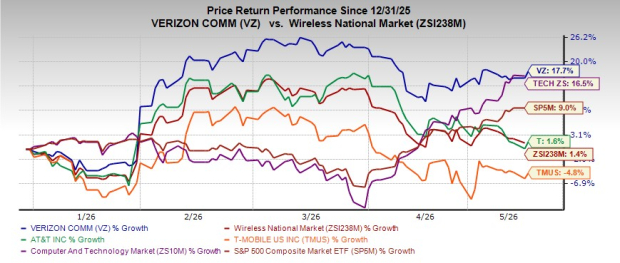

Verizon Communications Inc. VZ has gained 17.7% year to date compared with the Wireless National industry’s growth of 1.4%. The stock has outperformed the Zacks Computer & Technology sector during this period.

Image Source: Zacks Investment Research

The company has outperformed its peers like AT&T Inc. T and T-Mobile US, Inc. TMUS. Shares of AT&T have gained 1.6%, while T-Mobile has declined 4.8% during this period.

VZ Rides on Wireless Subscriber Growth, Lower Churn

Verizon is benefiting from healthy traction in the wireless vertical, backed by competitive price offers and diligent execution. The company achieved its first positive first-quarter postpaid phone net additions since 2013, adding 55,000 postpaid phone customers in Q1 2026. The company also improved total postpaid phone net adds by more than 340,000 year over year, driven by better customer retention, simplified offers and greater focus on customer satisfaction.

Consumer postpaid phone churn improved sequentially to 0.90%, with March churn falling below 0.85%. This indicates strong customer loyalty and retention trends. Management emphasized that the company is moving away from a promotion-heavy, price-hike-driven model to a customer-retention and value-driven growth model. This model focuses on transparent pricing, better service quality, bundled plan offerings and personalized customer experience.

VZ also took steps to ensure faster issue resolution, improve customer support and streamline the onboarding experience. Its convergence strategy is paying off well. Combining wireless services, fiber broadband, and fixed wireless broadband is making it difficult for customers to switch service providers. The company is also expanding its broadband infrastructure aggressively. The company is on track to exceed 32 million fiber passings by year-end.

Backed by strong momentum, Verizon raised its 2026 guidance. The company raised its 2026 adjusted earnings guidance to $4.95-$4.99 per share, implying 5.0%-6.0% year-over-year growth, up from $4.90-$4.95 expected earlier. It also tightened expectations for total retail postpaid phone net additions to the upper half of its 750,000 to 1.0 million range.

VZ Affected by Intense Competition, Heavy Debt Burden

The U.S. wireless market remains extremely competitive. T-Mobile continues to lead the industry in subscriber growth and aggressive pricing, while AT&T has recently shown strong wireless and fiber momentum. Despite operational improvements, Verizon’s mobility and broadband service revenue guidance remains only 2%-3% growth for 2026.

As of the first quarter of 2026, Verizon’s total debt stood at approximately $172.5 billion. Long-term debt exceeded $144 billion. This creates several risks related to interest fluctuations, elevated interest expenses and lower room for strategic mistakes.

Amid growing competition, the company must continuously invest in 5G network upgradation, fiber expansion and network maintenance. Its elevated debt burden, combined with a capital-intensive business model, creates pressure on free cash flow growth. Competitors like AT&T are also focusing on customer experience and convergence strategy to improve churn rate. So, although VZ saw strong improvement in churn in the first quarter, the trend might not persist in the long run as competitors initiate similar strategies.

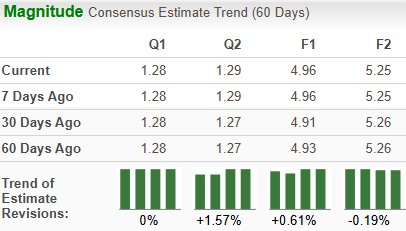

Estimate Revision Trend of VZ

VZ’s earnings estimates for 2026 have increased over the past 60 days, while for 2027, they have declined.

Image Source: Zacks Investment Research

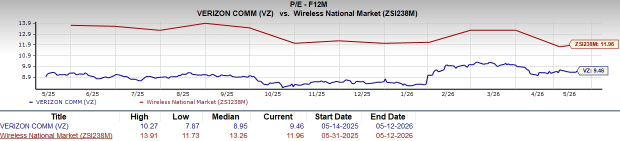

Key Valuation Metric of VZ

From a valuation standpoint, VZ appears to be trading relatively cheaper compared to the industry but trading above its mean. Going by the price/earnings ratio, the company’s shares currently trade at 9.46, lower than 11.96 for the industry.

Image Source: Zacks Investment Research

End Note

Improving wireless subscriber addition and broadband expansion are growth drivers for VZ. Focus on improving churn through various customer-oriented initiatives is a positive factor. However, stiff competition is putting pressure on the margin. High debt levels are reducing financial flexibility and making it vulnerable to economic downturns. With a Zacks Rank #3 (Hold), VZ appears to be treading in the middle of the road, and new investors could be better off if they trade with caution. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company's customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren't winners but this one could far surpass earlier Zacks' Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

AT&T Inc. (T): Free Stock Analysis Report

Verizon Communications Inc. (VZ): Free Stock Analysis Report

T-Mobile US, Inc. (TMUS): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).