Electric vehicle-making behemoth Tesla (TSLA) recently reported its first-quarter results, grabbing eyeballs on Wall Street. One of the largest factors that affected how the results were perceived was the company’s rising capital expenditures. The company’s Q1 CapEx increased by 67% from the year-ago value to $2.49 billion. Furthermore, it expects its CapEx to reach $25 billion this year.

Tesla has been investing heavily to transform itself from an EV maker into a company pioneering physical AI (such as robotaxis and its Optimus robot). However, this might put its cash flow under pressure in the near term. Wedbush’s Dan Ives believes that the huge CapEx is necessary to achieve its goal of “morphing into a physical AI stalwart,” maintaining a bullish “Outperform” rating on the stock and a Street-high $600 price target.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

We look into the company at this juncture…

About Tesla Stock

Tesla, headquartered in Austin, Texas, is increasingly framing itself as an AI and robotics company rather than just an automaker. It is investing heavily, on the order of tens of billions of dollars, in in-house AI chips, data centers, and manufacturing infrastructure to support full self-driving software, robotaxi fleets, and humanoid robots, rather than just vehicle production.

At the heart of this transformation is the company’s “Terafab” semiconductor project, humanoid robots, autonomous robotaxis, and tight collaboration with SpaceX on custom chips and space‑based systems. Tesla currently has a massive market capitalization of $1.4 trillion.

While the stock is up 45% over the past 52 weeks, it is not seen as enough by the standards Tesla set for itself earlier. Tesla’s stock has been down this year, mainly because investors are worried about margin pressure, weak demand in some markets, and a high valuation that has priced in a lot of future optimism. Recent delivery numbers have also disappointed. This year, Tesla’s stock has been down 16.9%. It had last posted a 52-week high of $498.83 in December 2025, and is down 24.6% from that level.

www.barchart.com

www.barchart.com Tesla’s lofty valuation refuses to come down. On a forward-adjusted basis, its price-to-earnings (non-GAAP) ratio of 178.60 times is eons higher than the industry average of 15.72 times.

Tesla’s Notable Q1 Earnings

As already stated, Tesla showed a remarkable recovery in the first quarter after a top line downturn in the previous quarter. Tesla’s revenue increased 16% year-over-year (YOY) to $22.39 billion. However, this was lower than the $22.64 billion that Wall Street analysts had expected (as polled by LSEG). The company’s automotive revenues also grew by 16% to $16.23 billion.

Tesla produced 408,386 vehicles during the quarter (including 394,611 Model 3/Y production), up 16% YOY, while it delivered 358,023 units during the quarter, up 6% YOY. However, the delivery numbers missed analyst estimates, leading to investor concerns. On the other hand, the company’s active FSD subscriptions increased to 1.28 million.

Tesla’s operating margin increased by 214 basis points YOY to 4.2%, as the company recognized an increase in automotive one-time benefits related to warranty and tariffs. Its non-GAAP EPS grew 52% from the prior-year period to $0.41, which topped the $0.37 figure that Street analysts had expected.

Analysts believe Tesla can further improve its bottom line. For the current year, Tesla’s EPS (on a diluted basis) is expected to grow 24.8% YOY to $1.36, followed by a 39% increase to $1.89 for the next year.

Analysts Still Have Mixed Feelings About Tesla

In addition to the “Outperform” reiteration from Wedbush analysts, post the Q1 results, other analysts have reiterated their stances on Tesla. Analysts at Cantor Fitzgerald maintained an “Overweight” rating and a $510 price target on the stock.

On the other hand, RBC Capital analysts lowered Tesla’s price target from $480 to $475, while maintaining an “Outperform” rating. The firm cited higher CapEx and caution around humanoids as the primary drivers of the reduced price target.

Needham analysts reiterated a “Hold” rating on Tesla with no price target, noting that the company’s first-quarter margin outperformance might be temporary due to non-recurring gains.

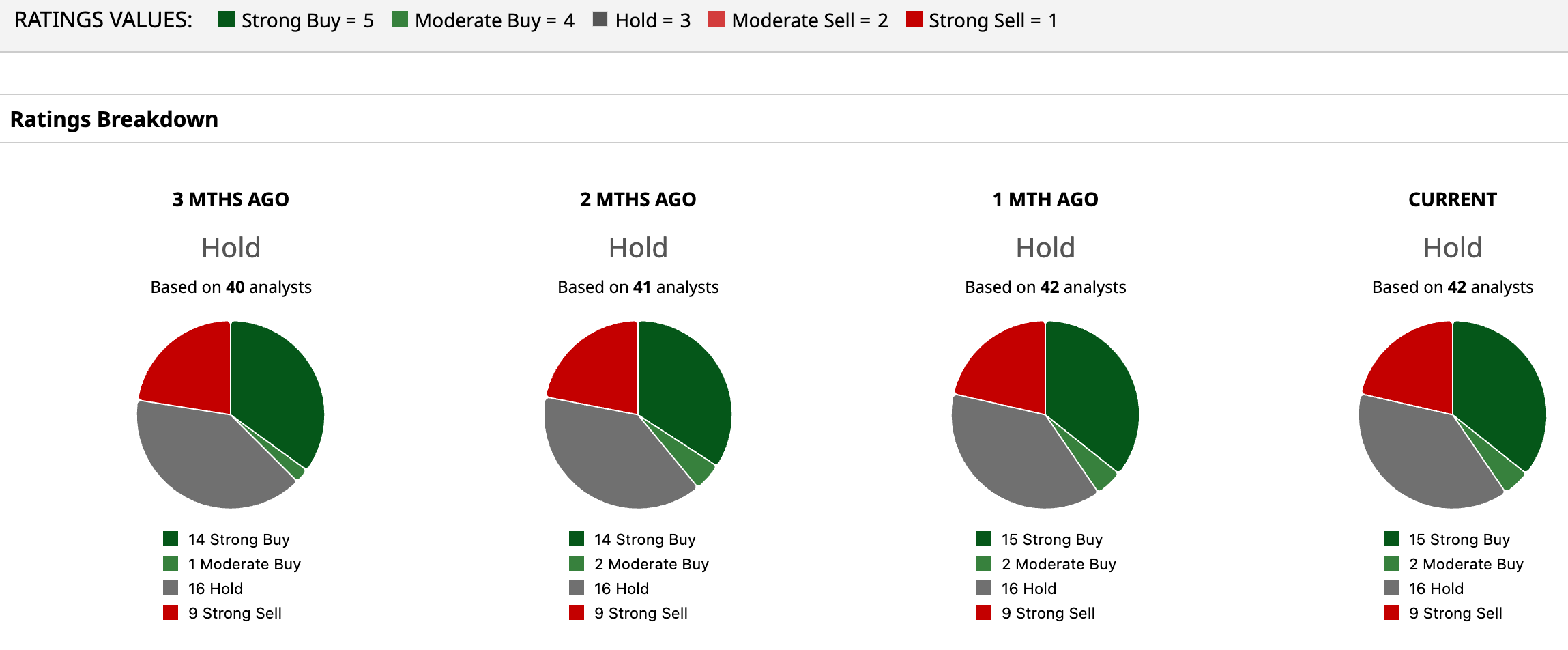

Wall Street analysts are taking a cautious stance on Tesla’s stock now, with a consensus “Hold” rating overall. Of the 42 analysts rating the stock, 15 analysts gave a “Strong Buy” rating, two analysts gave a “Moderate Buy” rating, while 16 analysts are playing it safe with a “Hold” rating, and nine analysts gave a “Strong Sell” rating. The consensus price target of $405.74 represents an 7.82% upside from current levels. Moreover, the Street-high Wedbush-given price target of $600 indicates a 59.5% upside from current levels.

www.barchart.com

www.barchart.com  www.barchart.com

www.barchart.com On the date of publication, Anushka Dutta did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Dan Ives: Tesla Is ‘Morphing into a Physical AI Stalwart’ So Don’t Sweat the CapEx and Just Buy TSLA Stock Intel Earnings Confirm CPU Demand Is Outpacing Supply, But Does the Company Really Have an Edge? Sell the News? You Can Now Bet Against Sandisk Stock Twice Over with This New ETF Roth Capital Analysts: What Matters Most for Tesla Stock Now Isn’t Tesla… It’s SpaceX