CrowdStrike (CRWD) is getting a very different message from Wall Street than it was a few months ago. The stock has moved lower from its highs, cybersecurity names have been volatile, and investors are still trying to decide whether AI is a tailwind or a threat for software vendors.

KeyBanc just came down squarely on the bullish side. It upgraded CrowdStrike to “Overweight” and set a $525 target, saying AI is a hope for cybersecurity, not a threat. That is the heart of the debate now. If AI expands the attack surface, then security spending should rise. If AI changes how companies buy software, then the old rules may not hold.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

Why CrowdStrike Still Matters

CrowdStrike is not just another software name. It is one of the best-known pure-play cybersecurity companies, built around its Falcon platform. The company sells a cloud-based security stack that helps customers protect endpoints, identities, cloud workloads, and data. That platform approach has made CrowdStrike a leader in a market where companies want fewer tools and more automation.

The company has stayed active this year. It launched new AI security tools, expanded product coverage, bought SGNL and Seraphic Security, and deepened partnerships with Microsoft (MSFT), VAST Data, and others. It also signed a memorandum with Aramco and won new recognition from Gartner (IT) peers. The strategy is simple. CrowdStrike wants to make Falcon broader, stickier, and harder to replace.

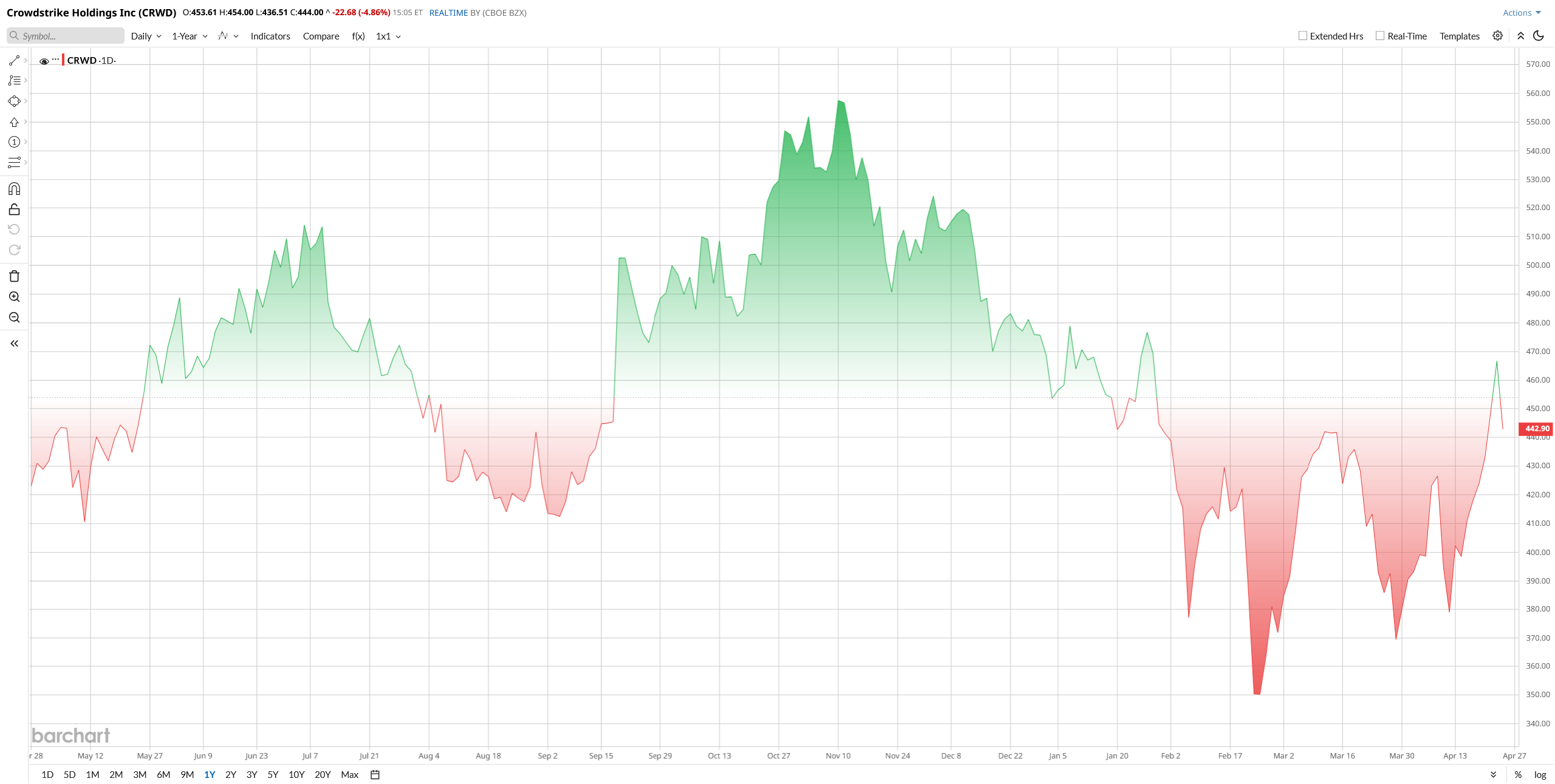

CRWD stock has had a messy 2026, even with a recent bounce. Shares have gained more than 15% over the past year, yet are trading down 5% year-to-date (YTD). The choppy movement reflects strong growth and record FY26 ARR, but valuation worries, slower six-month momentum, and post-outage caution have kept gains muted this year.

On paper, CRWD stock is not cheap. It trades at about 20.15 times enterprise value to revenue, which is below its 10-year median of 24.65 but still a premium multiple for any security stock. Its forward P/E is also extremely high, which tells you the market is still paying up for growth and cash flow. That is fine if the business keeps firing. It is risky if growth slows.

www.barchart.com

www.barchart.com Why KeyBanc’s Call Matters

This is where KeyBanc’s view gets interesting. The firm is basically saying the market may be misunderstanding what AI means for cybersecurity. More AI can mean more automation, but it can also mean more threats, more complexity, and more demand for protection.

KeyBanc sees that as a positive for CrowdStrike, not a negative. The stock moved higher after the note, but investors are still weighing that optimism against a broader software selloff and a valuation that is still demanding.

The Last Quarter Was Strong

CrowdStrike’s fiscal fourth quarter and full year 2026 were solid. Revenue in the quarter was $1.31 billion, up 23% from a year earlier. Subscription revenue was $1.24 billion, also up 23%. For the full year, revenue reached $4.81 billion. ARR climbed 24% to $5.25 billion, and net new ARR hit a record $330.7 million in the quarter. That tells you demand is still healthy.

Profitability was better, too. CrowdStrike posted net income of $38.7 million in the quarter, compared with a loss a year earlier. EPS came in at $1.12, up from $0.81. Free cash flow was $376.4 million in the quarter, and cash and cash equivalents reached $5.23 billion. That is the kind of balance sheet that gives management room to keep investing while still rewarding shareholders with strong cash generation.

CEO George Kurtz said the year would go down in the company’s history books as its best year yet, and he tied that strength directly to AI adoption. CFO Burt Podbere also said the company was in “rare air” after a record quarter and record cash flow. Those comments matter because they match the numbers. This was not a flashy quarter. It was a durable one.

Guidance also came in above expectations. For the fiscal first quarter of 2027, CrowdStrike guided revenue to $1.36 billion to $1.364 billion and adjusted EPS to $1.06 to $1.07. For fiscal 2027, it guided revenue to $5.87 billion to $5.93 billion and adjusted EPS to $4.78 to $4.90. Barchart’s earnings page shows the Street looking for full-year fiscal 2027 EPS of $1.01.

What Do Analysts Think of CRWD Stock?

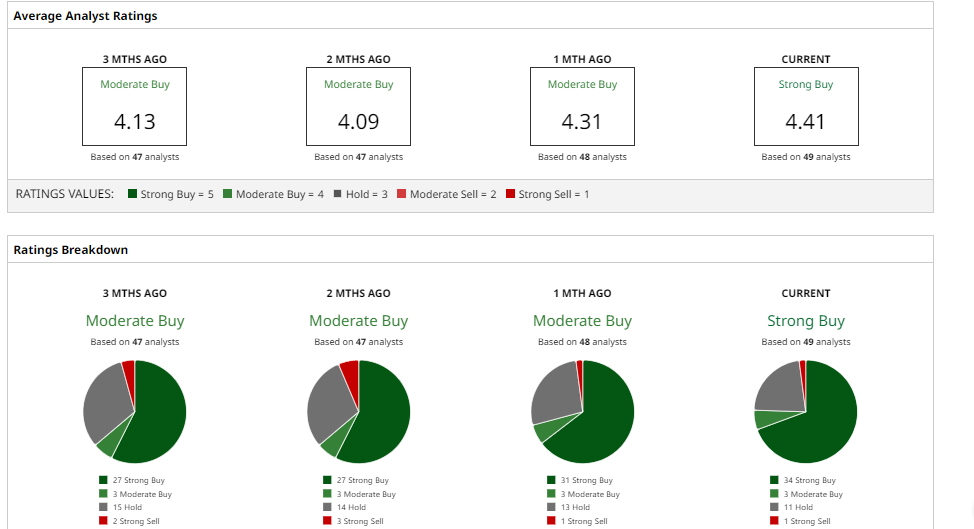

Wall Street still leans constructive on CRWD stock. Morgan Stanley recently moved to “Overweight” with a $510 target. Goldman Sachs kept a “Buy” rating and set a $500 target after cutting its earlier $564 view. BMO Capital Markets kept “Outperform” and put its target at $500. KeyBanc’s new $525 target sits right in that bullish camp.

Overall, Barchart shows a “Moderate Buy” consensus with 49 analysts and shows an average target near $492 with about 11% upside from the latest price.

KeyBanc’s view makes sense. AI may create more cyber risk before it creates less. That is good news for CrowdStrike, which is built to sell security in a world that keeps getting more complicated. The problem is not the business. The problem is the price. CRWD stock looks like a winner, but it still trades like one.

www.barchart.com

www.barchart.com On the date of publication, Nauman Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Tesla Beats in Q1—But TSLA Stock’s Bull Case Still Needs Fuel KeyBanc Sees AI Saving the Day for CrowdStrike Stock Despite Broad Wall Street Panic. Who’s Right? Amazon Aims to Take Over the GLP-1 Market Next. Will That Move the Needle for AMZN Stock? Should You Buy the Dip in ServiceNow Stock Today?