Alcoa Corporation AA shares have surged 91.3% in the past six months, outperforming the industry and the S&P 500, which have returned 87.7% and 12.3%, respectively. Among its peers, Constellium SE CSTM shares have surged 131.8% and Ryerson Holding Corporation RYZ increased 32.2%, respectively, over the same time frame.

AA Outperforms Industry & S&P 500

Image Source: Zacks Investment Research

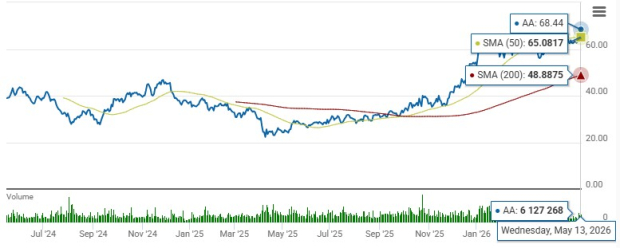

Closing at $68.44 in the last trading session, the stock is trading close to its 52-week high of $75.70 and significantly higher than its 52-week low of $25.83. It is trading above both its 50-day and 200-day moving averages, indicating solid upward momentum and confidence in the company's long-term prospects.

Alcoa Stock’s 50-Day & 200-Day Moving Averages

Image Source: Zacks Investment Research

Let’s take a look at AA’s fundamentals to better analyze how to play the stock.

Factors Driving Alcoa’s Performance

Alcoa is benefiting from strength in its Aluminum segment, supported by solid demand across packaging, electrical and transportation markets. The segment’s production capacity has increased following the restart of the San Ciprián smelter in Spain, Alumar in Brazil and Lista in Norway. In first-quarter 2026, the Aluminum’s segment’s third-party sales increased to $2.54 billion from $1.91 billion reported in the year-ago quarter.

Demand for aluminum has grown over the years, with increasing adoption of lighter and energy-efficient electric vehicles, recycled aluminum and rechargeable batteries. Alcoa is also benefiting from higher aluminum prices driven by the Middle East conflict, which has disrupted trade flows through the Strait of Hormuz. This has tightened aluminum supply in the region, driving up global aluminum prices.

The company is also gaining from U.S. tariffs on imported aluminum, which have strengthened domestic market conditions. In June 2025, the U.S. administration increased tariffs on imported aluminum to 50% as a measure to correct trade imbalances and boost the domestic industry. The move has also increased aluminum prices, thus benefiting domestic producers like Alcoa. For first-quarter 2026, aluminum product sales increased to $2.58 billion from $1.96 billion in the prior-year quarter.

The company’s Alumina segment is poised to gain from higher alumina shipments driven by the restart of San Ciprián smelter. However, shipment delays in Australia arising from the Middle East war and Cyclone Narelle are concerning for it. AA expects alumina production in 2026 to be in the range of 9.7-9.9 million tons, while shipments are anticipated to be 11.8-12.0 million tons.

However, Alcoa has been witnessing the impacts of escalating costs and expenses over time. In the first quarter, the cost of sales increased 3% year over year. The metric, as a percentage of net sales, increased 630 bps to 78.7%. Selling, general and administrative expenses also rose 16.9% in the year. The increase in operating expenses, if not controlled, might adversely impact the company’s margins in the quarters ahead.

The company’s high debt level also remains concerning. AA exited the first quarter with a total debt of $2.55 billion compared with $2.45 billion reported at the end of fourth-quarter 2025. Considering its high debt level, its cash and cash equivalents of $1.35 billion do not look impressive.

AA operates in the highly competitive primary aluminum market, which includes major industry players such as Constellium and Ryerson Holding.

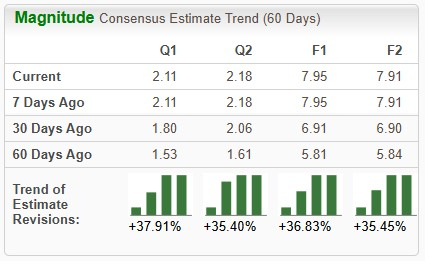

Estimate Revisions

Image Source: Zacks Investment Research

The Zacks Consensus Estimate for AA’s bottom line for 2026 has increased 36.8% in the past 60 days.

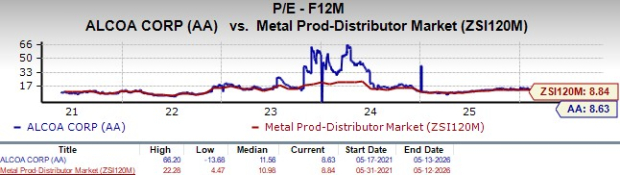

Valuation

Image Source: Zacks Investment Research

From a valuation standpoint, Alcoa is trading at a forward price-to-earnings ratio of 8.63X compared with the industry’s average of 8.88X. In comparison, Constellium and Ryerson Holding are trading at 14.80X and 11.05X, respectively.

Conclusion

Alcoa is benefiting from strong aluminum demand driven by increasing adoption of lighter and energy-efficient electric vehicles, recycled aluminum and rechargeable batteries. The company has restarted the San Ciprián smelter in Spain, which has increased production capacity within its Aluminum segment.

However, the near-term challenges, such as rising operating costs & expenses, as well as high debt levels, are limiting this Zacks Rank #3 (Hold) company’s near-term prospects. While current shareholders should hold their positions, new investors should wait for the stock to retract some of its recent gains and provide a better entry point.

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

7 Best Stocks for the Next 30 Days

Just released: Experts distill 7 elite stocks from the current list of 220 Zacks Rank #1 Strong Buys. They deem these tickers "Most Likely for Early Price Pops."

Since 1988, the full list has beaten the market more than 2X over with an average gain of +23.9% per year. So be sure to give these hand picked 7 your immediate attention.

See them now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Alcoa (AA): Free Stock Analysis Report

Constellium SE (CSTM): Free Stock Analysis Report

Ryerson Holding Corporation (RYZ): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).