Chewy, Inc. CHWY is increasingly leveraging private label expansion as a key driver of margin enhancement and product mix optimization. Through initiatives like “Chewy Made,” the company is building a unified owned-brand platform aimed at delivering high-quality products while improving profitability. This strategy complements Chewy’s broader margin trajectory, with the gross margin reaching 29.4% in fourth-quarter fiscal 2025, reflecting a 90 basis-point year-over-year expansion.

A major growth lever within private labels lies in the consumables category, particularly pet food and nutrition. Management highlighted that consumables represent $50-$60 billion of the broader $90-billion pet food and supplies market, underscoring a significant opportunity. By expanding its presence in this high-frequency category, Chewy is driving stronger customer engagement and increasing spending levels, as reflected in NSPAC of $591 in the fourth quarter of 2025, up 4% year over year.

Private label penetration currently remains at the low to mid-single-digit range of net sales, but the company is targeting a long-term range in the low-to-mid teens. At scale, these products are expected to deliver 500 basis points higher gross margin than the base business, making them a meaningful contributor to the overall margin expansion and earnings growth.

Chewy’s approach also includes a balanced assortment strategy, offering both premium and value-oriented products. This allows the company to expand its addressable customer base while maintaining pricing discipline and leveraging its e-commerce scale to manage costs efficiently. The combination of accessibility and premiumization strengthens customer acquisition and retention.

Looking ahead, private label growth is expected to remain a core pillar of Chewy’s profitability framework. Management projects an adjusted EBITDA margin of 6.6-6.8% in 2026, implying around 100 basis points of year-over-year expansion, supported in part by mix improvement. With increasing penetration and favorable unit economics, private labels position Chewy for sustained margin and earnings upside.

CENT & BARK’s Margin Picture vs. CHWY

Central Garden & Pet Company CENT delivered a solid gross margin performance in the first quarter of fiscal 2026, highlighting improved operational efficiency. Central Garden & Pet reported an adjusted gross margin expansion of 100 basis points to 30.8%, driven primarily by productivity gains and a favorable product mix. Despite a decline in gross profit to $190 million from $196 million, Central Garden & Pet maintained margin resilience through disciplined cost management and portfolio optimization. The company’s focus on higher-margin consumables and rationalization of low-margin categories supported margin improvement.

BARK, Inc. BARK reported a consolidated gross margin of 62.5% in the third quarter of fiscal 2026, slightly down from 62.7% in the prior-year period. BARK’s modest decline was primarily driven by an unfavorable revenue mix. Despite this, BARK delivered improvement across both DTC and Commerce segments on a sequential and year-over-year basis. These trends indicate stronger underlying unit economics and operational execution, even as overall margin faced mix-related pressure.

CHWY’s Price Performance, Valuation & Estimates

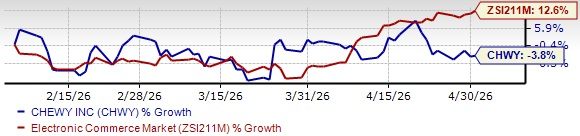

Chewy’s shares have edged down 3.8% in the past three months against the industry’s growth of 12.6%.

Image Source: Zacks Investment Research

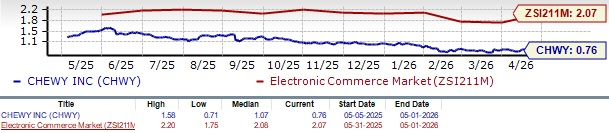

From a valuation standpoint, CHWY trades at a trailing price-to-sales ratio of 0.76X, below the industry’s average of 2.07X. It has a Value Score of A.

Image Source: Zacks Investment Research

The Zacks Consensus Estimate for CHWY’s fiscal 2026 earnings implies year-over-year growth of 28.4%, whereas the same for fiscal 2027 indicates an uptick of 22.2%. Estimates for fiscal 2026 and 2027 have been revised upward by 1 cent and unchanged, respectively, in the past 30 days.

Image Source: Zacks Investment Research

CHWY currently carries a Zacks Rank #2 (Buy). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company's customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren't winners but this one could far surpass earlier Zacks' Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Central Garden & Pet Company (CENT): Free Stock Analysis Report

Chewy (CHWY): Free Stock Analysis Report

BARK, Inc. (BARK): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).