Super Micro Computer (SMCI) has become one of the most controversial AI plays of 2026. Recently, Oracle (ORCL) canceled a major AI server contract worth roughly $1.1 billion to $1.4 billion with SMCI, involving hundreds of high-end AI racks, causing SMCI shares to drop more than 10% and raising concerns about the company's growth prospects.

Despite the setback with Oracle, SMCI stock quickly rebounded as the broader AI demand remains strong. So far this year, SMCI stock is down 6.3%, underperforming the Nasdaq Composite Index ($NASX) gain of 6%. Here are two red flags and one green flag to consider if you are planning to add SMCI to your portfolio.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

www.barchart.com

www.barchart.com Red Flag #1: Customer Concentration Risk Is Extremely High

Valued at a market cap of $16.7 billion, Super Micro Computer designs and manufactures high-performance servers, storage systems, and complete data center solutions. These are mostly used to run AI workloads, cloud computing, and enterprise infrastructure. Between 2021 and 2025, SMCI’s annual revenue has increased dramatically from just $3.5 billion to $21 billion.

While revenue growth is impressive, one of the most overlooked issues is customer concentration. The company is heavily reliant on a handful of buyers. What’s worse is that in the second quarter of fiscal 2026, one large data center customer accounted for approximately 63% of total revenue, which is dangerously concentrated. When a business relies this heavily on one customer, losing or declining orders can instantly hit revenue, shifting pricing power to the customer, and making future revenue vulnerable. The Oracle contract loss further exposes the company’s heavy dependency on a few large hyperscale clients.

This risk becomes even more concerning when you look at how the company’s overall business is evolving. For context, its OEM appliance and large data center segment generated $10.7 billion in revenue, representing 84% of total revenue, up sharply from 68% in the previous quarter. Meanwhile, the enterprise segment contributed $2 billion, or 16% of revenue, a drop from 31% in the prior quarter. This distinction indicates that SMCI is becoming more reliant on hyperscale customers, who often have greater pricing power and less loyalty.

Additionally, geographic concentration adds another layer of risk. The U.S. alone accounted for 86% of total revenue. This means SMCI is not only reliant on a few customers but also heavily tied to a single region. In a cyclical industry like data center infrastructure, that lack of diversification can amplify volatility during downturns.

Red Flag #2: Balance Sheet Pressure is Quietly Building

SMCI’s balance sheet gives investors another reason to be cautious. The company ended Q2 with $4.1 billion in cash but also held $4.9 billion in total debt. Its net debt position now stands at $787 million, up from $579 million in the prior quarter. To add to the worries, the company has secured a $2 billion U.S. revolving credit facility and an additional $1.8 billion secured Taiwan debt facility to support its rapid expansion. This shows that SMCI’s growth is increasingly funded through debt, which is not a sign of balance sheet strength.

The debt wouldn’t still be a concern if the company was generating enough free cash flow (FCF) to pay it off. In fact, FCF stood negative in the quarter, totaling $45 million, suggesting that working capital demands are consuming cash. A major cause of this is inventory buildup, which surged to $10.6 billion from $5.7 billion in the previous quarter. While management assured that this inventory will support strong future demand, a large inventory position also poses a risk if demand slows.

Green Flag: AI Demand Is Still Exploding

Despite these concerns, the company continues to benefit from the exploding AI demand. In Q2, revenue of $12.7 billion increased by 123% year-over-year (YoY) and 153% sequentially, driven by rapid deployment of rack-scale AI solutions. Notably, AI GPU platforms accounted for over 90% of total revenue. The Oracle contract loss removed a significant chunk of expected revenue. Nevertheless, the company’s backlog remains strong due to order strength across global large data center and enterprise customers. This gives the company confidence in its near-term revenue, which is expected to be $12.3 billion in the third quarter and at least $40 billion for the full fiscal year 2026.

Additionally, SMCI is expanding its product ecosystem through Data Center Building Block Solutions (DCBBS), which already contributed 4% of profit in the first half of 2026 and is expected to at least double by the end of the year. These initiatives position SMCI to continue playing a vital role in the global AI infrastructure buildout.

What Does Wall Street Say About SMCI Stock?

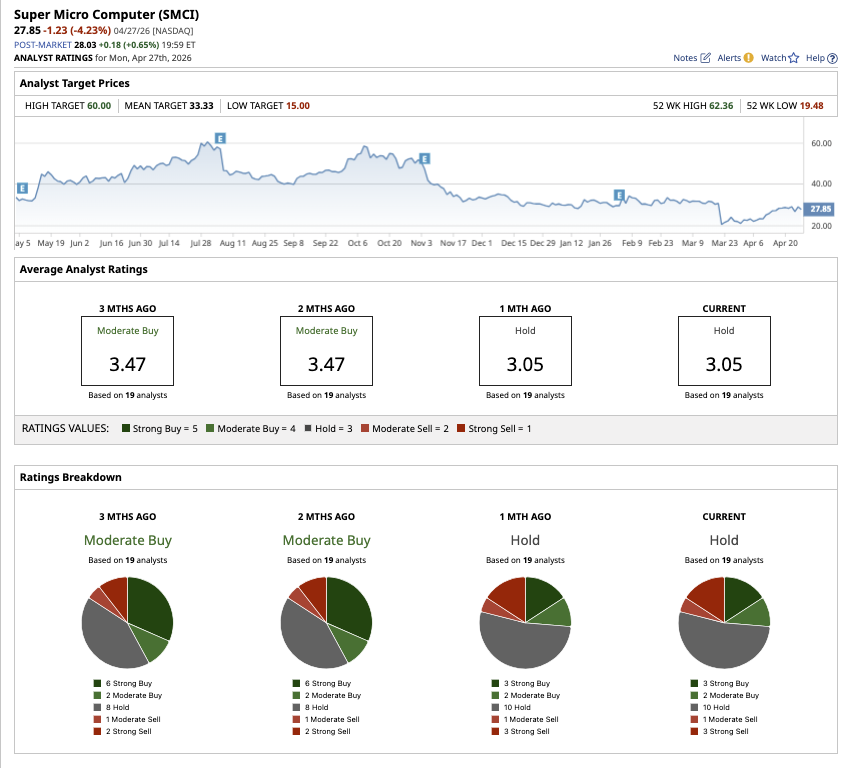

Nonetheless, Wall Street remains cautiously optimistic about SMCI stock. Of the 19 analysts who cover the stock, three rate it a “Strong Buy,” two say it is a “Moderate Buy,” 10 rate it a “Hold,” one says it is a “Moderate Sell,” and three say it is a “Strong Sell.” The stock’s average price target of $33.33 indicates a 20% increase from current levels. Meanwhile, the Street-high estimate of $60 suggests a potential 115% jump over the next 12 months.

www.barchart.com

www.barchart.com On the date of publication, Sushree Mohanty did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

SMCI Stock Alert: 2 Red Flags and 1 Green Flag About Supermicro Where is the Most Diversified U.S. Stock Market Index Heading? Memory Supply Dynamics May Hurt Qualcomm’s Q2. Is QCOM Stock a Buy, Sell, or Hold? As OpenAI Drags Down Chip Stocks, Is Applied Materials Stock a Buy, Sell, or Hold?