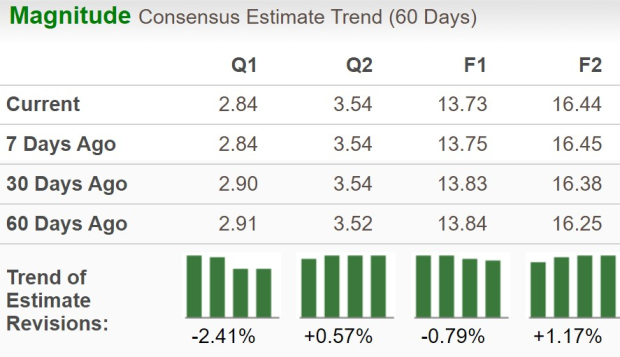

Global Payments Inc. GPN is set to report first-quarter 2026 results on May 6, 2026, before the opening bell. The Zacks Consensus Estimate for the to-be-reported quarter’s earnings is currently pegged at $2.84 per share on revenues of $2.83 billion.

The first-quarter earnings estimate witnessed no upward revision over the past 60 days against six downward movements. The bottom-line projection indicates a year-over-year increase of 0.7%. The Zacks Consensus Estimate for quarterly revenues implies year-over-year growth of 28.2%.

For full-year 2026, the Zacks Consensus Estimate for Global Payments’ revenues is pegged at $12.42 billion, implying a rise of 33.3% year over year. The consensus mark for the current year EPS is pegged at $13.73, implying a jump of 12.4% on a year-over-year basis.

Global Payments’ earnings beat the consensus estimate in three of the last four quarters and met once, with an average surprise of 2%. This is depicted in the figure below.

Global Payments Inc. Price and EPS Surprise

Global Payments Inc. price-eps-surprise | Global Payments Inc. Quote

Q1 Earnings Whispers for GPN

Our proven model does not conclusively predict an earnings beat for the company this time around. The combination of a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), 2 (Buy), or 3 (Hold) increases the odds of an earnings beat, but that is not the case here.

GPN has an Earnings ESP of -2.90% and a Zacks Rank #3. You can uncover the best stocks to buy or sell before they’re reported with our Earnings ESP Filter.

You can see the complete list of today’s Zacks #1 Rank stocks here.

What’s Likely to Shape GPN’s Q1 Results?

GPN’s first quarter results are expected to reflect the impact of the acquisition of Worldpay and the sale of Issuer Solutions Business. The transaction closed on Jan. 12, 2026. The Zacks Consensus Estimate for revenues from Europe operations is pegged at $526.2 million, which indicates a 101.5% year-over-year growth on a comparable basis. Similarly, the consensus mark for revenues from the Americas operations is pegged at $2.5 billion, signaling around 71% jump from a year ago.

The consensus estimate for revenuesfromAsia Pacific stands at $100.8 million, indicating 56.4% year-over-year growth. The above-mentioned estimates indicate that GPN is positioned for year-over-year growth. However, profit growth from the businesses is likely to have been partially offset by increased costs under certain heads.

For the to-be-reported quarter, we anticipate the adjusted cost of service to rise 40.5% year over year. We expect adjusted total operating costs to be around $1.7 billion in the quarter, a 34.4% increase from the year-ago level. We expect the Adjusted EBITDA margin to decline to 44.8% in the first quarter, from 47.9% a year ago.

How Are GPN’s Peers Placed This Quarter?

American Express Company AXP already reported first-quarter 2026 EPS of $4.28, which surpassed the Zacks Consensus Estimate by 6.2% and advanced 18% year over year. Total revenues, net of interest expense, improved 11% year over year to $18.9 billion. The quarterly results were driven by increased Card Member spending, higher net interest income and improved card fee growth. However, the upside was partly offset by AXP’s elevated operating expenses.

Visa Inc. V delivered second-quarter fiscal 2026 adjusted earnings of $3.31 per share, up 20% year over year and ahead of the Zacks Consensus Estimate by 7.1%. Its quarterly results benefited from resilient spending trends, higher cross-border volumes andsolid network activity, including a 9% year-over-year increase in payments volume on a constant-dollar basis.However, the upside was partly offset by Visa’s increased operating expenses.

Mastercard Incorporated MA is scheduled to report first-quarter 2026 results on April 30. The Zacks Consensus Estimate for adjusted earnings is pegged at $4.40 per share, indicating 18% year-over-year growth. The same for revenues is pegged at $8.29 billion, signaling a 14.4% increase. Mastercard beat earnings estimates in each of the past four quarters with an average surprise of 5.5%.

7 Best Stocks for the Next 30 Days

Just released: Experts distill 7 elite stocks from the current list of 220 Zacks Rank #1 Strong Buys. They deem these tickers "Most Likely for Early Price Pops."

Since 1988, the full list has beaten the market more than 2X over with an average gain of +23.9% per year. So be sure to give these hand picked 7 your immediate attention.

See them now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Mastercard Incorporated (MA): Free Stock Analysis Report

Visa Inc. (V): Free Stock Analysis Report

American Express Company (AXP): Free Stock Analysis Report

Global Payments Inc. (GPN): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).