Mirum Pharmaceuticals’ MIRM top line is primarily being driven by its lead product, Livmarli (maralixibat), which has seen steady sales growth since its launch. The drug remains a key contributor to the company’s revenues.

Livmarli is an orally administered ileal bile acid transporter (“IBAT”) inhibitor currently approved worldwide for the treatment of cholestatic pruritus in patients with Alagille syndrome (“ALGS”). The drug is also approved for treating certain patients with progressive familial intrahepatic cholestasis (“PFIC”) in the United States and Europe.

The FDA has also approved a new tablet formulation of Livmarli for treating cholestatic pruritus in ALGS and PFIC patients, a move expected to improve convenience for older patients.

In 2025, Livmarli’s net product sales were $360 million, up 68.8% year over year. Building on this growing momentum, we expect investors to keep a close eye on Livmarli’s sales performance when Mirum reports its first-quarter 2026 results.

The continued demand for Livmarli is expected to drive MIRM’s top line in the first quarter.

The Zacks Consensus Estimate for Livmarli’s first-quarter sales stands at $105 million.

Besides Livmarli, Mirum is also making good progress with its other marketed products — Cholbam capsules and Ctexli tablets, which are approved for certain rare diseases. These products were added to Mirum’s commercial portfolio following the acquisition of Travere Therapeutics’ TVTX bile acid products in 2023.

The acquisition of Travere Therapeutics’ bile acid products has diversified Mirum’s revenue stream. Sales from the bile acid products, comprising Cholbam and Ctexli tablets, also contributed meaningfully to MIRM’s top line in 2025.

Mirum expects worldwide net product sales of approximately $630-$650 million in 2026, reflecting strong Livmarli adoption and incremental sales from the bile acid products.

Meanwhile, Mirum’s lead pipeline candidate, volixibat, is currently being evaluated in two phase IIb studies for treating patients with primary biliary cholangitis (the VANTAGE study) and primary sclerosing cholangitis (the VISTAS study). The company recently initiated the phase II BLOOM study on its newly in-licensed PDE4D inhibitor, MRM-3379, for treating Fragile X syndrome, a rare genetic neurocognitive disorder.

MIRM’s Competition in the Target Market

Though Mirum is riding on the robust sales performance of Livmarli, the company’s heavy reliance on the drug for revenues remains a concern. Any regulatory setback for the drug in the days ahead could hurt the stock.

Competition is also rising from Albireo AB (now part of Ipsen), which markets Bylvay — an IBAT inhibitor directly competing with Livmarli in the PFIC and ALGS indications. Since both therapies work by inhibiting IBAT to lower serum bile acid levels, competition is likely to intensify and it could impact Mirum’s market share and revenue trajectory. Bylvay is considered the most direct competitor for Livmarli in the PFIC and ALGS markets.

Also, last month, GSK plc GSK announced that the FDA has approved Lynavoy (linerixibat) for the treatment of cholestatic pruritus in adult patients with primary biliary cholangitis (PBC).

Previously, GSK signed a license agreement with Italy-based Alfasigma, wherein the latter acquired exclusive global rights to develop and market Lynavoy for the given indication.

Though still in the early days, the FDA nod to Lynavoy is likely to pose stiff competition for Mirum’s volixibat.

MIRM’s Price Performance, Valuation and Estimates

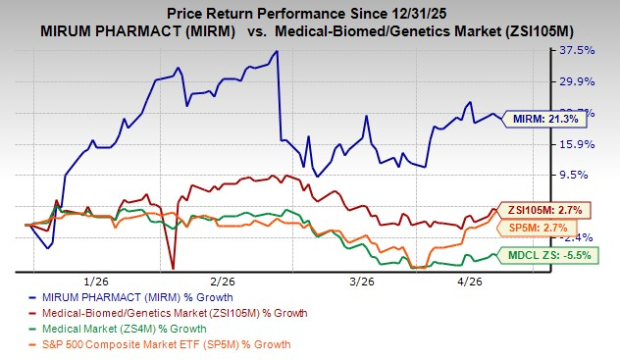

Year to date, shares of Mirum have rallied 21.3% compared with the industry’s rise of 2.7%. The stock has also outperformed the sector and the S&P 500 during the same time frame, as seen in the chart below.

Image Source: Zacks Investment Research

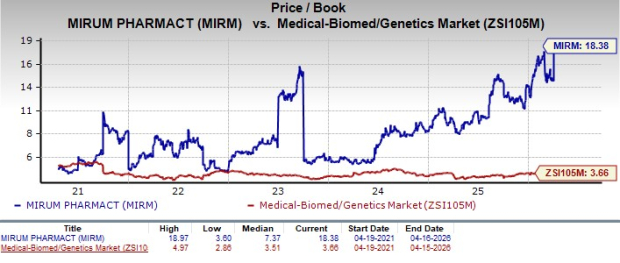

From a valuation standpoint, Mirum is trading at a premium to the industry. Going by the price/book ratio, the company’s shares currently trade at 18.38, higher than 3.66 for the industry. The stock is also trading above its five-year mean of 7.37.

Image Source: Zacks Investment Research

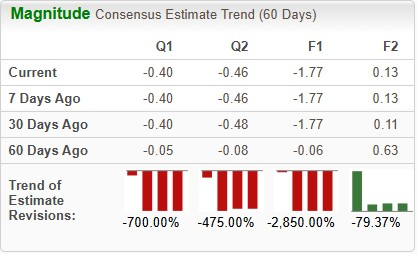

The Zacks Consensus Estimate for its 2026 loss per share has widened from 6 cents to $1.77 over the past 60 days. During the same time frame, estimates for 2027 earnings per share have declined from 63 cents to 13 cents.

Image Source: Zacks Investment Research

MIRM's Zacks Rank

Mirum currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

#1 Semiconductor Stock to Buy (Not NVDA)

The incredible demand for data is fueling the market's next digital gold rush. As data centers continue to be built and constantly upgraded, the companies that provide the hardware for these behemoths will become the NVIDIAs of tomorrow.

One under-the-radar chipmaker is uniquely positioned to take advantage of the next growth stage of this market. It specializes in semiconductor products that titans like NVIDIA don't build. It's just beginning to enter the spotlight, which is exactly where you want to be.

See This Stock Now for Free >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

GSK PLC Sponsored ADR (GSK): Free Stock Analysis Report

Mirum Pharmaceuticals, Inc. (MIRM): Free Stock Analysis Report

Travere Therapeutics, Inc. (TVTX): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).