Rocket Companies, Inc. RKT operates a vertically integrated homeownership platform built around the Rocket brand and its digital platform. The goal is to keep more of the homebuying and homeowner relationship in-house, from lead generation to closing and ongoing servicing.

That structure matters because Rocket is trying to smooth a cyclical mortgage business with recurring fee income from servicing, while using automation to lift conversion and expand capacity without matching fixed-cost growth.

Rocket Companies Overview and Where RKT Makes Money

Rocket’s ecosystem spans key steps in the homeownership journey. Rocket Mortgage anchors mortgage origination and financing, while Rocket Close provides national title, settlement and appraisal management that can be bundled into the transaction.

Upstream, Rocket Homes supports home search and agent referral, helping create purchase demand that can flow into Rocket Mortgage and Rocket Close. Beyond mortgages, Rocket Money is a personal finance app and Rocket Loans offers personal loans, while Lendesk provides Canadian mortgage software.

RKT Segments: Direct-to-Consumer vs Partner Network

Rocket reports two segments organized by client acquisition channel.

Direct to Consumer engages clients digitally and through mortgage bankers. It generates revenue from originating, closing, selling and servicing predominantly agency-conforming loans that are pooled and sold into the secondary market. Servicing activities are fully allocated to Direct to Consumer, including contractual servicing fees, other servicing income, and changes in the fair value of mortgage servicing rights.

Partner Network covers wholesale and enterprise partnerships, including Rocket Pro and relationships with mortgage brokers, community banks, credit unions and consumer brands. Revenue is primarily tied to gain on sale of loans and associated title, closing and appraisal fees.

Rocket also reports an All Other category that includes Rocket Money, Rocket Loans and Rocket Homes, along with professional service fee revenues from related parties.

Rocket’s Servicing Base as a Built-In Lead Engine

Servicing is central to Rocket’s strategy because it can produce recurring fee income and a built-in pool of high-intent leads. As of March 31, 2026, Rocket’s servicing portfolio totaled $2.1 trillion in unpaid principal balance across 9.4 million loans.

Management has emphasized the portfolio’s role in stable fee-based cash generation and its ability to reinforce recapture opportunities across cycles, including refinance and purchase demand.

The company also highlights a combined servicing footprint approaching 10 million homeowners and roughly $5 billion of recurring annual cash flow, which it views as a structural lead source as mortgage rates move lower and refinancing opportunities expand.

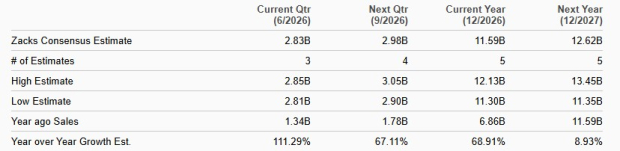

Sales Estimates

Image Source: Zacks Investment Research

RKT’s AI Push: Prospecting, Pre-Approvals, Capacity

Rocket is embedding artificial intelligence (AI) across prospecting, underwriting and client workflows to scale volume without proportional staffing increases. AI usage reduced loan officer prospecting time from up to two hours per day to zero and lifted conversion by double digits by shifting outreach toward engaged, pre-screened clients.

In February 2026, the company launched AI-powered purchase pre-approval letters. Rocket said 40% were completed outside traditional business hours, and “agentic” pre-approvals represent 10% of all pre-approvals while driving 33% higher conversion.

Those tools tie directly to Rocket’s capacity ambition. Management now cites up to $300 billion of origination capacity with several hundred fewer production team members than in 2024.

Rocket’s Redfin and Mr. Cooper Deals

Rocket acquired Redfin and Mr. Cooper Group in 2025, and the first-quarter 2026 results reflected the impact of those buyouts. Redfin adds home search and brokerage traffic that can be routed into Rocket’s mortgage and title offerings, widening the top of the funnel for purchase demand.

Rocket’s digital purchase mortgage leads hit a record in the first quarter and have grown more than three times since the July 2025 acquisition close. Mr. Cooper adds servicing scale and strengthens the recapture engine, which Rocket believes can translate servicing relationships into lower customer acquisition costs and better conversion over time.

RKT’s Near-Term Scorecard From Q1 2026 Results

Rocket posted first-quarter 2026 adjusted earnings of 15 cents per share, above the Zacks Consensus Estimate of 13 cents.

Surprise History

Image Source: Zacks Investment Research

Adjusted revenues were $2.82 billion, above the $2.7 billion consensus. Total net revenues were $2.94 billion, and total closed mortgage loan origination volume was $44.7 billion. The revenue mix reflected multiple engines. Net gain on sale of loans was $1.38 billion, loan servicing income (net) was $598 million, interest income was $507 million and other income was $460 million.

Profitability improved as scale increased, with adjusted EBITDA of $738 million. Total gain on sale margin was 2.74%, and excluding correspondent activity, gain on sale margin improved to 3.22% on $37.8 billion of closed loan volume.

Rocket’s Key Risks Investors Should Track

Rocket’s risk profile starts with an elevated expense base and heavier interest burden, which can pressure profitability if volumes do not rise enough to offset costs. Integration execution is another swing factor. The company is integrating Redfin and Mr. Cooper and must avoid disruption and cost leakage while pursuing targeted cost synergies.

Macro and industry forces also matter. Mortgage rate volatility can keep volumes uneven, while limited housing inventory, elevated home prices and affordability pressure can restrict purchase demand. Competitive pricing pressure can compress gain-on-sale margins, and regulatory uncertainty remains a headline risk, including potential changes in regulatory treatment of mortgage servicing rights.

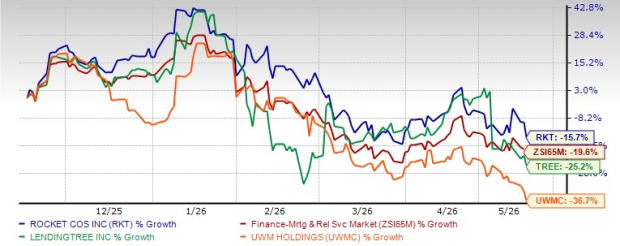

RKT’s Price Performance and Zacks Rank

Shares of Rocket have lost 15.7% in the past six months, compared with the industry’s decline of 19.7%. In the same time frame, the company’s peers, shares of LendingTree, Inc. TREE and UWM Holdings Corporation UWMC have plunged 25.2% and 36.7%, respectively.

6-Month Price Performance

Image Source: Zacks Investment Research

At present, LendingTree sports a Zacks Rank #1 (Strong Buy) and RKT carries a Zacks Rank #3 (Hold). On the other hand, UWM Holdings has a Zacks Rank #4 (Sell).

You can see the complete list of today’s Zacks #1 Rank stocks here.

Research Chief Names "Single Best Pick to Double"

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

This company targets millennial and Gen Z audiences, generating nearly $1 billion in revenue last quarter alone. A recent pullback makes now an ideal time to jump aboard. Of course, all our elite picks aren’t winners but this one could far surpass earlier Zacks’ Stocks Set to Double like Nano-X Imaging which shot up +129.6% in little more than 9 months.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Rocket Companies, Inc. (RKT): Free Stock Analysis Report

LendingTree, Inc. (TREE): Free Stock Analysis Report

UWM Holdings Corporation (UWMC): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).