On May 4, Morgan Stanley raised its price target on chip maker Navitas Semiconductor (NVTS) to $12.50 from $4.50. The price target increase came in the wake of the company's strong fourth-quarter results that were reported in February. But, although NVTS on May 5 unveiled Q1 results that were favorable in some respects, and it has several strong, potential, powerful, positive catalysts, the shares are changing hands at an extremely high valuation. Further, the company is still generating very little revenue and could be vulnerable to intensifying competition going forward.

Additionally, the name is trading far above Morgan Stanley's new price target, and the investment bank kept an “Underweight” rating on the shares.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

About Navitas

The company specializes in developing semiconductor materials called GaN (Gallium Nitride) and SiC (Silicon Carbide). These materials are utilized in many of today's chargers.

In Q1, the company's revenue came in at $8.6 million, compared with $7.3 million during the previous quarter and $14 million in Q1 of 2025. It reported a loss from operations, excluding some items, of $11.7 million, better than its $12.1 million adjusted loss during the previous quarter and its $11.8 million adjusted loss in Q1 of 2025.

The shares have a market capitalization of $4.05 billion.

www.barchart.com

www.barchart.com More About Morgan Stanley's Note and the Nosebleed Valuation of NVTS Stock

Citing strength in the semiconductor space, Morgan Stanley raised its price target on NVTS, along with several other names in the sector a few days ago. But the investment bank noted that NVTS stock is expensive and asserted that its high valuation “leaves limited room for error.”

Indeed, the shares currently have an astronomical price-sales ratio of 80 times.

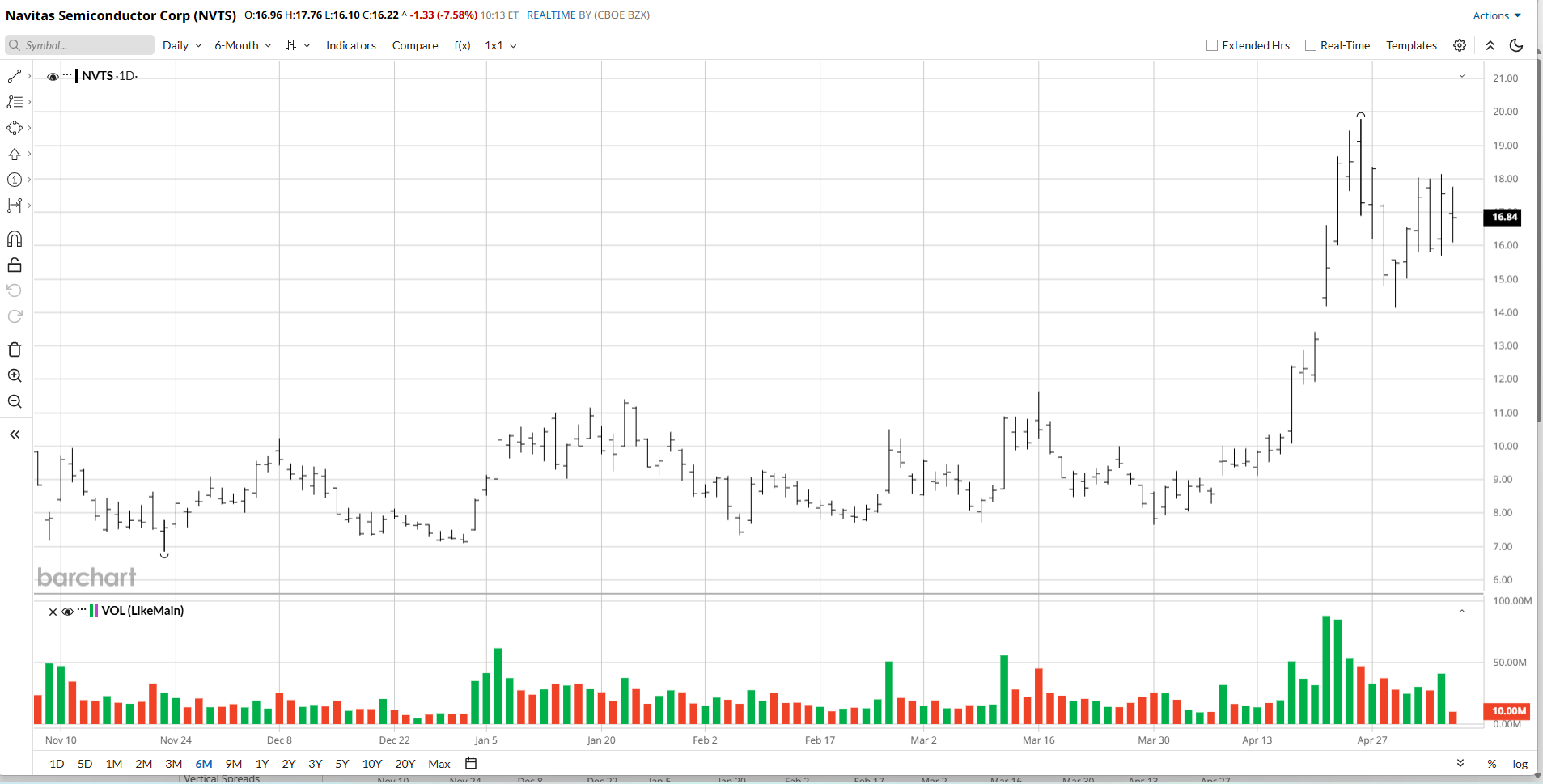

Also importantly, NVTS stock closed at $17.55 on May 5, far ahead of Morgan Stanley's price target of $12.50.

Low Revenue and Tough Potential Competition

Last quarter, the company's total revenue jumped 18% versus the previous quarter, but its total top line for Q1 came in at just $8.6 million. And in all of 2025, the firm generated revenue of just $45.9 million. In light of Navitas' low sales, the company could be dependent on very few customers, making its stock vulnerable to a big decline if it loses one of these customers.

Indeed, a great deal of the high valuation of NVTS appears to be related to its partnership with Nvidia (NVDA). Under the arrangement, the firms are jointly developing “800V high-voltage direct current (HVDC) power architecture….to support (NVDA's) ‘Kyber’ rack-scale systems.”

If Nvidia decides to abandon the collaboration with NVTS for any reason, the latter company's stock price is likely to tumble tremendously.

Making this situation more worrisome, Navitas has ten direct competitors, according to one source, which suggested that Nvidia could choose to use any of these firms in Navitas' place and that these competitors may have multiple advantages over NVTS. Additionally, NVTS “is the smallest” of these firms, according to the article. In light of these points, it's certainly quite possible that Nvidia could, at any time, decide to switch to one of Navitas' larger competitors instead of Navitas.

Morgan Stanley agrees that the firm's “competitive intensity” is “high.”

Powerful, Positive Potential Catalysts

According to Navitas CEO Chris Allexandre, who was speaking on the company's earnings call on May 5, data centers are accelerating their use of GaN and SiC, the two charging technologies provided by the firm. And with data centers rapidly proliferating to support the AI Revolution, Navitas' addressable market appears to be growing very quickly.

Plus, Navitas is "uniquely positioned as one of the very few companies that can claim deep long-term experience in both GaN and high voltage SiC technologies,” the CEO reported. And of course, NVTS can benefit a great deal from its partnership with Nvidia.

Finally, Navitas is active in the highly promising “grid infrastructure” sector, and the company's “design activity” in that area is undergoing “notable acceleration,” Allexandre noted.

The Bottom Line on NVTS Stock

Given the company's high valuation, low revenue, and meaningful competitive threats, investors should avoid the name at this time.

On the date of publication, Larry Ramer did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

After an Earnings Blowout, Morgan Stanley Just Raised This Chip Stock’s Target Price by $8 You Must Decide for Yourself If Super Micro Computer Stock Is Toxic or a Tantalizing Buy Here as Legal Drama Swirls Palantir’s Record Revenue Signals Strength — Ignore Overvaluation Fears for PLTR Stock Super Micro Computer Soars on Earnings Beat. Here's What Comes Next for SMCI Stock.