Black Diamond Therapeutics BDTX is a clinical-stage oncology company with a story that is simple and high stakes. The upside case is tied to one drug, silevertinib, and the market’s willingness to underwrite its next data points.

Early results suggest the asset may differentiate in EGFR-mutant non-small cell lung cancer through broad mutation coverage and meaningful central nervous system activity. That focus makes 2026 execution the central swing factor for the shares.

BDTX Setup: What the Market Is Paying For

BDTX is effectively a single-asset equity. Silevertinib is the company’s only wholly owned clinical asset, and valuation is largely a function of whether upcoming milestones reinforce a differentiated profile in EGFR-mutant disease.

With no approved products, the near-term narrative is not about commercial revenue. It is about clinical durability, progression metrics, and continued evidence that the drug’s mutation coverage and brain penetration can translate into a compelling risk-benefit profile in populations where central nervous system disease is a defining problem.

Black Diamond’s Cash Runway and Funding Overhang

The balance sheet reduces immediate financing pressure but does not remove it from the debate. Black Diamond ended 2025 with $128.7 million in cash, cash equivalents, and investments and guided that liquidity into the second half of 2028.

That runway matters because it spans key catalysts, including the expected progression-free survival update in the second quarter of 2026 and additional clinical updates tied to response durability. The longer the company can fund operations without tapping the market, the more valuation can be driven by data rather than by dilution risk.

BDTX Licensing Deal With Servier and Why It Matters

The out-licensing of BDTX-4933 to Servier provided meaningful non-dilutive leverage. Under the agreement, Servier took global development and commercialization responsibility, and Black Diamond received a $70 million upfront payment in March 2025.

The structure keeps upside exposure through potential economics that scale with success. Black Diamond is eligible for up to $710 million in development and commercial milestones, plus tiered royalties on global net sales. For a company prioritizing its lead program, that kind of back-end optionality can support the funding profile without forcing the investment thesis to depend on near-term equity issuance.

Black Diamond’s Expense Reset and Loss Trajectory

Recent operating results show the impact of restructuring and portfolio focus. In fourth-quarter 2025, Black Diamond posted an adjusted net loss of $0.14 per share versus a $0.28 loss in the year-ago period, reflecting a narrower loss base.

Expense reductions were the driver. Research and development expense fell nearly 49% to $6.3 million and general and administrative expense declined about 34% to $4.0 million. Total operating expenses were $17.6 million versus $18.3 million a year earlier, even with a $7.3 million non-cash impairment charge.

BDTX Catalysts That Can Reprice the Shares in 2026

Near-term repricing hinges on whether the clinical story strengthens in ways that investors can model. The company has flagged upcoming updates on duration of response and progression-free survival as key valuation catalysts.

A key checkpoint is the expected progression-free survival data in the second quarter of 2026 for the phase II program in non-small cell lung cancer. In parallel, partnership execution remains important, with management highlighting the role of strategic collaborations as a swing factor as the lead program advances.

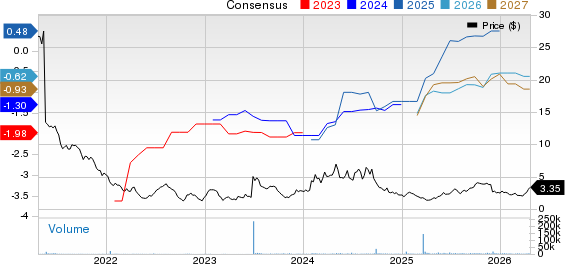

Black Diamond Therapeutics, Inc. Price and Consensus

Black Diamond Therapeutics, Inc. price-consensus-chart | Black Diamond Therapeutics, Inc. Quote

Black Diamond’s Competitive Reality Check in NSCLC

Competition is a real headwind in non-small cell lung cancer, and it shapes how much differentiation BDTX must prove. AstraZeneca AZN remains a defining incumbent with Tagrisso, a widely approved third-generation EGFR tyrosine kinase inhibitor across major markets.

Johnson & Johnson JNJ also has a strengthened first-line position with FDA approval of Rybrevant in combination with Lazcluze for EGFR exon 19 deletions or exon 21 L858R substitution mutations. Against that backdrop, BDTX’s opportunity is not simply about market size. It is about whether silevertinib’s central nervous system activity and breadth across classical and non-classical EGFR mutations, including resistance like C797S, can carve out a clinically meaningful lane.

BDTX Valuation Multiples Versus Peer Benchmarks

BDTX is trading at 3.32 times forward 12-month sales value per share. That compares with 2.08 times for the Zacks sub-industry, 2.36 times for the Zacks sector, and 5.13 times for the S&P 500.

History also frames expectations. Over the past five years, the stock has traded as high as 3.96 times and as low as 1.10 times, with a five-year median of 2.06 times. For investors, that range reinforces how quickly the multiple can move when the market recalibrates the probability of success around upcoming data.

Black Diamond Decision Framework Using Zacks Metrics

BDTX carries a Neutral Zacks Rank #3 (Hold). In practice, that lines up with a wait-for-evidence approach in a story where valuation is driven by clinical milestones and partnership execution rather than recurring product sales. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Staying on the sidelines is easier to justify when the next catalyst is a definitional one, such as progression-free survival and durability updates. Taking risk ahead of data becomes more defensible only if an investor is comfortable with single-asset concentration and believes the central nervous system signal and mutation coverage will continue to hold as follow-up matures.

Research Chief Names "Single Best Pick to Double"

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

This company targets millennial and Gen Z audiences, generating nearly $1 billion in revenue last quarter alone. A recent pullback makes now an ideal time to jump aboard. Of course, all our elite picks aren’t winners but this one could far surpass earlier Zacks’ Stocks Set to Double like Nano-X Imaging which shot up +129.6% in little more than 9 months.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

AstraZeneca PLC (AZN): Free Stock Analysis Report

Johnson & Johnson (JNJ): Free Stock Analysis Report

Black Diamond Therapeutics, Inc. (BDTX): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).