Enova International, Inc. ENVA is trying to reshape its model with the planned acquisition of Grasshopper. The logic is straightforward: pair Enova’s online lending engine with a digital-first bank platform and bring a national bank charter into the mix.

If approvals come through and integration goes as planned, the deal could lower funding costs, widen product reach, and lift earnings power.

The path is not linear, though, and near-term expense and credit trends still matter.

ENVA’s Grasshopper Plan Adds a National Bank Angle

Structurally, the transaction aims to combine Enova’s established online lending capabilities with Grasshopper’s digital-first banking infrastructure. That pairing is designed to create a tighter link between loan origination and a bank-based funding and deposit platform.

The national bank charter is the big unlock. It is expected to broaden access to both lending and deposit products, giving Enova more flexibility in how it funds loans and how it serves customers across the country.

Enova’s Funding Costs Could Improve With Deposits

A key trend implication is the potential reset in Enova’s funding stack. Grasshopper’s deposit base is estimated to be 300–400 basis points cheaper than Enova’s existing securitization funding, which could materially change unit economics.

Lower funding costs typically allow a lender to price more competitively while maintaining returns, or to hold pricing steady and expand margins. Either way, cheaper deposits can improve balance-sheet flexibility by reducing reliance on capital markets timing and securitization conditions.

ENVA’s Synergy Targets Are Material in Two Years

Management’s synergy targets are sizable relative to the scale of the move. The expectation is for revenue synergies of $175–$230 million within two years after close, with adjusted earnings per share accretion expected to exceed 15% in year one and rise beyond 25% as synergies mature.

Those figures create a clear “potential if executed” setup. The market will likely weigh these targets against integration complexity, the pace of deposit growth, and the time it takes to translate expanded product capacity into measurable originations and revenue.

ENVA’s Timeline and Approval Risk Are Part of the Story

The timeline is not fully in management’s control. The deal is subject to regulatory approvals, including the Office of the Comptroller of the Currency and the Federal Reserve, as well as Grasshopper shareholder approval.

Closing is anticipated in the second half of 2026. Until those milestones are cleared, the market may treat synergy targets and funding benefits as probabilistic rather than assured, especially given the centrality of the charter and deposit platform to the strategic case.

The deal also comes with an investment phase, and the early signs are already visible. Acquisition-related expenses showed up in the first quarter of 2026, including $2.7 million of pre-tax costs tied to the transaction.

Expense ratios also remain elevated, with marketing, operations, technology, and general and administrative expense guidance for the second quarter signaling continued intensity. The core question for investors is whether this spending ultimately converts into sustained deposit traction, product expansion, and measurable synergy capture.

Enova’s What-To-Watch List as the Deal Progresses

The first checkpoint is regulatory progress and the sequencing of required approvals. Clear milestones, timely filings, and transparent updates can reduce uncertainty around the closing window.

Next is evidence of funding mix improvement. Investors will want to see whether deposits begin to play a larger role and whether the implied 300–400 basis point cost advantage translates into reported funding costs and stronger lending economics.

Originations will be another key indicator, particularly as the product suite expands and the company tests broader reach across states and customer segments. Finally, watch whether expense intensity moderates as integration work stabilizes and whether early revenue synergies begin to show up in performance, validating the longer-term earnings accretion pathway.

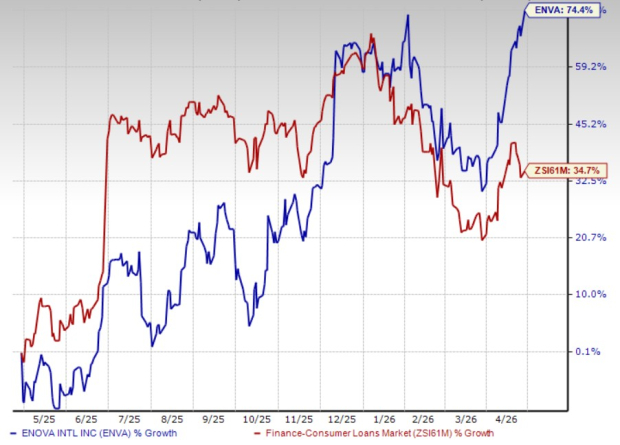

ENVA’s Zacks Rank and Price Performance

ENVA carries a Zacks Rank of 2 (Buy) at present. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Enova shares gained 74.4% in the past year compared with the industry’s rise of 34.7%.

Price Performance

Image Source: Zacks Investment Research

ENVA Peers Efforts to Expand Inorganically

Capital One’s COF opportunistic buyouts over the years have been driving its revenues. In January 2026, it announced a deal to acquire Brex for $5.15 billion, which is expected to be closed in the middle of 2026. In May 2025, COF acquired Discover Financial in an all-stock transaction valued at $35.3 billion, reshaping the landscape of the credit card industry, creating a behemoth and unlocking substantial value for shareholders (the deal is expected to be more than 15% accretive to adjusted EPS by 2027).

Sallie Mae SLM has made efforts to expand its business operations on the back of investments in varied product offerings and inorganic activities. In 2023, the company acquired several vital assets, technology, intellectual property, and the experienced staff of Scholly, a scholarship publishing and servicing platform. In 2022, Sallie Mae closed the deal with Epic Research LLC to acquire a digital marketing and education solutions company, Nitro College. Such inorganic moves are likely to aid SLM in becoming a holistic education solutions provider for students and drive loan originations for the company.

Research Chief Names "Single Best Pick to Double"

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

This company targets millennial and Gen Z audiences, generating nearly $1 billion in revenue last quarter alone. A recent pullback makes now an ideal time to jump aboard. Of course, all our elite picks aren’t winners but this one could far surpass earlier Zacks’ Stocks Set to Double like Nano-X Imaging which shot up +129.6% in little more than 9 months.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

SLM Corporation (SLM): Free Stock Analysis Report

Capital One Financial Corporation (COF): Free Stock Analysis Report

Enova International, Inc. (ENVA): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).