Shares of fuel cell energy services provider Bloom Energy (BE) climbed 24% on April 14 following an announcement that cloud infrastructure major Oracle (ORCL) has extended its partnership with the company. As part of the agreement, Oracle will secure 2.8 gigawatts (GW) of Bloom's fuel cell systems to assist in its AI infrastructure buildout.

Commenting on the development, Executive Vice President of Oracle Cloud Infrastructure Mahesh Thiagarajan said, “By rapidly deploying Bloom's reliable, efficient fuel cell energy, we are quickly meeting the demands of our customers across the United States.” Weighing in, Bloom Chief Commercial Officer Aman Joshi remarked, "Together, we are defining a shared vision for the future of energy and AI infrastructure, with Bloom advancing its position as the standard for onsite power."

Don’t Miss a Day: From crude oil to coffee, sign up free for Barchart’s best-in-class commodity analysis.

About Bloom Energy

Founded in 2001 and based in San Jose, California, Bloom Energy designs and sells solid oxide fuel cell (SOFC) systems. Bloom Energy serves end markets such as data centers, utilities, hospitals, telecom, and infrastructure, among others.

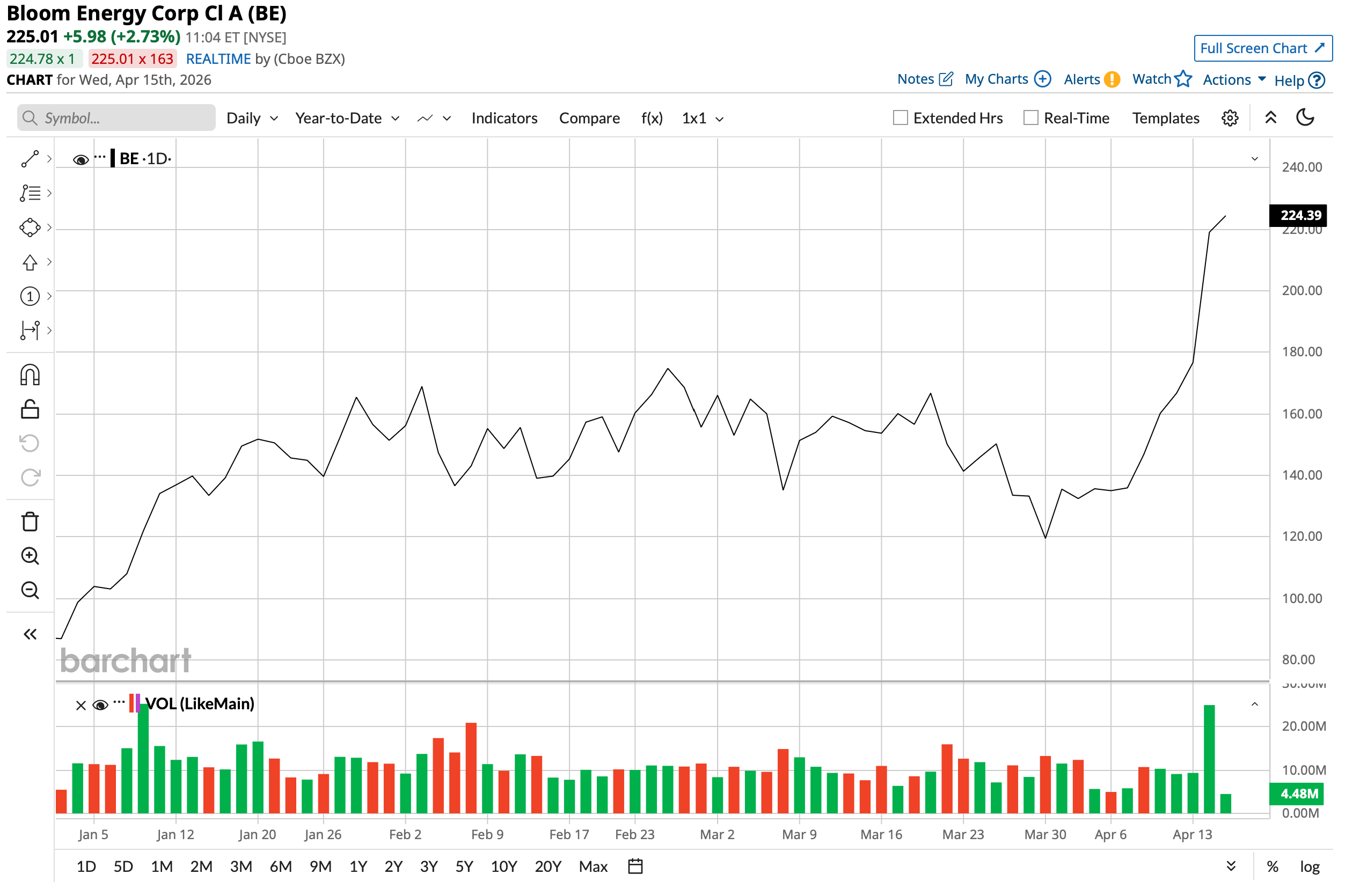

Valued at a market capitalization of about $59 billion, BE stock is up an impressive 142% on a year-to-date (YTD) basis.

www.barchart.com

www.barchart.com So, does Bloom have what it takes to bloom further? Let's take a closer look.

A Strong Q4, Uncomfortable Valuations

Bloom Energy closed 2025 with a bang, marked by record revenues, a sizeable backlog, and rising earnings. The fourth quarter of 2025 saw revenue of $777.7 million, up almost 36% year-over-year (YOY). The product segment — the core revenue segment of the company — witnessed yearly growth of 35% to $638.5 million as Bloom closed the year with a hefty backlog of $20 billion.

Meanwhile, diluted EPS remained almost flat at $0.45 per share, compared to $0.43 per share in the year-ago period. However, earnings comfortably outpaced the consensus estimate of $0.31 per share.

Net cash from operating activities at $418.1 million saw a slight decline when compared to the prior year's figure of $484.2 million, as a hit to the net profits flowed down into the cash flows. Overall, Bloom Energy closed the quarter with a cash balance of $2.45 billion.

The strong financials and the share price rally have come at the cost of punchy valuations for BE stock. Its forward price-to-earnings (P/E), price-to-sales (P/S), and price-to-cash flow (P/CF) ratios of 223 times, 30.3 times, and 548.4 times are all trading at substantially higher levels when compared to the respective sector medians.

What Makes Bloom Energy Different?

To service the huge demand for power in the massive AI buildout, Bloom Energy is embarking on a unique path. The company is offering rapidly deployable, behind-the-meter generation that completely bypasses congested utility grids. While traditional grid connections for gigawatt-scale data centers can take over five years, the company delivers solid oxide fuel cells in as little as 50 days.

Furthermore, Bloom's differentiation lies in a high operating temperature and continuous, load-following efficiency. Unlike proton exchange membrane systems from peers like Plug Power (PLUG) that are tailored for mobility, or molten carbonate systems from FuelCell Energy (FCEL), Bloom provides always-on, stationary baseload power with a 54% electrical efficiency. When configured for combined heat and power to run data-center cooling loops, total system efficiency exceeds 90%. Bloom plans to sustain this competitive advantage through direct 800-volt direct current integration into server racks, eliminating costly energy losses associated with alternating current conversions.

Regarding the primary bottlenecks facing the company and its mitigation strategies, Bloom Energy's overarching challenges involve supply-chain vulnerabilities and the long-term transition away from fossil fuels. For one, Bloom's solid-oxide architecture relies heavily on scandium, a rare earth element largely refined in China. Management is actively overcoming this by diversifying procurement across multiple continents to avoid dependence any single geopolitical entity. Additionally, while the systems currently run predominantly on natural gas — facing intense regulatory and environmental scrutiny — the technology is inherently independent of fuel. Bloom is mitigating long-term obsolescence risk by ensuring its fuel cells are entirely hydrogen-ready, allowing a seamless transition as zero-carbon infrastructure matures globally.

What Do Analysts Think of Bloom Energy Stock?

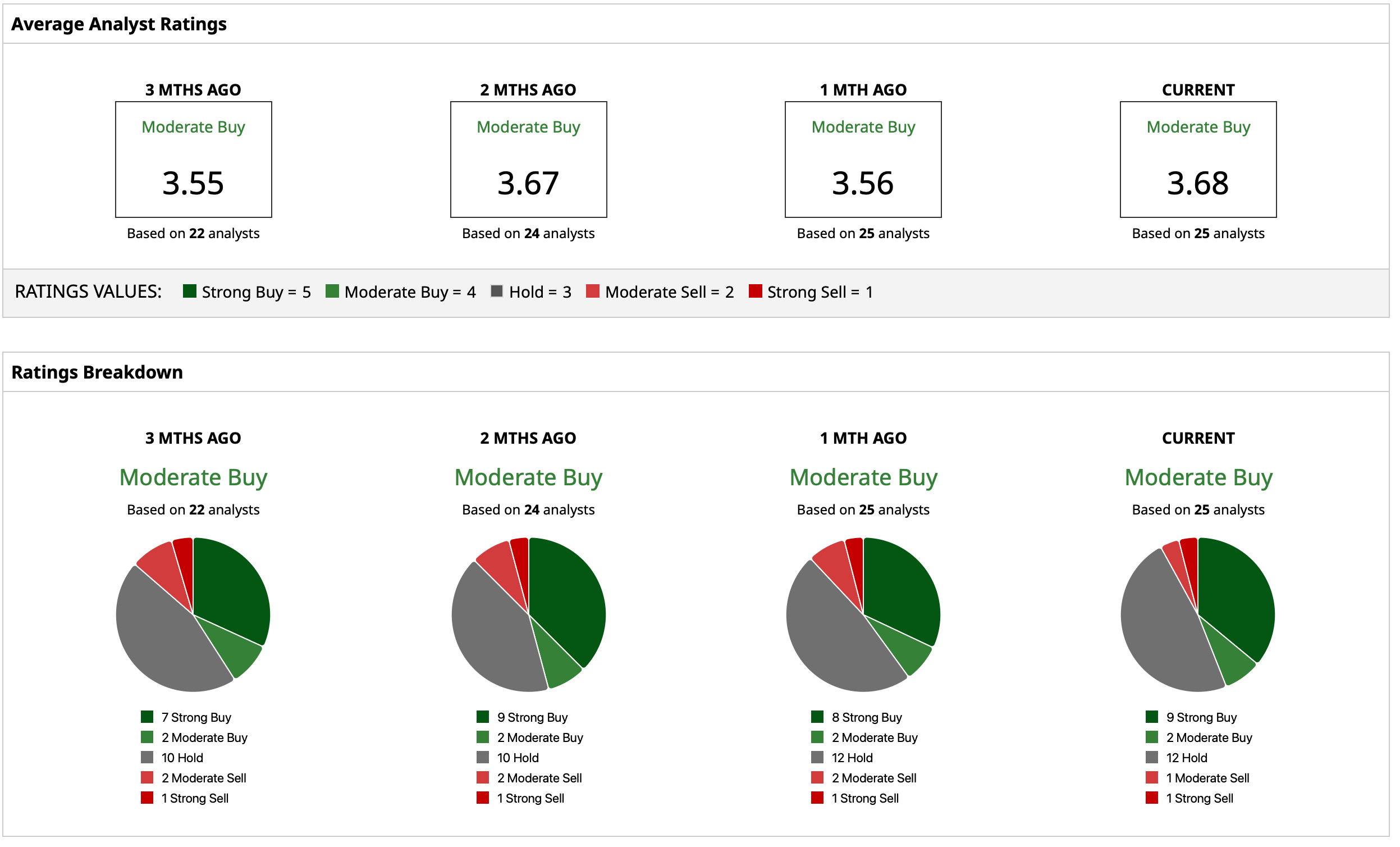

Taking all of this into account, analysts attribute a consensus “Moderate Buy” rating to BE stock. The mean target price of $154.18 has already been surpassed by BE, while the high target price of $231 implies potential upside of 10% from current levels — a glowing testament to Bloom Energy's share price performance. Out of 25 analysts covering BE stock, nine have a “Strong Buy” rating, two have a “Moderate Buy” rating, 12 analysts have a “Hold” rating, one has a “Moderate Sell,” and one has a “Strong Sell” rating.

www.barchart.com

www.barchart.com On the date of publication, Pathikrit Bose did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

AMD Stock Is in Overbought Territory. Is It Too Late to Snag Shares Now? Bloom Energy Just Partnered With Oracle. Does That Make the Fuel Cell Energy Stock a Buy Here? Wall Street Is Bullish on GE Aerospace Before Q1 Results — Buy GE Stock Now? BIRD Stock Shot Way Into Overbought Territory on the Allbirds AI Pivot. What’s the Trade Here?