Microsoft’s partnership with OpenAI just took a big turn. On April 28, Microsoft (MSFT) said it will no longer pay a revenue share to OpenAI. At the same time, Microsoft’s license to OpenAI’s technology is no longer exclusive through 2032, which means OpenAI can now work more freely with other cloud companies, including Amazon (AMZN) and Alphabet's Google (GOOGL).

The timing is not great. MSFT stock was already under pressure going into 2026. The shares had already taken a 10% one-day drop after fiscal Q2 2026 earnings, even though revenue rose 17% year-over-year (YOY). This latest change came just one day before Microsoft’s fiscal Q3 earnings release today on April 29, which gave investors even more to think about at a sensitive time.

More Yield, Less Trap: Sign up free to get Barchart’s daily Dividend Investor newsletter straight to your inbox.

Still, not everyone on Wall Street sees this as a bad move. Wedbush analyst Dan Ives said the new setup could actually help Microsoft. His view is that the deal gives Microsoft years of access to OpenAI’s technology, clears up some of the friction between the two companies, and lets Microsoft keep more of the revenue tied to Azure.

So is Microsoft losing something important here, or is this change actually giving it more room to win? Let’s find out.

The Numbers Still Tell Microsoft’s Story

Microsoft makes its money in a few simple ways. Cloud services through Azure, software like Office and Dynamics, security tools, and consumer products such as Windows, Xbox, and devices, with subscriptions and cloud now doing much of the heavy lifting. Over the past 12 months, MSFT is still up 7.21%, even though it’s down 12.65% so far this year.

www.barchart.com

www.barchart.comThe stock trades at 25.69 times forward earnings versus 23.21 times for the sector, so investors are still paying a premium for Microsoft. Income investors get a steady stream of cash, too. The company pays a quarterly dividend of $0.91 per share, with a forward payout ratio of 22.01%, a 0.86% annual yield, and 24 straight years of dividend hikes, compared with a 1.37% average yield for tech.

The latest quarter was strong. Revenue came in at $81.27 billion versus $80.32 billion expected, operating profit was $38.28 billion versus $36.62 billion, and GAAP EPS hit $5.16 versus $3.85, while non-GAAP EPS was $4.14 excluding the OpenAI impact. Intelligent Cloud revenue was about $32.9 billion and beat estimates, with Azure growing 38% YOY. Business software revenue reached $34.12 billion versus $33.46 billion expected, while personal computing was weaker at $14.25 billion versus $15.77 billion.

Even so, gross margin held at 68% and operating margin improved to 47.1% from 45.5%, though free cash flow margin slipped from 9.3% to 7.2%, showing solid performance overall with a few soft spots.

Why the Core Business Remains Intact

Microsoft’s deeper work with CrowdStrike (CRWD) is a good reminder that its main business is not tied to one AI partner. Customers can now buy the CrowdStrike Falcon platform straight from Microsoft’s marketplace using their existing Azure commitment, which helps them get protected faster, use more of the cloud spend they already signed up for, and keep billing and paperwork in one place. It also keeps Azure at the center of the deal, even when the security product itself comes from a third party.

The long-term deal with the Mercedes‑AMG PETRONAS F1 Team tells a similar story. Mercedes is putting Microsoft’s cloud and analytics tools at the heart of how it designs, tests, and runs cars ahead of the big 2026 rule changes, from the factory all the way to race day. When a top F1 team is willing to lean on your stack for speed and reliability, it says a lot about how sticky that technology is inside big organizations.

Then there is the work with North America's Building Trades Union and TradesFutures, which is about training real workers rather than just talking about AI. Microsoft is rolling out free AI literacy courses and recognized credentials across apprenticeship readiness programs in 34 states, using union training centers and LinkedIn Learning to reach people on the ground.

Wall Street’s Case for Looking Past the Noise

For the current quarter ending March 2026 (results due after market close today, April 29, 2026), analysts expect earnings of $4.07 per share, up from $3.46 a year ago, which works out to 17.63% growth. For the June 2026 quarter, the Street is looking for EPS of $4.15 versus $3.65 last year, or 13.70% growth. Full-year estimates sit at $16.54 for fiscal 2026, up from $13.64 (21.26% growth), and $18.80 for fiscal 2027 versus $16.54, which implies another 13.66% increase.

Goldman is on board with that trajectory, keeping its “Buy” rating and a $600 price target, and backing management’s choice to focus on long-term AI scale, Copilot adoption, and in-house compute rather than pushing every short-term dollar out of Azure.

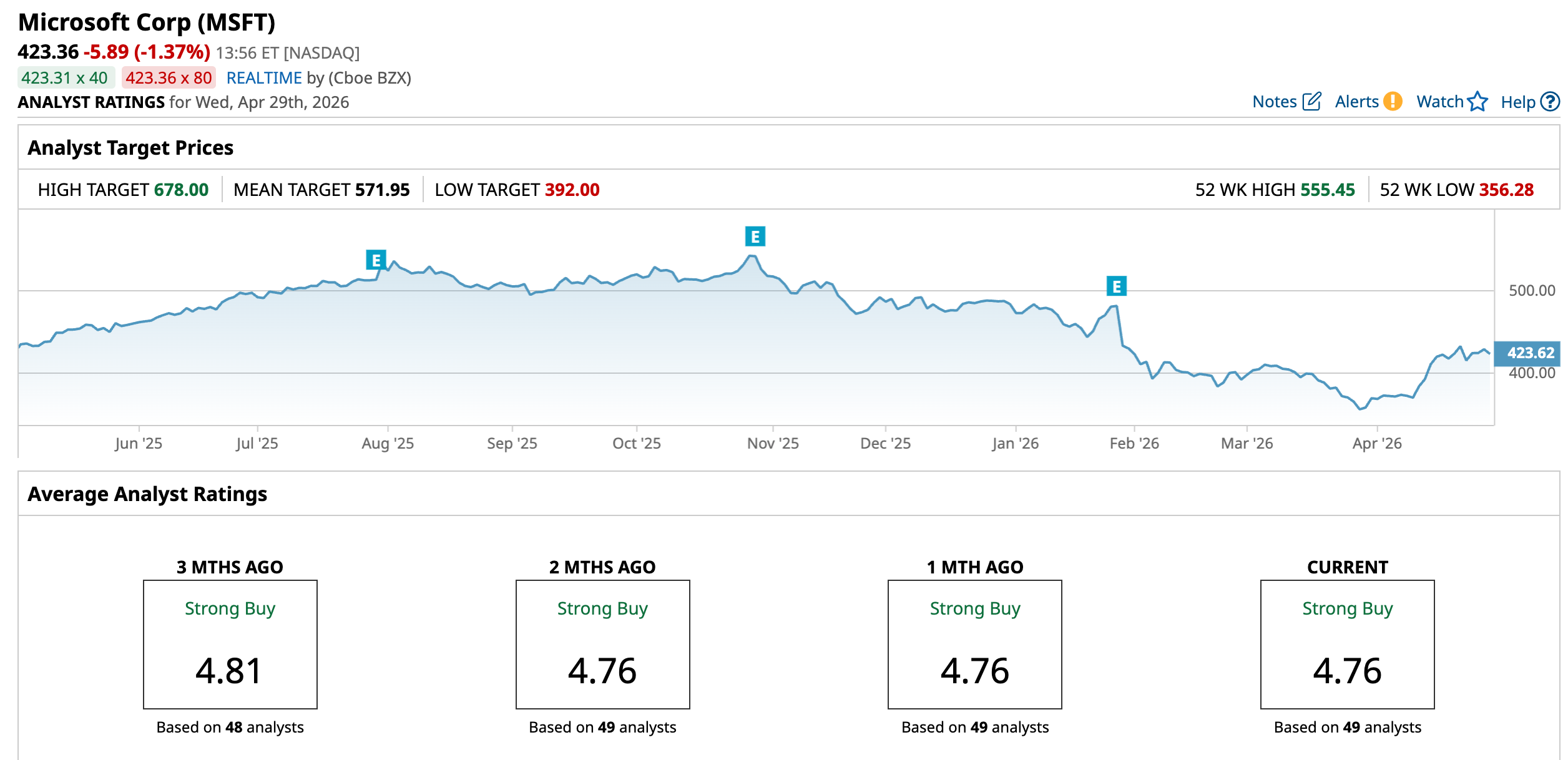

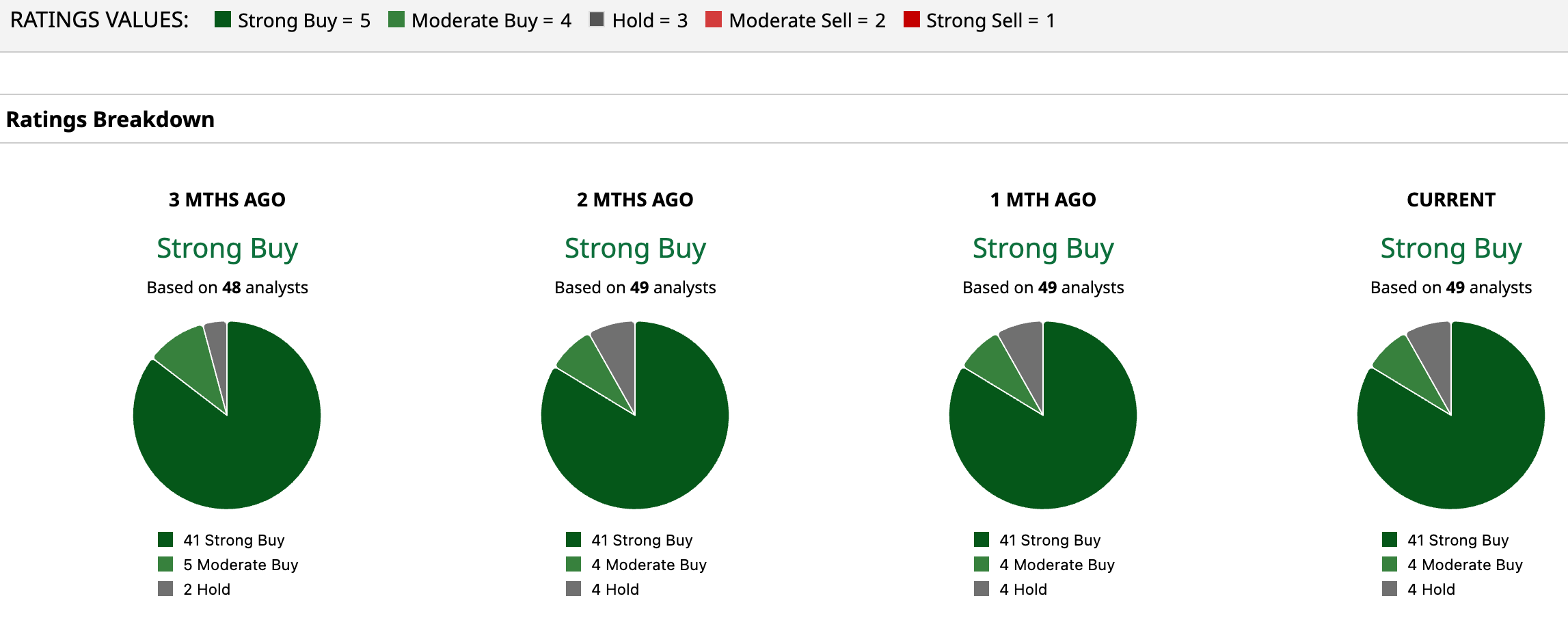

On top of that, all 49 analysts surveyed rate MSFT a consensus “Strong Buy,” and the average target of $571.95 suggests a 35.1% upside from where the stock trades today.

www.barchart.com

www.barchart.com www.barchart.com

www.barchart.comConclusion

The short answer is that losing exclusivity does not look like a thesis-breaker for Microsoft, at least not yet. The company still has the scale, earnings power, cloud footprint, and enterprise reach to keep monetizing AI even under a looser OpenAI arrangement, and Wall Street clearly thinks the market may be overplaying the negatives. From here, I think the most likely direction is that MSFT shares remain volatile in the near term as investors digest the new deal and earnings, but the bias probably stays higher over time if Azure growth and AI monetization continue to hold up.

On the date of publication, Ebube Jones did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Micron Stock Just Got a New Street-High Price Target. Should You Buy Shares Now? Seagate Stock Surges After Q3 Earnings — Why the Rally May Continue Microsoft and OpenAI Just Ended Their Exclusive Deal, and Wall Street Is Trying Hard to Shake Off the Negatives for MSFT Stock Strong Earnings and an Inflated Buffett Indicator Are Sending Opposite Signals for the Market, and for These 2 Consumer Stocks