Intel (INTC) stock was up nearly 30% after reporting strong Q1 performance. It has gained 4x since the day Donald Trump met CEO Lip-Bu Tan in August last year. Before that meeting, the president had called for Lip-Bu Tan's resignation. After the meeting, he was all praise for the CEO’s amazing life story. What happened in between is anybody’s guess, but one thing was clear: Donald Trump wanted to revive the struggling giant, and whatever happened at the meeting finally seems to be bearing fruit.

Up until the end of the first quarter, nobody gave Intel a chance. After all, the stock still hadn’t reached the dot-com bubble highs, and it was difficult to back a giant that seemed to be dying a slow death. There are still question marks over Intel’s ability to execute to serve the increasing demand for CPUs and benefit from the supply crunch.

Join 200K+ Subscribers: Find out why the midday Barchart Brief newsletter is a must-read for thousands daily.

Intel’s 18A process node (equivalent to 1.8nm) is the most advanced process currently in development. Intel made it work but has faced issues ramping up. The Intel 3, the 7nm equivalent, was delayed due to issues with the preceding node. And the Intel 20A was the predecessor to 18A but was canceled for production as focus shifted to 18A. These issues have eroded investor interest, and even though the rise in stock price has given them some confidence, the underlying execution issues continue to bother many.

About Intel Stock

Founded in 1968, Intel Corporation is a semiconductor company specializing in computing and related end products and services. It operates in the DCAI, CCG, and Intel Foundry segments. The company serves original design manufacturers, original equipment manufacturers, cloud service providers, and other manufacturers and service providers. It delivers a range of products, including data center and AI products, client computing group products, and semiconductors comprising wafer fabrication, substrates, and other related products and services.

Intel has lately been in a league of its own when it comes to stock performance. After lagging or completely missing out on the semiconductor rallies since the emergence of AI, the company now outperforms all benchmarks over the last year. The often-hated stock is now the darling of Wall Street.

www.barchart.com

www.barchart.comThe Surprise on the Earnings Call

Intel reported its first quarter FY 2026 earnings on April 23. The company’s Q1 results were supported by inventory and pricing actions. Pricing and a better product mix also helped margins, with Non-GAAP gross margin reaching 41%. On the segment side, CCG revenue came in at $7.7 billion, down 6% sequentially. However, AI PC revenue grew 8% sequentially and now makes up more than 60% of the client CPU mix. DCAI revenue reached $5.1 billion, reflecting a 7% sequential increase and 22% year-over-year (YoY). Intel Foundry continued to weigh on overall performance.

For the second quarter, Intel Corporation expects revenue to range from $13.8 billion to $14.8 billion. At the midpoint of $14.3 billion, the company is guiding for a non-GAAP gross margin of 39%, a tax rate of 11%, and EPS of $0.20. Due to rising input costs and supply constraints, Intel expects weaker PC demand in the second half, with full-year units declining by low double-digit units. At the same time, the server outlook has improved. The company now expects double-digit unit growth for the industry and for Intel.

Considering the supply constraints amid extremely high CPU demand, investors are now clearly backing the company to deliver. The earnings call provided some insights that are partly driving the positive sentiment. Lip-Bu Tan acknowledged on the call that, at the end of the day, the best product wins. The company has made numerous changes to CPU architecture to make it suitable for modern workloads. What’s more, the company is also building a GPU line. This makes Intel a designer, advanced packaging expert, foundry, and GPU maker. This is the same advantage the company has previously squandered, but investors are willing to bet that this time, it’s different.

What Are Analysts Saying About INTC Stock?

Following its earnings report, TD Cowen analyst Joshua Buchalter raised the firm’s price target on INTC stock from $60 to $75. However, he kept his “Hold” rating on the stock. In addition to TD Cowen, Jefferies also raised its price target on the shares from $60 to $80 while maintaining a “Hold” rating. This positive analyst sentiment is further strengthening investor confidence in the stock.

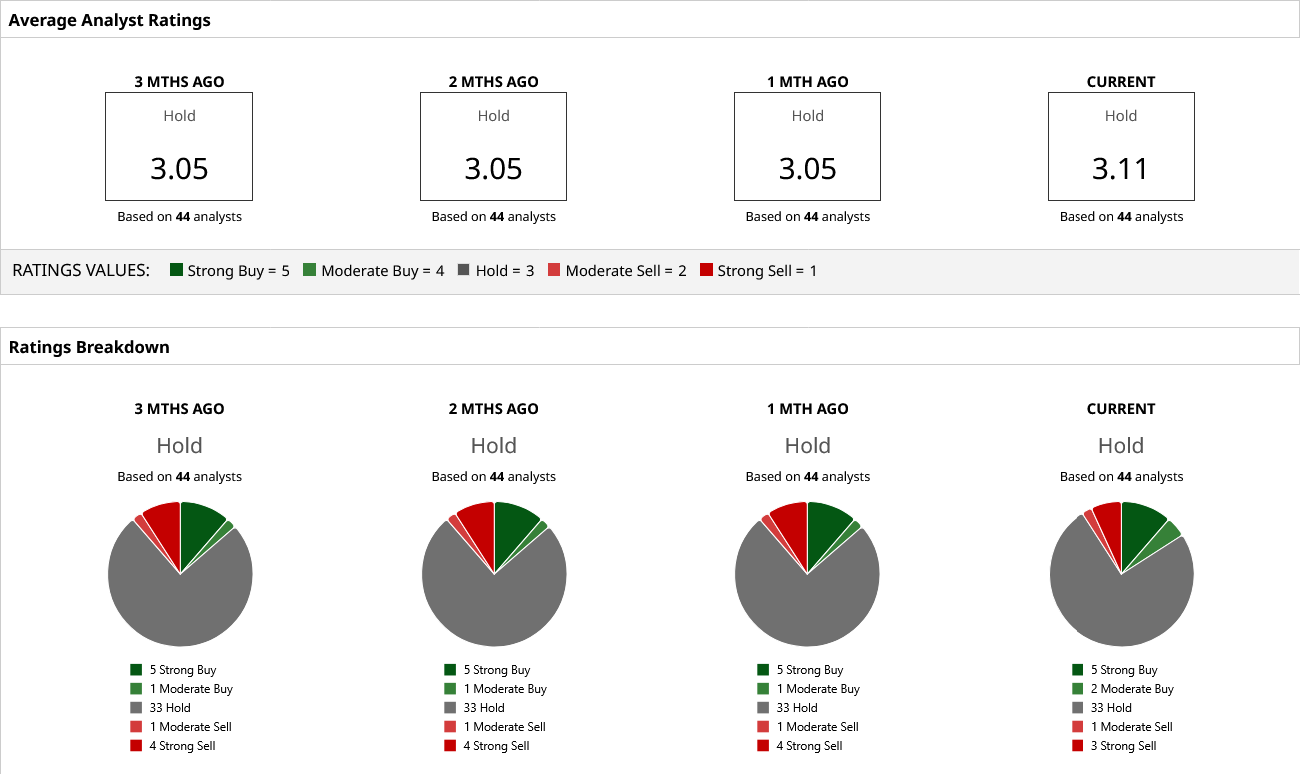

Intel is currently covered by 44 Wall Street analysts and carries a consensus “Hold” rating. The most bullish estimate suggests the stock could climb as high as $95, implying potential upside of 17%. In the coming days, most analysts will revise their models, and the mean target price is expected to go up.

www.barchart.com

www.barchart.com On the date of publication, Jabran Kundi did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Dan Ives: Tesla Is ‘Morphing into a Physical AI Stalwart’ So Don’t Sweat the CapEx and Just Buy TSLA Stock Intel Earnings Confirm CPU Demand Is Outpacing Supply, But Does the Company Really Have an Edge? Sell the News? You Can Now Bet Against Sandisk Stock Twice Over with This New ETF Roth Capital Analysts: What Matters Most for Tesla Stock Now Isn’t Tesla… It’s SpaceX