The renewable fuels industry is experiencing a structural transformation — from a commodity-based market toward a policy-backed, decarbonization-oriented energy sector, focusing more on low-carbon, higher-value fuel. Demand is mostly shaped by low-carbon fuel standards and clean fuel tax credits, with global capacity expected to triple by 2028 as per a Bain & Company report. In this context, Alto Ingredients ALTO and Gevo Inc. GEVO are worth mentioning.

Alto is a leading producer and distributor of specialty alcohols, renewable fuels and essential ingredients in the United States. It is poised to gain from its compelling portfolio, its focus on customer relationships, and its leveraging of technologies. On the other hand, Gevo is a leading renewable chemicals and advanced biofuels company.

Let's discuss in detail.

The Case for ALTO

Alto Ingredients is undergoing a strategic transformation, shifting away from its legacy role as a traditional fuel ethanol producer toward a more diversified model centered on specialty alcohols and essential ingredients. By leveraging its long-standing operational expertise and existing infrastructure, the company is targeting higher-value end markets that offer more stable demand and improved margins.

The business has broadened its portfolio beyond commodity ethanol into specialty alcohols and ingredients used in pharmaceuticals, personal care, food, and industrial applications. This move is intended to reduce reliance on volatile ethanol pricing while maximizing the value of its assets and customer relationships.

A major pillar of this strategy is lowering carbon intensity scores to benefit from the federal Section 45Z clean fuel tax credit. Management is focusing on capital-efficient projects with defined timelines and strong returns, alongside initiatives to enhance environmental performance. If targets are achieved and credits are monetized, Section 45Z could generate up to $18 million in incremental gross benefits during 2025–2026.

Additionally, Alto is expanding carbon capture and utilization at its Pekin and Columbia plants, building on its Carbonic acquisition. By commercializing fermentation-derived CO2, the company is developing a higher-margin revenue stream that supports both sustainability goals and earnings diversification.

Operational discipline remains a priority, with ongoing cost reductions, exits from underperforming segments, and investment in near-term, high-return opportunities. Early progress, including increased renewable fuel export sales, highlights the flexibility of its platform.

Improved profitability has supported debt reduction, with $10 million repaid in February 2026 and another $6 million in March, bringing term debt to $39 million by the end of the first quarter. For 2026, Alto plans approximately $25 million in capital expenditures. However, the business remains capital-intensive and sensitive to fluctuations in corn and natural gas prices.

ALTO shares have risen 71.6% year to date.

The Case for GEVO

Gevo has evolved from a pre-revenue technology developer into an early-stage operating company, with improving EBITDA and cash generation indicating reduced execution risk. The company is focused on commercializing sustainable aviation fuel (SAF) through its proprietary alcohol-to-jet (ATJ) technology, while positioning itself as a vertically integrated producer of low-carbon fuels. Its model combines ethanol production, carbon capture and sequestration and SAF conversion.

The Gevo North Dakota facility highlights this integrated approach, producing low-carbon ethanol alongside carbon removal credits and renewable natural gas. Management views the acquisition and integration of the Red Trail Energy assets—now operating as Gevo North Dakota—as a turning point. This transaction has significantly improved adjusted EBITDA and enabled the company to better monetize carbon as a valuable co-product, in addition to ethanol, animal feed and oil.

Strong operational performance at the North Dakota facility, coupled with insights into carbon value capture, supported Gevo’s transition to positive operating cash flow in the fourth quarter. The company has also achieved three consecutive quarters of positive non-GAAP adjusted EBITDA, reflecting consistent operational progress.

In early 2026, Gevo strengthened its balance sheet by consolidating debt and increasing cash levels without issuing new equity. At the same time, it continues to advance development of its ATJ-30 plant, a key SAF project planned for the North Dakota site.

Gevo’s diversified revenue model—spanning fuel sales, carbon credits and tax incentives—positions it for steady growth. The company expects to generate approximately $40 million in annualized non-GAAP adjusted EBITDA and achieve neutral to positive operating cash flow for full-year 2026.

Nonetheless, GEVO is not expected to be profitable soon. Shares have lost 14% year to date.

Estimates for ALTO and GEVO

The Zacks Consensus Estimate for ALTO’s 2026 revenues implies a year-over-year increase of 7.7%, while that for EPS implies a year-over-year increase of 171.4%. However, EPS estimates witnessed no movement in the past 30 days.

Image Source: Zacks Investment Research

The Zacks Consensus Estimate for GEVO’s 2026 revenues implies a year-over-year increase of 18.5%, and that for EPS implies a year-over-year increase of 42.9%. EPS estimates witnessed no movement in the past 30 days.

Image Source: Zacks Investment Research

Are ALTO and GEVO Shares Expensive?

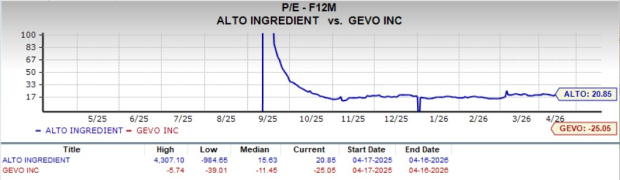

ALTO is trading at a forward price to earnings multiple of 20.85, above its median of 15.63 over the past year. GEVO’s forward price-to-earnings multiple sits at negative 25.05, wider than its median of negative 11.45 over the past year.<

Image Source: Zacks Investment Research

Conclusion

Alto’s transition, strategic buyouts, focus on lowering carbon intensity score, cost-control efforts and its VGM Score of A instill confidence.

Gevo targets sustainable aviation fuel using ethanol-to-jet pathways and carbon capture. SAF mandates and partnerships are tailwinds, while high capex, execution delays, and funding risk are headwinds.

ALTO, with a less expensive valuation, better price appreciation and a Zacks Rank #1 (Strong Buy), has an edge over GEVO, which carries a Zacks Rank #3 (Hold).

You can see the complete list of today’s Zacks #1 Rank stocks here.

#1 Semiconductor Stock to Buy (Not NVDA)

The incredible demand for data is fueling the market's next digital gold rush. As data centers continue to be built and constantly upgraded, the companies that provide the hardware for these behemoths will become the NVIDIAs of tomorrow.

One under-the-radar chipmaker is uniquely positioned to take advantage of the next growth stage of this market. It specializes in semiconductor products that titans like NVIDIA don't build. It's just beginning to enter the spotlight, which is exactly where you want to be.

See This Stock Now for Free >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Gevo, Inc. (GEVO): Free Stock Analysis Report

Alto Ingredients, Inc. (ALTO): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).