Post Holdings, Inc. POST delivered second-quarter fiscal 2026 results, with both the top and bottom lines showing year-over-year growth. However, the top line missed the Zacks Consensus Estimate, while the bottom line surpassed.

POST’s Q2 Key Performance Metrics

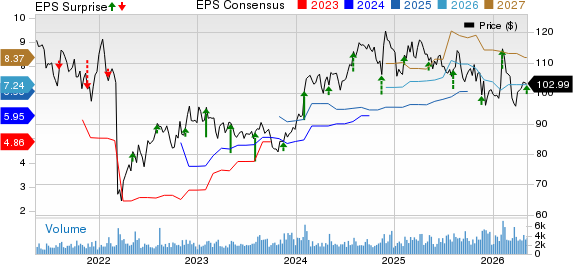

POST’s adjusted earnings per share increased 37.6% to $1.94 from $1.41 in the prior-year period and surpassed the Zacks Consensus Estimate of $1.64.

Post Holdings, Inc. Price, Consensus and EPS Surprise

Post Holdings, Inc. price-consensus-eps-surprise-chart | Post Holdings, Inc. Quote

Net sales increased 4.7% year over year to $2,042.9 million from $1,952.1 million in the prior-year period. The increase included a contribution of $152.3 million in net sales from acquisitions during the current-year period. The figure missed the Zacks Consensus Estimate of $2,062 million.

Post Holdings’ Margin & Cost Performance

Gross profit increased 13.2% year over year to $617.6 million from $545.8 million in the prior-year period. Gross margin also expanded to 30.2% from 28% in the prior-year period.

Selling, general and administrative expenses increased 3.6% year over year to $326.2 million. However, SG&A expenses as a percentage of net sales improved slightly to 16% from 16.1%, reflecting relatively stable expense leverage during the quarter.

Operating profit climbed 16.3% year over year to $211.9 million from $182.2 million in the prior-year period. Fiscal second-quarter operating profit included a $28.3 million loss on amounts held for sale related to Crystal Farms Dairy Company, which was treated as an adjustment for non-GAAP measures.

Post Holdings’ Segmental Performance

Post Consumer Brands’ net sales increased 5.8% year over year to $1,044.9 million. The Zacks Consensus Estimate is pegged at $1,059 million. Net sales included a $145 million contribution from 8th Avenue. Excluding 8th Avenue, volumes declined 10%, reflecting a 14.1% decline in pet food volumes and a 3.5% decline in cereal and granola volumes. Segment adjusted EBITDA declined 1.8% to $200.2 million, while beating the Zacks Consensus Estimate of $192 million.

Foodservice segment net sales increased 3.2% year over year to $627.4 million, missing the Zacks Consensus Estimate of $633 million. Net sales of Foodservice included a $6.5 million contribution from PPI. Excluding PPI, volumes increased 6.7%, driven by improved customer service levels and higher production in protein-based shakes. Segment adjusted EBITDA increased 47.9% to $142 million, which beat the Zacks Consensus Estimate of $135 million.

Net sales in the Refrigerated Retail segment increased 4.8% year over year to $235.3 million, supported by a 5.6% increase in volumes. This beat the Zacks Consensus Estimate of $229 million. Growth was primarily driven by higher side-dish product volumes following the introduction of private-label offerings and the shift of Easter demand into the quarter. Segment adjusted EBITDA rose 17.6% to $40.8 million, missing the Zacks Consensus Estimate of $43 million.

Weetabix net sales increased 3.3% year over year to $136.1 million, supported by a foreign currency exchange rate tailwind of approximately 680 basis points. The figure missed the Zacks Consensus Estimate of $141 million. Volumes declined 2.6%, primarily due to product discontinuations and weakness in private-label products, partially offset by growth in protein-based shakes. Segment adjusted EBITDA rose 6.6% to $32.3 million, but missed the Zacks Consensus Estimate of $34 million.

Post Capital Allocation & Financial Position.

During the second quarter of fiscal 2026, Post Holdings repurchased 3.3 million shares for $331 million at an average price of $99.85 per share. During the first six months of fiscal 2026, the company repurchased 7 million shares for $709.9 million at an average price of $100.76. Following the quarter through May 5, 2026, POST repurchased an additional 1.1 million shares for $111.9 million. Management also approved a new $600 million share repurchase authorization effective May 9, 2026.

The company ended the quarter with cash and cash equivalents of $269.4 million and long-term debt of $7,629.1 million.

What to Expect From Post Holdings in the Future?

Post Holdings maintained its full-year adjusted EBITDA guidance range of $1,550 million to $1,580 million while incorporating new cost pressures and uncertainty related to the conflict in the Middle East.

The company expects adjusted EBITDA performance in the remaining two quarters to slightly favor the fourth quarter, driven by seasonality within PCB cereal. Foodservice results are expected to align with the previously indicated $500 million annual run rate.

The company also maintained its full-year capital expenditure projection of $350 million to $390 million, with lower spending anticipated in the second half of the fiscal year.

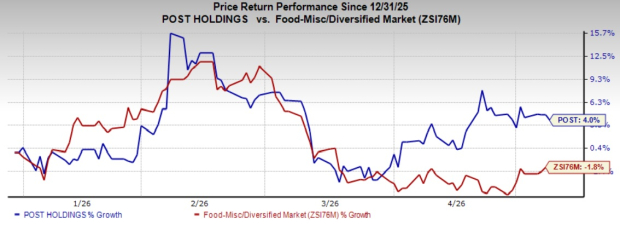

This Zacks Rank #2 (Buy) company’s shares have gained 4% in the year-to-date period against the industry’s decline of 1.8%.

Image Source: Zacks Investment Research

Other Stocks to Consider

Some ohter top-ranked stocks have been discussed below:

The Chef’s Warehouse, Inc. CHEF distributes specialty food and center-of-the-plate products in the United States, the Middle East, and Canada. CHEF currently sports a Zacks Rank #1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

The Zacks Consensus Estimate for CHEF’s current fiscal-year sales and earnings indicates growth of 8.3 and 24.7%, respectively, from the year-ago reported figures. CHEF delivered a trailing four-quarter earnings surprise of 28.9%, on average.

Darling Ingredients Inc. DAR develops, produces, and sells sustainable natural ingredients from edible and inedible bio-nutrients in North America, Europe, China, South America, and internationally. DAR currently carries a Zacks Rank #2.

The Zacks Consensus Estimate for DAR’s current fiscal-year sales and earnings implies growth of 7.1% and 567.7%, respectively, from the year-ago actuals. DAR delivered a trailing four-quarter negative earnings surprise of 16.1%, on average.

Ambev S.A. ABEV engages in the production, distribution, and sale of beer, draft beer, soft drinks, malt and food, and other beverages. ABEV currently carries a Zacks Rank #2.

The Zacks Consensus Estimate for ABEV’s current fiscal-year sales and earnings indicates growth of 17.4% and 11.1%, respectively.

Radical New Technology Could Hand Investors Huge Gains

Quantum Computing is the next technological revolution, and it could be even more advanced than AI.

While some believed the technology was years away, it is already present and moving fast. Large hyperscalers, such as Microsoft, Google, Amazon, Oracle, and even Meta and Tesla, are scrambling to integrate quantum computing into their infrastructure.

Senior Stock Strategist Kevin Cook reveals 7 carefully selected stocks poised to dominate the quantum computing landscape in his report, Beyond AI: The Quantum Leap in Computing Power .

Kevin was among the early experts who recognized NVIDIA's enormous potential back in 2016. Now, he has keyed in on what could be "the next big thing" in quantum computing supremacy. Today, you have a rare chance to position your portfolio at the forefront of this opportunity.

See Top Quantum Stocks Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Darling Ingredients Inc. (DAR): Free Stock Analysis Report

The Chefs' Warehouse, Inc. (CHEF): Free Stock Analysis Report

Post Holdings, Inc. (POST): Free Stock Analysis Report

Ambev S.A. (ABEV): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).