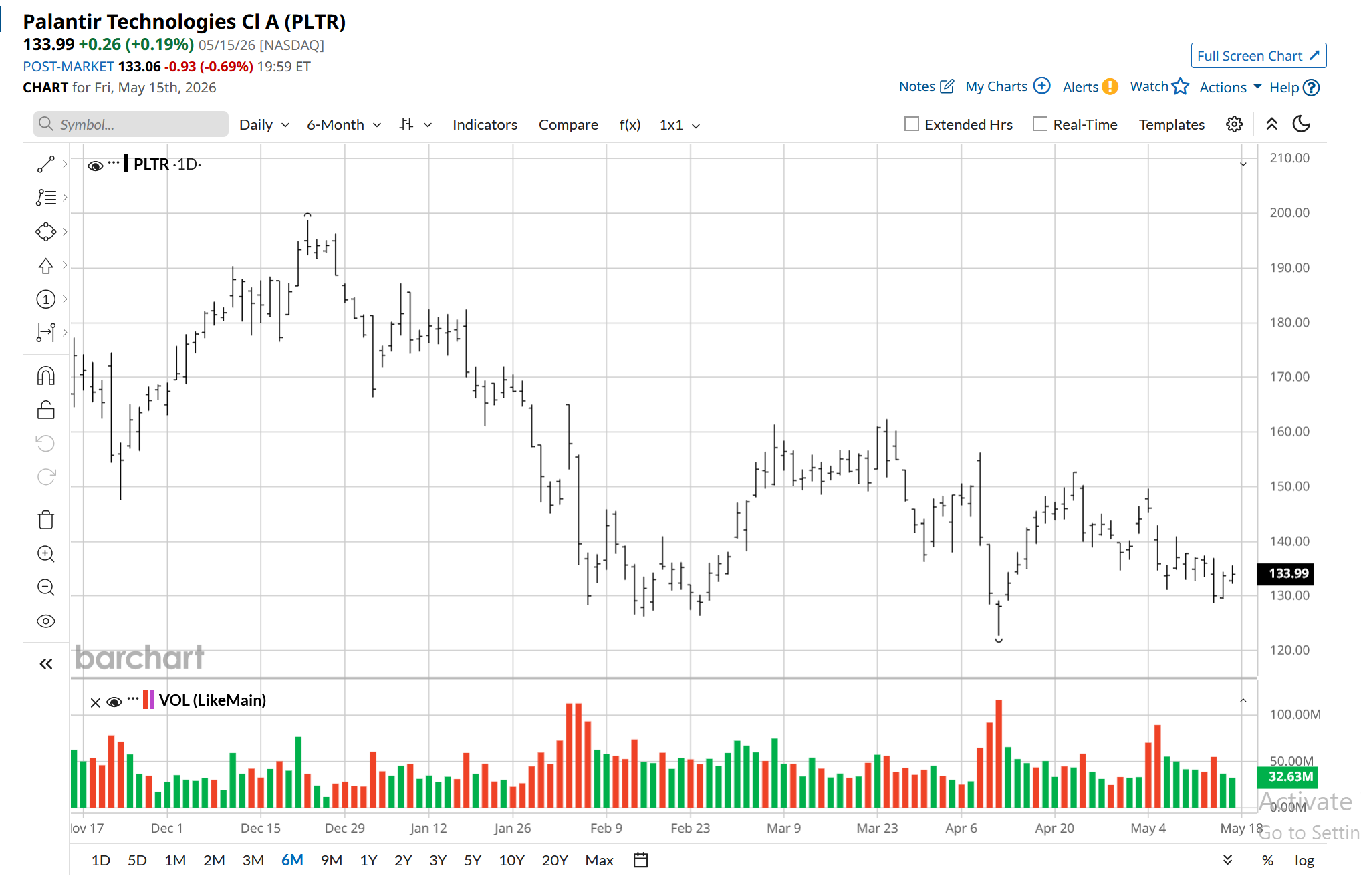

Palantir (PLTR) began as a company that worked purely with intelligence and government agencies. Once it cemented its place there, it moved to commercial businesses, targeting key industries like health care and energy. The stock became the darling of Wall Street when it later pivoted to artificial intelligence (AI) through its artificial intelligence platform (AIP). Consequently, despite losing nearly one-third of its value in the last six months, the stock is up 545% over the last five years.

The party already came to an end late last year when the stock last touched its all-time highs. It was the AI labs that crashed the party, taking away all the spotlight. But the spotlight wasn’t all they took away from Palantir. The numbers tell a story that few can argue about, and showcase how disruption from these AI labs is a much bigger threat than the high valuation.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

Anthropic is reported to have surpassed a $44 billion annual recurring revenue run rate. This is about six times the expected revenue that Palantir has guided for 2026. The fear is not just that companies like Anthropic and OpenAI threaten Palantir. It’s that they can completely obliterate even disruptive technology firms.

Currently, Palantir’s AIP integrates models from Anthropic and OpenAI to develop its enterprise offerings. This reliance, along with many other factors, has forced investors to rethink how they look at software companies and AI foundational models. If Palantir depends on Anthropic and OpenAI, then these companies deserve a higher valuation than Palantir.

Anthropic is currently exploring fundraising at a trillion-dollar valuation. At an annual recurring revenue rate of $44 billion, this gives it a valuation to annualized revenue rate ratio of 22.7x. This can be roughly compared with Panatir’s price-to-sales ratio, which is twice this number. In hindsight, those who exited the stock when it was trading at $200 were smart. Even today, Palantir’s valuation is high in light of the competitors it faces. This threat isn’t going anywhere, and if investors don’t jump ship now, it might be too late to abandon a sinking vessel.

About Palantir Technologies Stock

Founded in 2003, Palantir Technologies develops software platforms for intelligence and defense operations in the United Kingdom, the United States, and other international markets. The company’s platforms are used for intelligence-based decision-making, counterterrorism investigations, and defense operations. It offers Palantir Gotham, Palantir Foundry, Palantir Apollo, and Palantir Artificial Intelligence Platform.

The stock has underperformed the S&P 500 over the past year, delivering returns of around 4%. In comparison, the broader index generated roughly 6 times higher returns than the stock over the same period. The underperformance has continued into this year as well, with the stock falling about 24% year-to-date, while the S&P 500 has gained approximately 8%.

www.barchart.com

www.barchart.comPalantir's valuation has always been up for debate during the last three years. Compared to its own five-year average, the stock is trading at a 30% discount to its historic forward P/E and a 36% discount to its forward price-to-cash-flow multiple. A stock would usually be considered trading at a discount after such a dip, but Palantir continues to trade at a forward price-to-sales multiple of 41.6x when the IT sector’s median is just 3.31x.

The company’s expected earnings growth rate continues to hover over 40% over the next three years, as has been the case in the past. Valuation is normalizing, but the threat of disruption continues to scare investors.

Palantir Technologies Posts Solid Earnings

Palantir Technologies reported its first-quarter fiscal 2026 earnings on May 4, posting revenue of $1.633 billion. The commercial segment revenue came in at $595 million, and the government segment revenue totaled $687 million. During the quarter, the company also reported $2.4 billion in total contract value (TCV) bookings. Cash generated from operations reached $899 million. Adjusted income from operations was $984 million, with an adjusted operating margin of 60%.

Going forward, revenue for the second quarter of 2026 is expected to range from $1.797 billion to $1.801 billion. Adjusted income from operations is projected between $1.063 billion and $1.067 billion. For the full year 2026, the company increased its revenue outlook to range between $7.650 billion and $7.662 billion. The U.S. commercial revenue is now forecasted to surpass $3.224 billion.

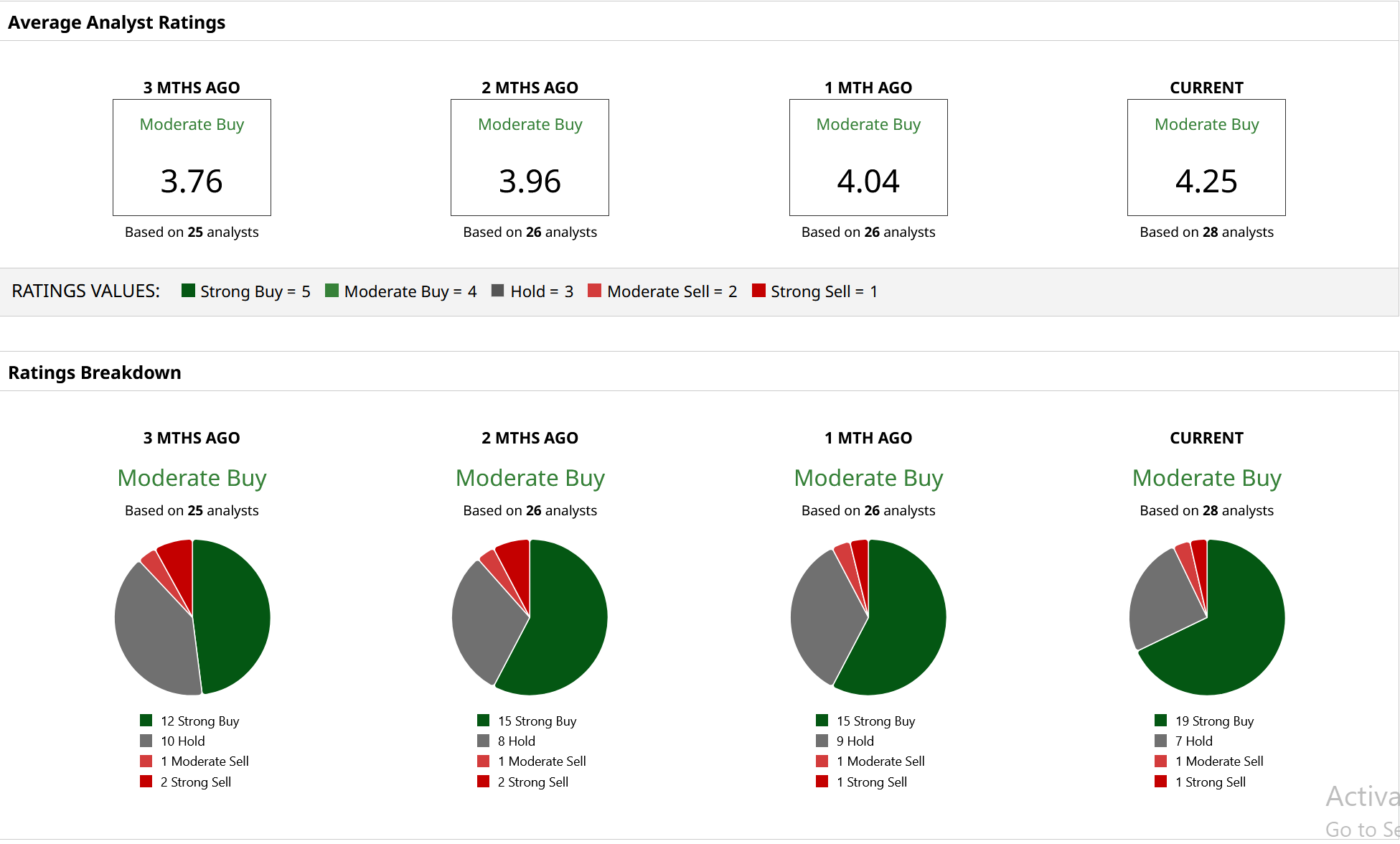

What Are Analysts Saying About Palantir Technologies Stock

Following the earnings report, several analysts adjusted their price targets upward on Palantir Technologies. On May 5, Rosenblatt Securities analyst John McPeake raised the firm’s price target on the stock from $200 to $225 while keeping a “Buy” rating. A day later, Citi also increased its price target on the shares from $210 and $225 and reaffirmed a “Buy” rating. These analysts certainly believe the threat of disruption isn't as serious.

According to 28 Wall Street analysts covering the stock, it holds a consensus “Moderate Buy” rating. Their estimates point to a mean price target of $192.50, offering 42% upside from the current levels. Moreover, the highest price target of $255 reflects an additional 89% upside from here on.

www.barchart.com

www.barchart.com On the date of publication, Jabran Kundi did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Palantir Faces a Bigger Threat Than Valuation: AI Labs Like Anthropic and OpenAI Are Disrupting the PLTR Stock Story Nvidia’s Blockbuster Quarter Is Coming — And NVDA Stock Is Still Cheap Corning Stock Rallies to All-Time Highs as AI Optical Boom Builds Oklo Looks Stronger as a Long-Term Energy Play Thanks to 2 Major Growth Drivers