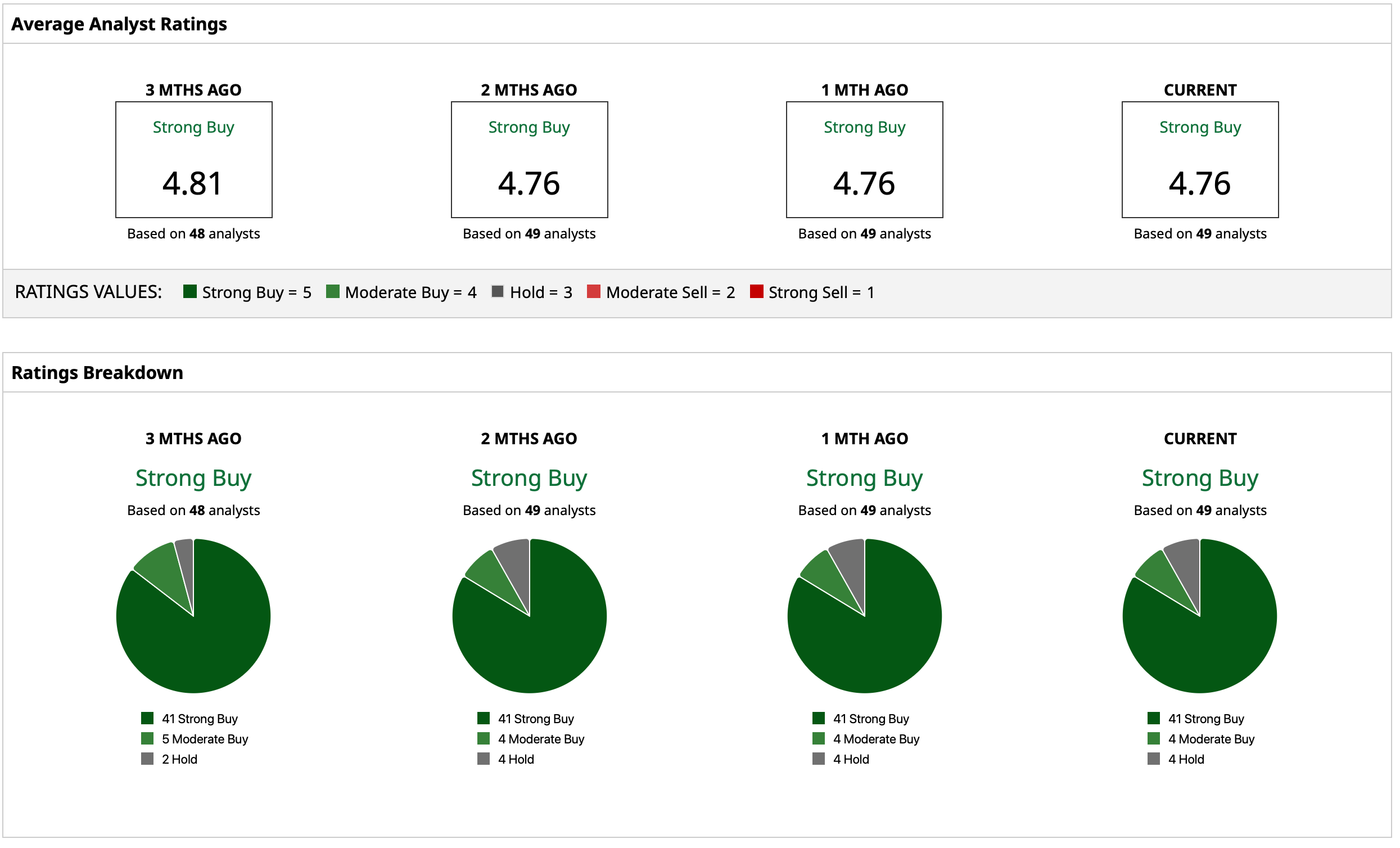

Thus, analysts have attributed to MSFT stock an overall rating of “Strong Buy,” with a mean target price of $582.38, indicating an upside potential of about 43% from current levels. Out of 49 analysts covering the stock, 41 have a “Strong Buy” rating, four have a “Moderate Buy” rating, and four have a “Hold” rating.

www.barchart.com

www.barchart.com On the date of publication, Pathikrit Bose did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Up Nearly 60% in 5 Days, Should You Chase the Rally in D-Wave Quantum Stock? CEO Eliott Hill Just Bought 24,000 Shares of Nike Stock. Should You? Analysts Are Divided Over Tesla Ahead of Q1 Earnings, but TSLA Stock Is a Buy Anyway Microsoft Stock Warning: Why Piper Sandler Analysts Just Slashed Their MSFT Price Target by More Than 15%