Leading marketing platform company AppLovin Corporation (APP) is back in Wall Street's crosshairs, and the artificial intelligence (AI) powered mobile advertising platform just made it official by confirming its Q1 fiscal year 2026 earnings report drops on Wednesday, May 6 after markets close.

The report carries more baggage than most. AppLovin beat expectations in its last outing yet watched its stock absorb punishment from three directions at once. Those include an active U.S. Securities and Exchange Commission (SEC) investigation into its AI data collection practices, a relentless barrage of short seller attacks alleging fraud, and over $169 million in recent insider selling piling on at the worst possible moment.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

AppLovin has refused to take the heat lying down though. The company spent the months leading up to this print sharpening its AXON advertising engine, going deeper into AI led optimization and automation while deliberately stepping back from less strategic segments to lean harder into higher margin scalable software driven operations.

The pivot signals a deliberate push to streamline execution, tighten efficiency, and plant its flag as a technology first platform rather than a hybrid operator straddling two worlds. Investors heading into May 6 will look well past the headline numbers. They will treat sustainability, margins, and competitive positioning as the real scorecards that tell them where APP stock goes next.

About AppLovin Stock

Headquartered in Palo Alto, California, AppLovin is an AI advertising platform that helps businesses grow their apps and monetize content, serving everyone from indie developers to large enterprises.

The company sits on a market cap of roughly $150.5 billion, backed by a toolkit that covers the full advertising stack. Axon handles mobile ad targeting, MAX runs real-time auction bidding, Adjust crunches campaign analytics, and Wurl plants the flag in connected TV advertising.

The stock has had a wild ride worth tracking. AppLovin’s shares climbed 63.39% over the past 52 weeks before running into turbulence this year and sliding 32.23% year-to-date (YTD). The bulls are fighting back though, pushing the stock up 17.75% in just the past month alone.

www.barchart.com

www.barchart.com From a valuation standpoint, APP stock is currently trading at 28.21 times forward adjusted earnings. The valuation still trades at a discount relative to the company's own five-year historical average, indicating a wise entry point in the stock for long term investors.

AppLovin Surpasses Q4 Earnings

AppLovin dropped its Q4 fiscal year 2025 results on Feb. 11, and the company delivered what management called the most exceptional year ever and one of the strongest performances the public markets had seen in recent memory.

Revenue climbed 65.9% year-over-year (YOY) to $1.66 billion, fueled by continued technology advancements in its core mobile gaming business, seasonal tailwinds, and the expanding footprint of its e-commerce initiative. The figure also cleared analyst estimates of $1.62 billion with room to spare.

Net income jumped 84% from the year ago value to $1.1 billion, adjusted EBITDA landed at $1.4 billion representing an 81.7% margin, and EPS marched 87.3% higher to $3.24, comfortably beating the $3.11 Street’s forecast.

The balance sheet told an equally impressive story. Cash and cash equivalents ballooned to $2.5 billion as of Dec. 31, 2025, up sharply from $697 million a year earlier, while free cash flow rose 88.3% from the year ago value to $1.3 billion.

AppLovin put that strength to work for shareholders, repurchasing and withholding roughly 800,000 shares for $482 million during the quarter.

Looking forward to Q1 fiscal year 2026, the management expects revenue in the range of $1.745 billion to $1.775 billion. Adjusted EBITDA is projected between $1.465 billion and $1.495 billion, implying an adjusted EBITDA margin of approximately 84%.

On the other hand, analysts pencil in Q1 fiscal year 2026 EPS at $3.40 reflecting 103.6% YOY growth, full year fiscal 2026 earnings rising 56.6% to $15.72, and fiscal 2027 delivering another 32.6% surge to $20.84.

What Do Analysts Expect for AppLovin Stock?

Oppenheimer analyst Martin Yang is staying in AppLovin's corner with an “Outperform” rating but trimmed his price target from $740 down to $660, recalibrating after a fresh look at the company's financial outlook and the broader market environment.

Jefferies is keeping its “Buy” rating intact while pulling its price target back from $860 to $700, following AppLovin's fourth quarter financial results. Whereas Needham analyst Bernie McTernan held his ground entirely, reiterating a “Buy” rating and keeping his price target locked at $700, doubling down on confidence that APP stock still has a meaningful growth runway ahead.

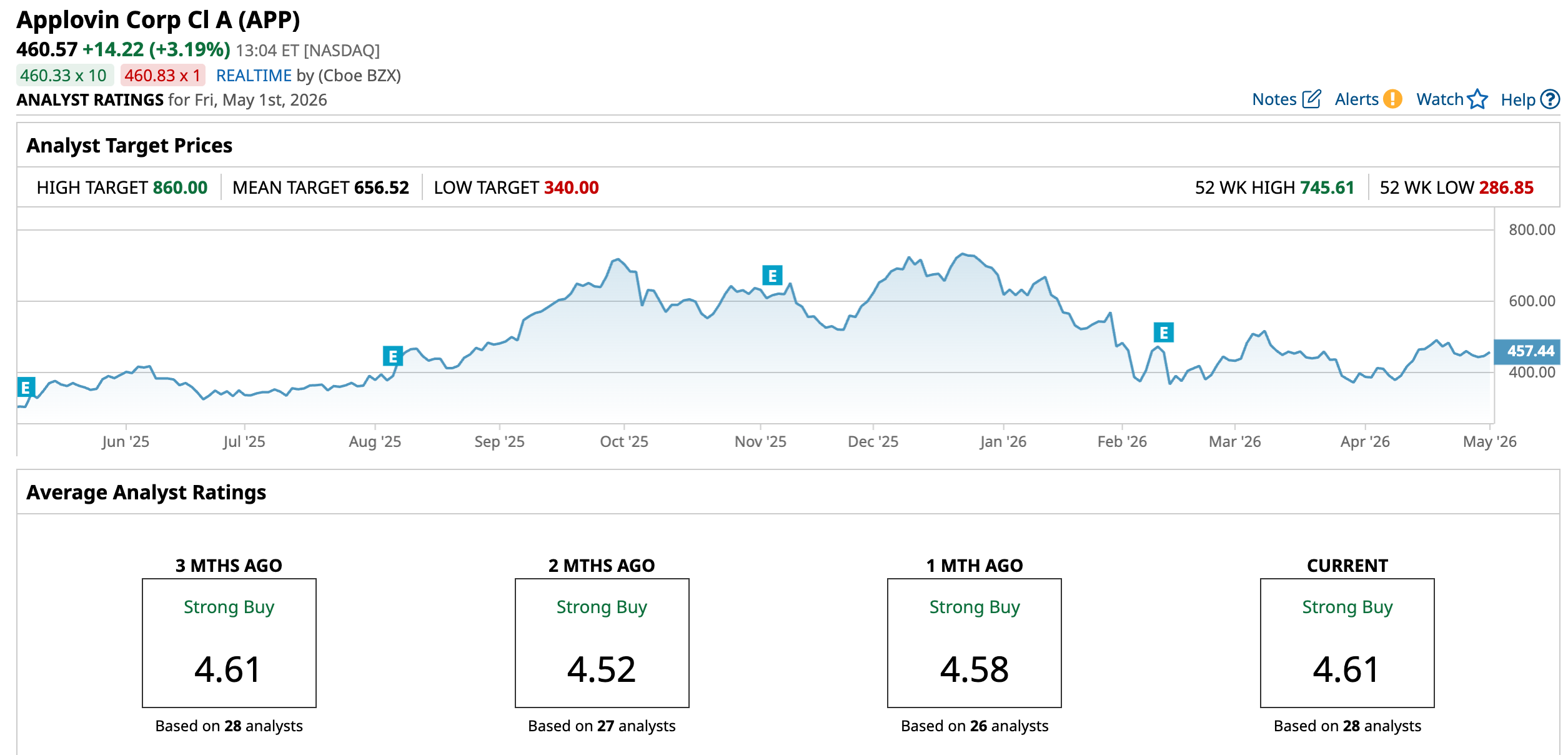

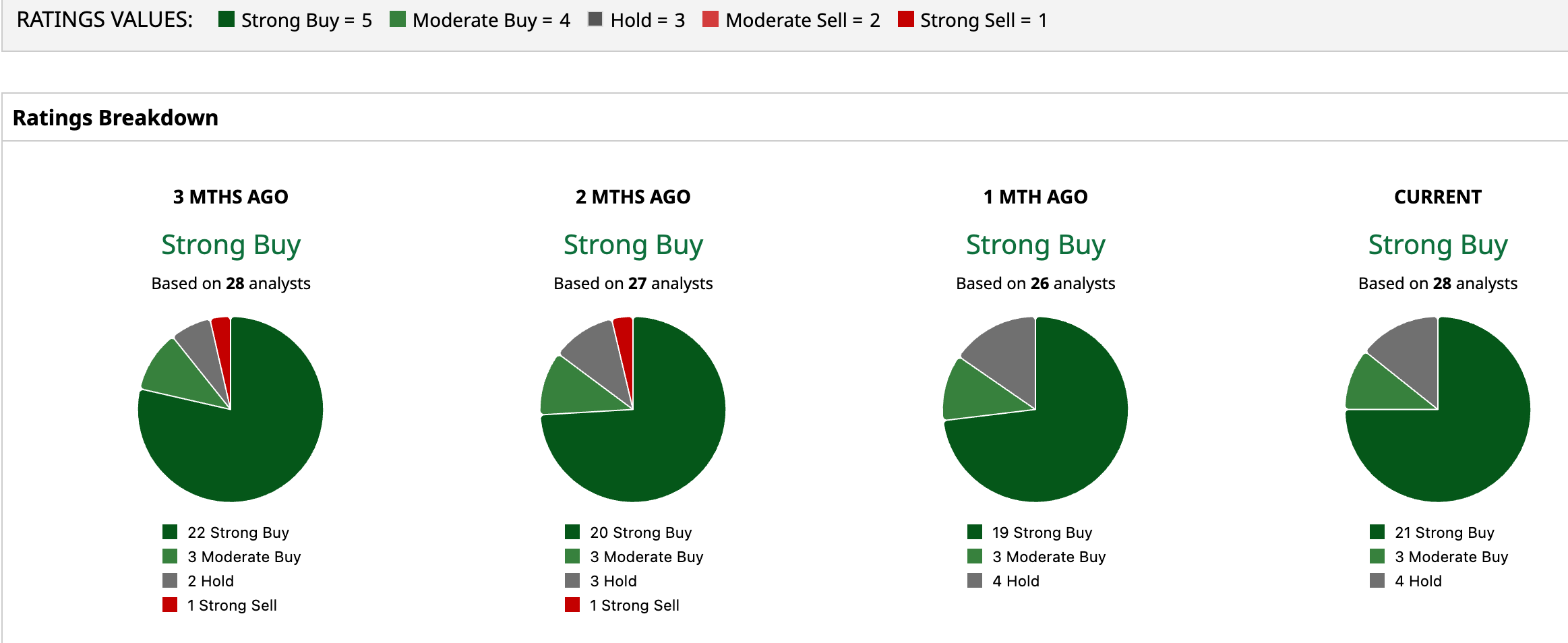

APP stock carries an overall rating of "Strong Buy" from Wall Street. Among 28 analysts covering the stock, 21 have assigned it a "Strong Buy" rating, three settled on "Moderate Buy," and four went with a "Hold" call.

The stock’s average price target of $656.52 represents potential upside of 42.6%. Meanwhile, the Street-High target of $860 still leaves 86.7% of upside on the table from current levels.

www.barchart.com

www.barchart.com  www.barchart.com

www.barchart.com On the date of publication, Aanchal Sugandh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Dear AppLovin Stock Fans, Mark Your Calendars for May 6 Apple Stock Reports Strong Free Cash Flow and FCF Margins - AAPL Looks 23% Too Cheap A Short Squeeze Could Trigger in EZCORP Stock as It Trades at New 10-Year Highs SoFi Stock Is Down 50%. Should You Buy Now, Cut Your Losses, or Stay Put?