Palantir Technologies PLTR delivered a striking first-quarter 2026 performance, underscoring its emergence as a dominant force in operational AI. The company’s results reflected exceptional top-line acceleration, expanding margins and strong customer engagement. However, beneath the headline growth lies a more nuanced investment picture shaped by capacity constraints, competitive pressures, and elevated expectations.

Strong Revenue Growth Drives Momentum

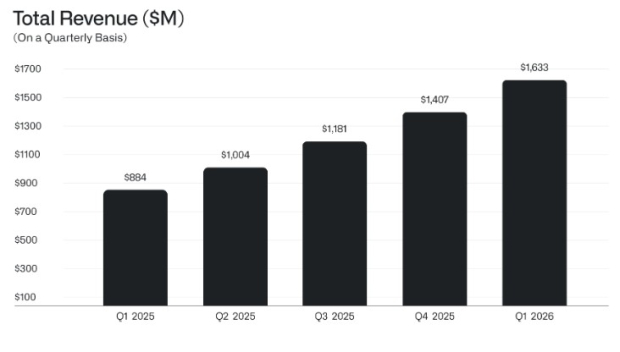

Palantir delivered first-quarter 2026 revenues of $1.63 billion that beat the Zacks Consensus Estimate by 6%, reflecting a sharp 85% year-over-year increase. Growth was broad-based, with commercial revenue reaching $774 million and government revenue at $858 million. The standout was the U.S. business, which now contributes 79% of total revenues and surged 104% year over year, highlighting intense domestic demand for AI-driven solutions.

The company also reported $2.4 billion in total contract value bookings during the quarter, indicating strong deal momentum and reinforcing visibility into future revenue streams.

Margins and Profitability Show Structural Strength

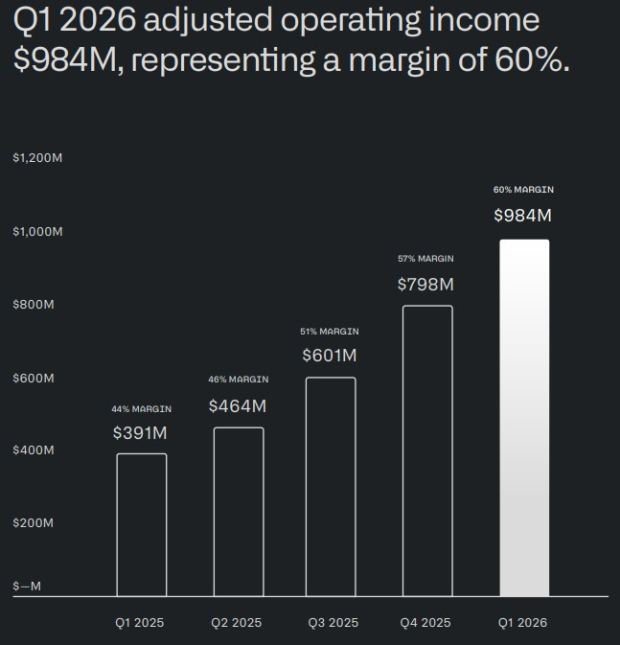

Profitability remained a defining feature of the quarter. Palantir posted an adjusted gross margin of 88%, reflecting the scalability of its platform model. Adjusted operating income came in at $984 million, translating into a 60% adjusted operating margin. Adjusted earnings per share reached 33 cents, beating the Zacks Consensus Estimate by 13.8%, showing 154% improvement from the prior year.

The company’s Rule of 40 score rose to 145%, underlining a rare combination of high growth and strong profitability. Cash flow generation was equally solid, with $899 million in operating cash flow and $925 million in adjusted free cash flow, demonstrating efficient conversion of revenue into cash.

Customer Metrics Highlight Deepening Adoption

Customer engagement metrics reinforced the strength of Palantir’s platform. The company ended the quarter with 1,007 customers, while net dollar retention stood at an impressive 150%, indicating significant expansion within the existing client base.

Forward-looking indicators remained strong, with total remaining deal value at $11.8 billion and remaining performance obligations at $4.5 billion. These figures suggest sustained demand and long-term revenue visibility as customers increasingly embed Palantir’s solutions into their operations.

AI Platform and Product Strategy Fuel Growth

Palantir’s Artificial Intelligence Platform continues to act as the primary growth engine. The company is focusing on enabling enterprise autonomy through AI-driven workflows, supported by capabilities such as cost attribution, traceability, and governance controls.

As AI model costs decline and performance converges across providers, Palantir is positioning itself at the application and operational layer, where execution, reliability, and accountability matter most. This strategic positioning is helping it stand out in an increasingly competitive AI landscape.

Raised Guidance Signals Confidence

Management raised its full-year outlook significantly, reflecting strong demand trends. The company expects second-quarter revenue between $1.797 billion and $1.801 billion, indicating continued growth momentum.

For full-year 2026, revenue guidance was raised to between $7.650 billion and $7.662 billion, marking a notable increase from prior projections. The company also expects U.S. commercial revenue to exceed $3.224 billion and projects adjusted free cash flow in the range of $4.2 billion to $4.4 billion. This upward revision signals confidence in both demand visibility and execution capability.

Key Risks Remain in Focus

Despite the strong performance, several challenges remain. The company acknowledged that it is currently unable to meet all demand in the United States, pointing to capacity constraints that could limit near-term growth. Government budget uncertainties, including the likelihood of continuing resolutions, may also affect deal timing.

Competitive pressures are intensifying as more AI players enter the enterprise space, while international expansion appears to face operational friction. These factors suggest that sustaining the current growth pace may not be entirely smooth.

Hold Strategy: Stay Invested, But Be Patient

Palantir has delivered one of the strongest quarters in the software industry, reinforcing its leadership in enterprise AI. The company’s growth trajectory, improving profitability and rising demand create a solid long-term narrative. However, the current setup also reflects elevated expectations, operational bottlenecks, and macro uncertainties. Investors already holding the stock may benefit from staying invested, while new entrants could consider waiting for better entry points. A disciplined approach that balances optimism with caution appears most appropriate at this stage.

PLTR currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Recent Earnings Snapshots

Trane Technologies TT reported impressive fourth-quarter 2025 results.TT’s quarterly earnings of $2.86 per share beat the Zacks Consensus Estimate by 1.4% and increased 9.6% from the year-ago quarter. Total revenues of $5.1 billion surpassed the consensus estimate by 1.3% and increased 5.5% from the year-ago quarter.

Booz Allen Hamilton BAH posted mixed results for the third-quarter fiscal 2026.

BAH’s earnings per share of $1.77 beat the consensus mark by 40.5% and increased 14.2% from the year-ago quarter. However, revenues of $2.6 billion missed the Zacks Consensus Estimate by 3.9% and declined 10.2% from the year-ago quarter.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company's customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren't winners but this one could far surpass earlier Zacks' Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Booz Allen Hamilton Holding Corporation (BAH): Free Stock Analysis Report

Trane Technologies plc (TT): Free Stock Analysis Report

Palantir Technologies Inc. (PLTR): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).