Palantir Technologies (PLTR) recently delivered a first-quarter performance that can only be described as exceptionally strong. Shattering previous revenue records, the company reported an acceleration in revenue growth, driven by massive demand for its Artificial Intelligence Platform (AIP).

Management was confident enough to raise its full-year outlook, signaling that demand for AIP isn’t slowing. However, PLTR stock retreated nearly 7% following the earnings release, extending a year-to-date (YTD) decline that has seen shares shed 24.96% value.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

The disconnect between Palantir’s solid operational performance and its share price performance is due to its valuation. Palantir remains one of the most expensive names in the software sector.

So is Palantir stock overvalued, or does its exceptional growth justify a premium? Here’s a closer look.

www.barchart.com

www.barchart.com Palantir’s AI Leadership Justifies a Premium Valuation

Palantir has evolved beyond a software provider and is an AI leader with accelerating revenue growth, a strong cash position, and no debt. This justifies its premium valuation. The company’s Q1 results marked its highest year-over-year (YOY)growth rate to date, with revenue jumping 16% sequentially and 85% annually. This also marked the eleventh consecutive quarter of accelerating top-line growth.

Palantir’s U.S. business is growing rapidly, with revenue increasing 104% YOY and 19% sequentially. This significant growth reflects the rising adoption of the company’s AIP, which is gaining traction among both commercial enterprises and government agencies. Customer count reached 1,007, up 31% YOY, while spending among large clients continues to expand. Palantir’s top 20 customers generated an average of $108 million in trailing twelve-month revenue, reflecting 55% growth and indicating strong expansion within existing accounts.

The U.S. commercial business revenue jumped 133% YOY, reflecting strong enterprise demand for operational AI deployments. Government contracts remain a significant contributor as well, with U.S. government revenue increasing 84% to $687 million, driven by both renewed contracts and new program wins.

Palantir’s net dollar retention reached 150%, a substantial increase from the prior quarter, indicating that customers are significantly increasing their spending. Total contract value bookings surged 135% YOY, strengthening the visibility and durability of future revenue streams.

Reflecting the sustained demand for its AI platform, management has raised its full-year 2026 outlook. The midpoint of revenue guidance now stands at $7.66 billion, up from $7.19 billion, and implying 71% annual growth. The company also increased its U.S. commercial revenue forecast to more than $3.224 billion, signaling anticipated growth of at least 120% in that segment. And, profitability expectations have moved higher, with adjusted operating income projected between $4.44 billion and $4.452 billion, alongside adjusted free cash flow guidance of $4.2 billion to $4.4 billion.

Overall, Palantir’s accelerating growth, expanding customer base, growing revenue from existing customers, and increased guidance suggest that demand for its AI platform remains solid, which justifies its premium valuation.

What Wall Street Projects for Palantir Stock

Palantir continues to post strong growth, driven by accelerating adoption of its integrated AI platform. Demand for its offerings has driven consistent revenue growth, strengthening the company’s position in the enterprise AI space.

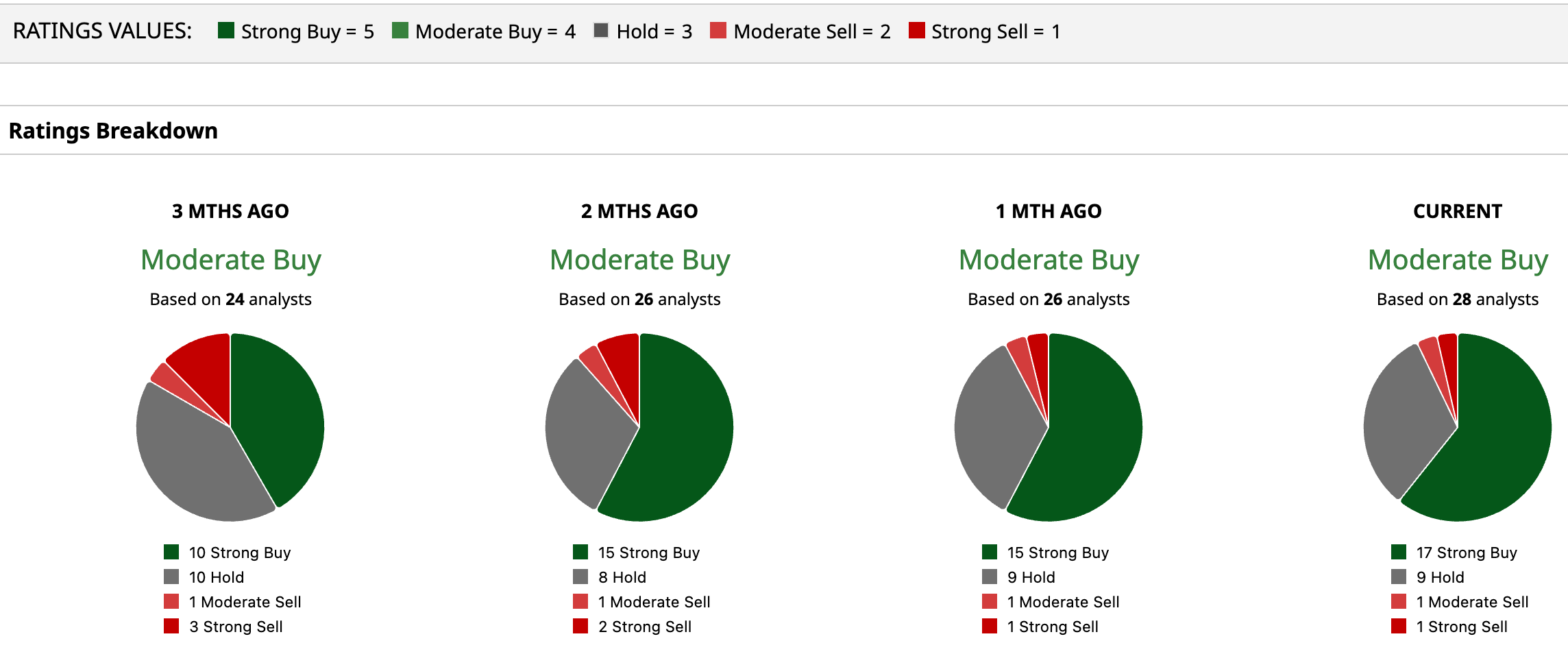

However, Palantir's stock is trading at a price-to-sales ratio of 78 times, which is significantly higher than that of any software firm. This keeps analysts cautiously optimistic on PLTR stock, reflected in the “Moderate Buy” consensus rating. Analysts’ average price target of $190.48 suggests 42.28% upside from current levels.

www.barchart.com

www.barchart.com  www.barchart.com

www.barchart.com The Bottom Line for Palantir Stock

Palantir’s latest financial results reflect that the company is executing at an exceptional level, with AI-driven demand translating into rapid revenue growth and expanding customer economics. However, the stock’s underperformance indicates that positives are already priced in and the market still sees it as overvalued.

However, Palantir’s leadership in enterprise AI and accelerating growth justify a premium multiple. Moreover, analysts also point to meaningful upside potential, indicating that long-term investors could consider gradually building a position in the stock.

On the date of publication, Amit Singh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

After an Earnings Blowout, Morgan Stanley Just Raised This Chip Stock’s Target Price by $8 You Must Decide for Yourself If Super Micro Computer Stock Is Toxic or a Tantalizing Buy Here as Legal Drama Swirls Palantir’s Record Revenue Signals Strength — Ignore Overvaluation Fears for PLTR Stock Super Micro Computer Soars on Earnings Beat. Here's What Comes Next for SMCI Stock.